Forgive my ignorance but it seems that one major problem with crypto-exchanges is that they don't necessarily have any assets other than the crypto that has been deposited there, which means all overheads (which I am assuming for some of these guys is $Ms/year) can only come from trading crypto unless they are charging reasonable money for the privilege of using their exchanges.

In the FIAT world, banks make tonnes of money from things like loans and mortgages so they can handle some risk by holding onto cash.

If this is true, how does it get fixed? Is there any reason someone would take out a loan in crypto and pay interest on the repayments?

An exchange shouldn't count deposited crypto as their asset. It is an asset of their customer.

I do not think the actual problem here is crypto exchanges being unprofitable. Even if a crypto exchange goes under, it could (and frankly should) still be able to go under gracefully, e.g. letting all customers withdraw their assets for a month (and E-Mailing private keys as a last resort).

The issue here is crypto exchanges severely mismanaging the assets of their customers.

Banks need to be heavily regulated because they are investing the assets of their customers. An exchange should not be doing that, it should be holding customer assets and making them available on request.

You can say that, but when MtGox went bankrupt, and also lost 4 fifths of its stored crypto, the court just heaped together all assets into one big pile and all creditors into one big pile and let them fight it out.

So now there's a bunch of assholes including but not limited to Peter Vessenes, that are suing the bankrupt entity for billions (completely frivolous of course) and all the depositors have waited for 8 years now to get a fraction back that the vultures have been picking on.

It's completely unfair, but the courts simply don't distinguish between someone who partners with an exchange, and someone who deposits money at an exchange.

The exchanges work very hard to not distinguish between those legally, because if they admit it, they're admitting bank-like aspects and regulations kick in, which they're often trying to avoid.

MtGox was pretty much stripped bare long before it was finally closed down. In fact it was effectively insolvent before it was even bought out by the last owner and running in pure Ponzi mode while the guy tried to make creative "investments" to get the exchange solvent again. Even with the incredible bull market on Bitcoin he couldn't make it work.

So nobody should expect to get much of anything out of the remains of MtGox.

Despite these issues, and despite and the hack, creditors are still set to make at least a 4x return (in USD) based on appreciation of the bitcoin that wasn't stolen.

To do this legally, one can have a separate legal entity to hold on to third party assets. In the Netherlands this can be done using a foundation (stichting derdengelden).

Any transactions of third party assets go through this entity and don’t touch the company at all. And this entity doesn’t take on any risk, whatsoever.

Fees etc, of course, happen separately and are paid to the company.

So in closing: this has nothing to do with fairness and everything with the exchanges (whether purposefully or through negligence) not working this way.

Well, let's not forget that BTC has gone up from $300 to $15,000 in the meantime, meaning those fractions are still worth 50x what they were back in 2014. Although who knows what the value of BTC will be once the funds are released, which is itself an event that's likely to crash the market through oversupply.

> Well, let's not forget that BTC has gone up from $300 to $15,000

Depending on how one measures. Prior to Gox's implosion, BTC was $1,000, which is the price people were actually depositing at. Meanwhile, the fact that we're denominating in USD means that we have to account for inflation if we want to compare historical data, which means the current price is more like $13,000 in 2014. There's quite the difference between 13x and 50x.

I prefer to use the trustee's watermark which reflects the value of Bitcoin after the price manipulation of fake Bitcoin being sold by MtGox had been taken out of the market at $460. But your point is made even stronger if you consider that same money could have been safely invested with a steady interest of 2-4%. And that's if you disregard that the sort of risky investments that that sort of play money could have gone to, nearly all of those investments have been extremely lucrative the past 8 years.

And that's largely because of the lack of regulation that so many cryptocurrency fans tout.

If it's not legally regulated as a currency, or a security, or anything of the sort, then why would it be considered to belong to you, and not Mt Gox, once you've given it to them?

All you have is a digital account that's basically the legal equivalent of an IOU on a napkin.

> And that's largely because of the lack of regulation that so many cryptocurrency fans tout.

In next sentence they will tell you, that you shouldn't have kept the private keys at the exchange. Use your own wallet and keep your copy of the Blockchain.

Hardware wallets, which are recommended for holding significant amounts of cryptocurrency, are designed so that even if your normal computing devices get hacked or trojaned, the software running on them cannot steal the coins.

This is because the private keys are securely stored in the hardware wallet, which never reveals them to the outside world. The user has to physically confirm a transfer on the hardware wallet itself before funds can be spent (which is why they usually have either a small touchscreen or a non-touch screen plus physical buttons).

> And once the user has confirmed the transfer, the software could send the coins to a different address, right?

No, the destination address and amount to send need to be confirmed on the hardware wallet.

The hardware wallet cryptographically signs the entire transaction with the private key, so the software in the user's computer or mobile phone cannot change the transaction without the signature becoming invalid.

The software in the user's computer can't, but the software in the hardware wallet can. It's probably more secure than running the software on a conventional computer, this I can see.

The biggest problem probably isn't modifying the transaction, which is pretty easy to catch, but using predictable keys in the hardware or somehow leaking bits of the key in the transaction.

This way they could watch all the value stored in their wallets and steal whatever they wanted by making it look like you did it yourself when one had a large enough balance to be useful.

Most societies generally recognize that a person's ownership extends past the objects in his immediate use/possession. You don't give up ownership of your car, just because you parked it on the street unattended, just like I don't become the owner of it if I steal your keys.

The point is that the holder(s) of the cryptographic keys is the only one(s) that can effectively manage (and transfer) the coins on the blockchain.

When you transfer the coins to a crypto exchange, the exchange becomes the holder of the keys and therefore you run into the risk of the crypto exchange mismanaging the coins, getting hacked, losing them, etc.

This can't happen if you securely hold the keys yourself (with a proper hardware wallet, seed backups and a reasonable amount of OPSEC).

But even in the case the crypto exchange is holding your coins (or they get stolen), legally, the coins are still yours, of course (well, unless the crypto exchange goes through bankruptcy proceedings, I suppose).

But you run the risk of never getting them back even if they are legally yours.

Which is why it's better to hold them yourself if you can.

> Thanks for explaining something to me that I did not require explanation of

It didn't seem like you understood the value of the expression "not your keys, not your coins", because you argued for the legal position, which implied that the legal position was more significant and that holding the keys didn't have as much value (even though it's the only one that actually ensures that you don't lose the coins).

Another interpretation is that you understood "not your keys, not your coins" literally, because you said (paraphrasing) "no, in fact they are your coins, otherwise stealing them wouldn't be illegal". Which implies that you did not understand the meaning and utility of the expression.

So maybe I misinterpreted you, or maybe you didn't express yourself as well as you think you did.

I didn't argue for the legal position. I pointed out that "not your keys, not your wallet" is a trite statement that doesn't account for the reality we live in, in which property law is a thing. But very generous of you to explain it again and to do so so welcomely!!

> I pointed out that "not your keys, not your wallet" is a trite statement that doesn't account for the reality we live in, in which property law is a thing.

So again, you are still interpreting the expression literally?

It doesn't mean that they are not literally your coins if you don't have the keys! Do you understand this?

It means that you can lose the coins forever if you don't have them securely stored yourself.

It's not a literal statement, it's a concise expression that gets used repeatedly to get a very important point across unsuspecting (unexperienced, novice) crypto holders. So it's actually good that it's a trite statement, because it helps to decrease the probability of someone losing money, potentially ruining their lives unexpectedly.

So that the reality is not literally what the expression says is besides the point!

In fact, I've never heard of someone (besides you) that has interpreted this expression literally and actually thought that the expression means that you completely lose the ownership of the coins as soon as you transfer them into a crypto exchange.

But if you want, I'm sure you can propose a better phrasing that has the same viral effect while also being literally true.

> But very generous of you to explain it again and to do so so welcomely!!

>So again, you are still interpreting the expression literally?

People use it literally all the time. I don't buy that people mean it figuratively. Maybe you do. But this statement is banded out so often and with no regard to the situation except where the coins are gone, it reflects little insight into the situation besides what I have pointed out.

I am happy for you that you find such meaning in the statement. That you read that statement and it means, to you, so much more than what it says.

> It's not a literal statement, it's a concise expression that gets used repeatedly to get a very important point across unsuspecting (unexperienced, novice) crypto holders.

A group of people who just so happen to think that the crypto is somehow exempt from the law, which they reflect with statements like "not your keys, not your crypto" which is said with absolutely no reflection on how property law works. It's not as if this is even a new thing, intangible property has existed long before crypto. Yet in the crypto world, the statement which you find so meaningful goes so far!

> People use it literally all the time. I don't buy that people mean it figuratively. Maybe you do. But this statement is banded out so often and with no regard to the situation except where the coins are gone, it reflects little insight into the situation besides what I have pointed out.

Well, see, when you use more words to express yourself, it actually makes it possible to understand what your point was.

I was not aware that your perception existed. So thank you (genuinely) for explaining it.

I think that this could be better explained to new users, especially by crypto exchanges which are usually the onboarding vector for them.

I think one good way to solve this, is actually for crypto exchanges to require that a relatively strict test about some crypto, investment and trading basics should be passed when you first register for an account at a crypto exchange, before these new users would be able to start operating with crypto currencies or any such trading products.

I wish crypto exchanges did this out of their own initiative rather than the government requiring such regulations, but since this is clearly not happening so far, I'm not against some government regulation for exchanges in this direction (although I'm against requirements about minimum investment amounts, as that promotes inequality and unfairness).

> A group of people who just so happen to think that the crypto is somehow exempt from the law

I'm not aware that this is the case, but I'm willing to concede that there might still be some unwarranted beliefs in this general direction, given all the carelessness that's going on from companies and projects in this sector. I hope that these people are proven wrong and either responsibility improves substantially, or that at least justice gets served when bad things happen.

> which they reflect with statements like "not your keys, not your crypto" which is said with absolutely no reflection on how property law works. It's not as if this is even a new thing, intangible property has existed long before crypto. Yet in the crypto world, the statement which you find so meaningful goes so far!

As you're already aware, I never interpreted this statement literally and never thought other people did, so I don't know... maybe you're right that the expression is not clear enough. I think my suggestion above about the test requirement for onboarding new users would improve the status quo with regards to this issue that you are pointing out.

Let the record show that I have always supported (explicit) regulation of cryptocurrency. In addition I have always held the opinion that Ripple is a security, not a cryptocurrency, and that it should never have been tolerated by the SEC. The reality there is that no one is actually doing anything about anything unless there's a big scandal. Maybe FTX will change things.

Defi is not this.

In defi exchanges you place your coins into a smart contract or have them always on your account.

If anything a crypto exchange is a misnomer as it's not even needed. The only reason it exists is because smart contracts didn't exist when they first started.

>The only reason it exists is because smart contracts didn't exist when they first started.

Calm down. That is not true. Smart contract based exchanges do not let people exchange real money into crypto. There will always need to be offchain exchanges for trading USD for crypto. Additionally, trading off chain is much cheaper than on chain.

Centralized exchanges will always exist because people want on / off ramps, people want low fees, and because people are willing to trust others.

it's superior in terms of not having the trusted third party that facilitates your trade make off with your money, as is happening in these self-described exchanges right now. Keeping a trusted third-party in the loop is always cheaper than automating that function using a blockchain, unless the risk is factored in.

There are a few classes of users. If you're the type who always uses the "I forgot my password" workflow on sites then you probably are the type who will lose your keys.

But if you're the type of trader who makes a trade and then forgets about it for a while you're at risk of losing the funds left on the exchange - like with Paypal.

Lots of things are tradeoffs. In this case, the tradeoff is that trades are more expensive on chain, but you don't have to worry that the exchange will blow up and lose all your money, like happened with a huge exchange just last week.

As a bonus, Ethereum's scaling roadmap is coming along pretty well, with a pretty clear path to 100K tx/sec within the next few years. That should make transactions quite a bit cheaper.

The flaw of BTC: everyone wants to cash out in dollars, euros or Swiss francs. Real money

BTC is barely used as an actual currency to buy things with. I could be wrong but I thought the idea was that you'd be using BTC in daily life so that you wouldn't need to go "off the ramp".

Well yes but at 2-3tx/sec, that supports a large flea market or a mid-sized costco, not a global economy. Even onboarding everyone onto Lightning would take 75 years, the entire rest of the block reward, about a trillion dollars worth of electricity and many gigatons of e-waste.

There are people, even today, who have no better choice but to use BTC for transactions or for storing value.

The point is that if you want to (or need to), you can do it. So people now have that option, which they didn't have before BTC was created.

As an example, it might be the best option for doing transactions and storing value for large amounts of people in some area, in times of crisis (e.g. financial crisis, war, oppressive governments, etc). You might not be able to use a fiat currency in such cases without significant downsides, such as extreme inflation, confiscation, blocking of bank withdrawals or transactions, going to prison, etc. Bitcoin is available and can be used whenever such events happen.

In fact, if you ever run into a situation like this, you might even desperately need BTC and will be very glad it exists, so don't discount its value so easily.

That said, sure, it would be better if there was more adoption. I think there should be and hope there will be.

But it's not exactly a flaw, in the same way as you not being able to use the currency of some obscure country in your daily life is not a flaw with that currency.

> storing value for large amounts of people in some area, in times of crisis (e.g. financial crisis, war, oppressive governments, etc).

> Bitcoin is available and can be used whenever such events happen.

Except the fact that bitcoin needs continuous internet access and electricity. The first can be blocked by oppressive government. The second can be hard to come by in times of war.

Bitcoin is a first-world solution to imaginary problems.

> Except the fact that bitcoin needs continuous internet access and electricity. > The first can be blocked by oppressive government.

First of all, bitcoin users don't need continuous internet access. At best, they need intermittent internet access.

It's also possible to use Bitcoin without internet access. Nowadays you can send and receive Bitcoin transactions over satellite, SMS and I think even over radio, no Internet required.

There are also ways to get around Internet blocking.

> The second can be hard to come by in times of war.

There are ways to produce your own electricity. And using Bitcoin (as opposed to mining it) doesn't require much electricity. You just need to be able to charge your mobile phone with a small portable solar panel.

There are also many, many, many examples of such crisis where people have access to both the Internet and electricity.

> Bitcoin is a first-world solution to imaginary problems.

You really are completely oblivious to the many crisis around the world that have happened in recent decades, aren't you?

> It's also possible to use Bitcoin without internet access. Nowadays you can send and receive Bitcoin transactions over satellite, SMS and I think even over radio, no Internet required.

All of these mean: continuous easily available connection at any point. And to send anything through SMS or radio? Again. First. World.

"To send Bitcoin (or any cryptocurrency) over ham radio you need to download the apps TxTenna and Samourai wallet, sync your phone with a goTenna mesh device, and then you’ll be set up to send and receive Bitcoin via a mesh network "

Ah yes. Apps. And readily available proprietary mesh devices.

> There are ways to produce your own electricity.

And all that is surely available and instantly accessible to people living with oppressive governments and in times of war. Instead of, you know, actual cash, barter, and storing valuables in actual valuables.

> You really are completely oblivious to the many crisis around the world that have happened in recent decades, aren't you?

It's precisely because I know of these crises that I find "generate your own electricity to just charge a mobile phone to just send bitcoin transactions over satellite or radio in times of war/oppressive government" laughable.

> You might just eat these words one day.

See, I lived through at least one of these crises in the 90s [1], after the fall of the Soviet Union. The idea that your bitcoin fantasy would survive a single brownout (or a blackout) when you need things like potable water or food now and not when "intermittent internet access is available" shows how much you understand about "the many crises around the world".

And that's without war or an oppressive government.

What good is a book on gardening when you're hungry right now? What good is a herd of cows when you need to put out a fire? You sound like an anti-second amendment person asking if we intend to use our guns to shoot down an f35 fighter.

No, bitcoin and crypto aren't going to be the savior for someone who wakes up in Mosul in the middle of the fighting.

But they might be a way out of the country with wealth intact, the difference between being a penniless refuge and a valued citizen.

> Again. First. World.

You're using first/second/third world incorrectly labels, and you're wrong. Even in the poorest places in the world, and the most war torn, we see people with their mobile devices and tiny solar panels, or charging from a merchant with a larger panel.

> continuous easily available connection at any point

No, you really don't need that. You could produce a signed transaction alone, disconnected from everyone, on your phone, and represent it as a QR code with bushes in your backyard and I could scan it from a satellite photo, decode it, and submit it to the blockchain.

This is far fetched but the point is that the transaction can be made alone and offline, transmitted to the blockchain by any means even over months or years, without risk of being modified on the way. You could hide these in letters overseas, or boxes of goods, etc.

> Instead of, you know, actual cash, barter, and storing valuables in actual valuables.

If I was you I'd list all the ways that cash and valuables can be taken and that barter might be for broken or worthless goods. Instead I'll summarize as "there are risks in everything".

>> smart contracts didn't exist when they first started.

> Calm down. That is not true.

It pretty much is. Bitcoin's solution to scripting exploits was to weaken scripting. It would have been impractical to use BTC for defi and more work was undergoing to fix those problems. The weasels snuck in at the beginning and now that we can do without them they're already in the walls.

> Smart contract based exchanges do not let people exchange real money into crypto.

For trading there are a couple of options (aside from Tether, which is a scam) for pegging a trade to USD.

For on/offramp, you are sorta right. If I want to trade for strawberries I need someone holding strawberries, and I have a risk he'll give me raspberries.

> Centralized exchanges will always exist because people want on / off ramps, people want low fees

On/off ramps don't require centralization, they only require one legally bound actor, and we can all pick our fave. You may trust a lawyer near you, I may trust my local gold bullion store for up to $5k at a time, etc.

Low fees are far better achieved by a channel or rollup based solution, where the assets are essentially on-chain the entire time.

> and because people are willing to trust others.

This is bad argument. You're trying to make trust virtuous even though removing the need for trust is far better for society - removing risk and friction for everyone.

If you let somebody borrow your car and they steal it, that's still a crime. You don't need to be a regulated and registered automotive lender to make it anymore or less of a crime. The law has surprisingly strong enforcement of even informal agreements (such as e.g. an email), and these agreements were anything but informal.

Incidentally, protection of property rights is one of the primary roles of the government in a libertarian ideology. It's not anarchy.

> you let somebody borrow your car and they steal it, that's still a crime

Agreed. But there is no public requirement to direct prosecutorial resources towards your recovery. If the criminal is prosecuted, recovery is a secondary concern, an enforcement cost often borne by the victims through civil action.

Crypto isn't money. You are not a bank customer depositing cash. I'm not sure why their customers should be creditors at all, it's a bit like asking GMail for your emails back when Google goes bankrupt.

> a bit like asking GMail for your emails back when Google goes bankrupt.

And I sure as heck would want by e-mails back if Google goes bankrupt. Google shouldn't own them, they're just an exchange for e-mails. The idea that another entity would buy those e-mails and do with them what they like is ridiculous, regardless of any juristic reality.

As much as tech-bros think that the legal system is stupid, it's usually had to deal with many variations on a theme and has ended up with broad definitions around things of value. It doesn't matter if that thing is chickens, a right to land, potential mining rights or a stamp worth millions. A weird techno thing that has a public dollar value is not hard for it to work with.

Bernice can't sleep. She tosses and turns, tosses and turns. Her partner asks, "What's the problem?"

"You know the $1,000,000 bridge loan we got from Fred's bank? It's due tomorrow and thanks to not closing the PQX deal, we don't have the money to pay."

Her partner thinks for a moment, then pulls out an iPhone and says aloud, "Hey Siri! Tell Fred that Bernice doesn't have the money to repay the bridge loan... Send!"

Bernice is aghast. "What did you do that for!?"

Bernice's partner smiles. "Now it's Fred's problem. Let him toss and turn, you can go back to sleep."

Matching orders is what brokers canonically do. Exchanges came about to consolidate their activity. There is nothing resembling a true exchange in the crypto space.

There are multiple exchanges in the crypto space. I spent 20 years working in conventional exchanges and where I work now is very much the same.

This said, we don't appear on the radar, as a conventional exchange is not as highly profitable because they can't make use of client funds or holdings. (We offer a few other unexciting institutional services that make more money than the exchange).

One day people will realise the value in conservatism in financial markets.

That's fair - in any case, the segregation of customer cash and securities from proprietary activities is a (the?) fundamental obligation of broker-dealers.

One thing that FTX was doing was minting a new totally BS coin, putting out a small float but retaining the vast majority of it. Then propping up their financials using that completely illiquid asset as collateral. On top of that, allowing Alameda to front run announcements about different coins. There's no way FTX is the only one doing this. How such a thing is allowed is absolutely baffling. It's very Enron-mtm-esque.

> An exchange shouldn't count deposited crypto as their asset. It is an asset of their customers.

Yes they should. A deposit liability arises from the fact that they received an asset in a deposit transaction. Liabilities and assets aren't mutually exclusive in any transaction, and both must increase when you receive a customer's deposit, or else where does the liability come from?

> Banks need to be heavily regulated because they are investing the assets of their customers. An exchange should not be doing that, it should be holding customer assets and making them available on request.

If the exchange doesn't spend assets they received from their customers, they still have assets. If they sit on them until they receive instruction from a customer to dispose of it, it's still an asset on their books until they carry out the instruction.

> Yes they should. A deposit liability arises from the fact that they received an asset in a deposit transaction. Liabilities and assets aren't mutually exclusive in any transaction, and both must increase when you receive a customer's deposit, or else where does the liability come from?

Does a cash transporter count the contents of their armored vans as assets? Does DHL count the contents of their vehicles and warehouses as assets? Why should exchanges be different?

I know it's the law for exchanges to account custodial funds as assets (SAB121), but I don't see why it should be this way. In fact it seems to achieve the opposite of consumer protection.

They way I look at it, deposit and withdraw implies storage. I'm not giving you something to transport, I'm giving you something to store until I tell you what to do with it at a later time.

I'm not sure I agree it achieves the opposite of consumer protection. The liability to the customer is equal to the asset being stored this way. Lack of regulation is what achieves the opposite.

An exchange facilitates trades between two parties and should not hold client assets at all, not even custodial basis.

A clearing house settles trades between two counter parts often acting as counterpart to both sides of the trade for a nominal fee. Some clearing houses also hold performance bonds (think of margin on futures).

For instance, NYSE uses National Securities Clearing Corporation (NSCC) which is a subsidary of the Depositary Trust Clearing Corporation (DTCC). DTCC is a private company owned by many banks and brokers.

In fact, banks count assets of their clients as liabilities because it is in fact money in their possession (read: control) that they owe to their clients.

There are some 0 fees exchanges, often requires significant volume or occasionally it's for limited periods and/or on a small list of pairs, but I wouldn't be suprised that someone's running fractional reserve with an exchange and offers 0 fees because they make money elsewhere.

Exchanges provide the infrastructure for trades to happen (i.e. they maintain order books, match market orders against these, ensure that settlement will eventually happen etc.), but do not take on financial positions themselves.

The "exchange rate" is only determined by the order book, i.e. ultimately by supply and demand.

So if an exchange makes money, it needs to charge at least some of its participants for these services. That can happen through transparent fees, or through less obvious mechanisms (like making retail trades free, and charging an exclusive market maker for the privilege of that exclusivity).

What do you mean by "providers"? Different exchanges?

Long-standing price differences are usually reflective of market inefficiencies that can't easily be arbitraged away, such as difficulties funding a given exchange account, insufficient volume to make it worth trading there, or many others.

Binance and bybit offer 0% fees on spot, but you usually want some kind of leverage, so you pay interest in your margin loan.

If you are not a small retail and want to trade crypto, you usually need to use futures - which are associated with fees - because of liquidity and tighter spreads.

That's how they made their money for most of their existence, and how crypto exchanges still do, but not anymore. The NYSE actually makes most of its money now by charging for colocated server space which HFT's use to get super low latency connections to the market.

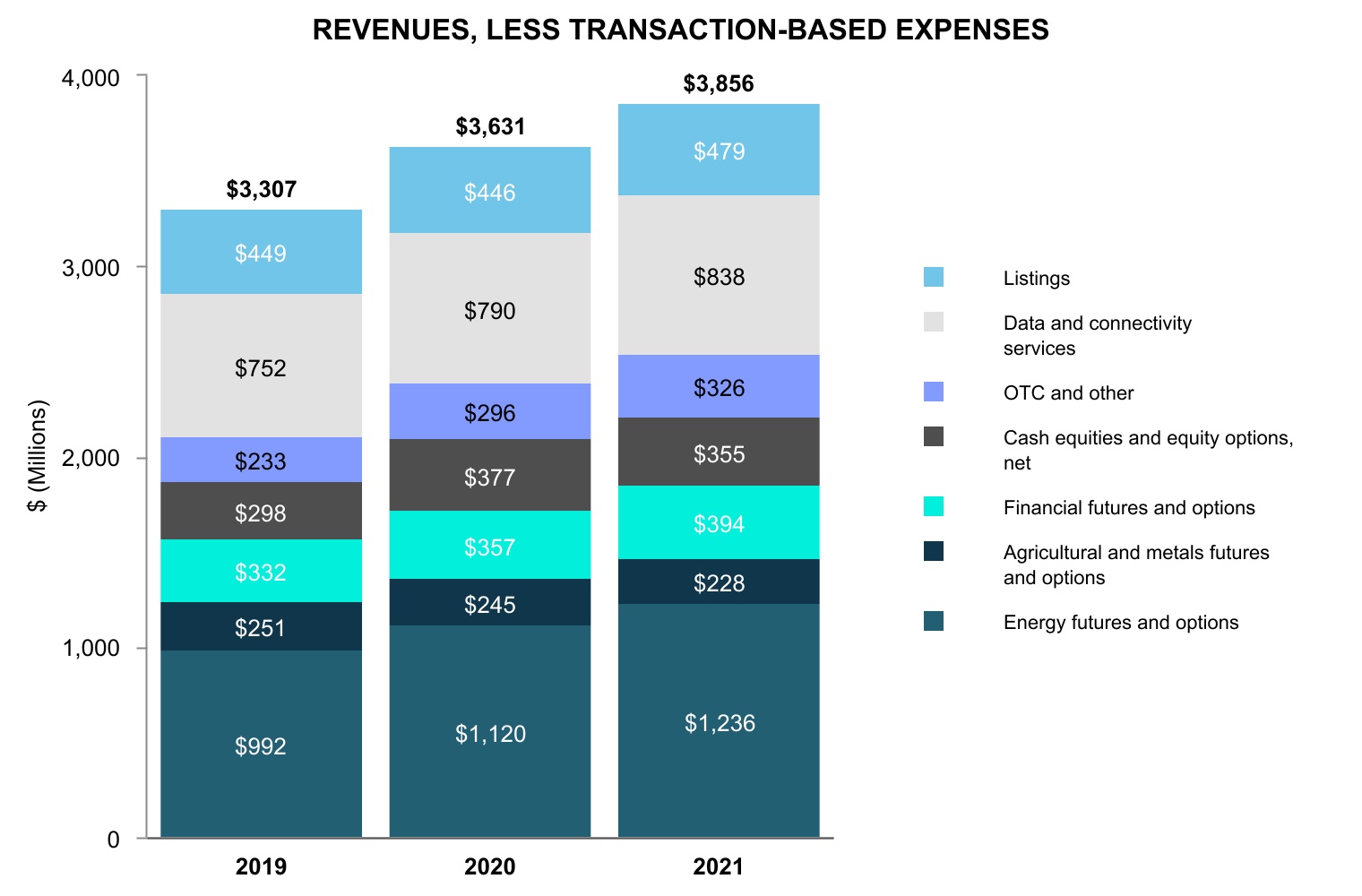

Wait, really? That sounds weirdly counterintuitive. Do you know if there's any public information about this? The only thing I could find from a quick search was [0] which doesn't provide a huge amount of info...

OP is wrong though. Their entire data and hosting revenue is $838m, but more traditional listing and transaction fees make up the rest of their $3.8b revenue. So basically 20% data and hosting, 80% classic exchange profit: https://www.sec.gov/Archives/edgar/data/1571949/000157194922...

I know nothing about the world of crypto currencies, but I do know finance.

The exchange does not hold the trades instruments/currencies/securities as assets. The business of a normal exchange is normally risk free (just matching buyers to sellers). Some exchanges step in as middle man in the trades, a process that I believe is called novation of the trade. The original trade between the buyer and the seller is novated, transformed into two trades, both against the exchange, one for each party and opposite direction. In this case the main risk is counterparty risk, the risk that one of the counterparties fail in some way.

An exchange never holds its own positions.

What is the difference in these cases? Have the crypto exchanges somehow used their users cryptosecurities as assets?

Crypto exchanges usually combine a function of an exchange and a clearing house. And tend to create ad-hock financial instruments. Hence the risk.

To me it feels like it is time to rethink at least the proof-of-work coins, particularly the CO2 emissions and energy use. It is crazy that people go cold in Europe while the energy is spent to mine bitcoins. And that the amount of CO2 produced by mining bitcoins is that of a small country. While the benefits of of all these coins seem to be nonexistent.

It's pretty dangerous though. Even though crypto is mostly on the way down and out some coins will predictably lurch upward from time to time.

If you hold an asset long you have a finite potential for loss but infinite potential for gain. Short it's the other way around. Algo traders and hedgies often treat short and long positions as symmetrical as they almost are when linearized but over long periods of time and large princemovements that's wrong. It leaves you with the hedgie viewpoint that it's as bad a "risk" that the stock market goes up too much as if it goes down which is not the way most people think.

Most of the exchanges are considered international and dance around laws and regulations. Some have versions of their site that are supposed to be dedicated to certain countries laws, but as we have seen lately that seems to be a lot of lies for a some of these exchanges as well. They make money on customer trades, but when the market is down, trade volume craters. If they were responsible with funds they would know this is coming and have planned accordingly, but most of these exchanges operate like its a perma-bull market. On top of all of that, they are leveraging heavily into other financial devices using customer funds on their books. Its a recipe for disaster.

It would be fine if it were only an exchange. If the only assets are those of the customers deposited, then everyone can withdraw at the same time without issue. The problem is that they are also lending on margin, which means they are lending customers money to use to buy more crypto.

Each customer has their margin loan secured by the crypto in their account, but in a steep drop in crypto valuations, the value of the crypto can drop below the loan principal. And if individuals don't cough up the cash to pay the balance, the exchange is on the hook for it.

And it gets worse. Where does the exchange get the cash to lend in the first place? They borrow it, of course. And like the individual traders use the securities in their account as collateral for their loans, the brokerage uses all of the securities they hold as collateral for their loan. Problem is that they don't own these securities, but rather hold them on behalf of customers. So in a situation where the exchange as a whole is undercolateralized, the brokerage as a whole can get a margin call. And then they will have to liquidate securities they hold (your crypto). This means that even if you are a customer with a low risk portfolio, you can lose your securities because the exchange took on risk to finance someone else's risky trade. This exact process happened at MF Global back in the financial crisis, and would have happened to a lot more firms if the government hadn't bailed them out.

Margin lending in the stock market is heavily regulated, and I'm sure you can see why. Crypto is the wild west. A lot of lessons were learned about this in the crash of 1929, and the crypto market is learning them now.

It gets fixed by largely replicating the traditional finance system, which would of course be completely pointless. The whole point of crypto is to evade government regulations, which means this kind of stuff is inevitable.

The problem with all these current Crypto "projects" is that they don't want to be boring. Banks and other typical financial institutions are boring; and there's a good reason for that. There's a reason why you have all those audits, certifications, compliance programmes and red tape. We (as developers/workers) may like it or not; but as customers we love it.

Banks are audited every month to verify that their reserves are there. They are also audited to see the balance between their risks and assets. Their systems are audited to ensure accountability (everyone must take at least 5 days of PTO a year, to ensure no single point of failure/fraud).

But the kids that are creating these new Crypto CeFi companies hate being boring. They got in because of the millions and the whirlwind of excitement that the Crypto space brings. And for that reason they have a mess in their internal ledgers.

I love Blockchain technologies, Bitcoin and Ethereum. But I couldn't care less for all the "cool kids" wanting to get into this train without proper adult supervision.

The problem is that the people who run the exchanges can't stop themselves from using customers' money to try to get rich.

In theory it is possible that an exchange could just take customer money, keep it in a lockbox, and make their revenue by charging transaction fees. But does that ever happen?

The kind of people who are so into crypto that they build a business out of it are fundamentally incapable of that kind of self control. They think they are revolutionaries who are remaking the financial system. They do really dumb financial stuff that the rest of us learned was bad after the 19th century. They aren't the kind of people who would just leave customer deposits alone.

Remember that FTX was supposed to be the responsible exchange. All the other ones were considered to be worse.

That's an interesting related problem - their costs are real dollars/Euro/Peso etc, but their revenue is in crypto. Eg they have to pay rent, salaries, AWS bill but their revenue is in ETH or BTC or SOL which is a fraction of what it used to be. Banks dont have that problem - their costs are denominated in same currency as their revenues.

With your description I am guessing that what you call FIAT world is a financial system that is regulated where in fact banks (not exchanges, although they are also regulated in terms of what they can do with whatever is deposited and how they create revenue) are forced to hold cash to handle the risk and ensure some safety for the deposits.

> If this is true, how does it get fixed?

So far the only way to fix this seems to be with regulations, which seems to go against one of the main arguments in favor of these assets.

It's in the name, isn't it? An exchange is where assets are exchanged.

For that service they get a fee, usually tied to the transaction volume. Pay any expenses out of that fee and keep transactions rates high is a good mode for survival.

Unfortunately, if asset prices depreciate, fees tank too. But that's manageable.

What's not manageable though if you start using assets of your customers to create a new revenue stream by locking those assets up somewhere or by using them for high-risk trades.

When people start asking their assets back you suddenly have a problem.

In the real world all organizations are regulated and fraud is illegal. But sadly something being illegal does not prevent if from happening, and greasing political palms always help:

> The 30-year-old Bankman-Fried has been a major force in Democratic politics, ranking as the party’s second-biggest individual donor in the 2021–2022 election cycle, according to Open Secrets, with donations totaling $39.8 million. That ranks only behind George Soros (about $128 million) but ahead of many other big names, including Michael Bloomberg ($28.3 million). What’s more, he had promised to spend far more on Democrats moving forward, predicting in May that he’d fund “north of $100 million” and had a “soft ceiling” of $1 billion for the 2024 elections.

Yet 18 of the 25 top donors were Republican leaning. Billionaires comprise 20% of Republican funding vs. 14% for Dems. Most republican megadonors were entirely republican. The big ones are from hedge funds.

So yeah, SBF donated to the dems. We need more regulation to get money out of politics. But let's not kid ourselves into thinking the republican party is immune to this. They are in it. They tend to be more in it.

96% of house seats were won by the party that spent more in their race.

> 96% of house seats were won by the party that spent more in their race.

I don’t think the causality here is clear. A lot of companies/billionaires/millionaires and even regular people tend to donate money towards the people who are likely to win the race. If you wanna be in the good graces of the person representing a certain district in the House the best way to do that is to make a bet on the likely winner ahead of the elections.

Many have literally $0 by outside spenders (ignoring the parties themselves).

On the other hand you don't see a ton of money going to non-competitive races because it doesn't really matter. The politician doesn't benefit all that much so it's not exactly a great way to earn favors. Or at least, that's what I'd assume. Lobbying is cheaper than people expect but a lot of these totals are so low I can't imagine it really matters to anyone.

The highest spending race was Nevada 3. With ~$15M for Republicans and ~$5M for Democrats. Predicted a likely democrat Win by 538 and ultimately won by democrats 52-48. Contradicting kind of all points here we're making. It's fuzzy of course. Need to get money out regardless.

>On the other hand you don't see a ton of money going to non-competitive races because it doesn't really matter. The politician doesn't benefit all that much so it's not exactly a great way to earn favors.

Just my own speculation, but this is probably only true to a certain point. A politician in a non-competitive race is not going to have anything productive to do with 15 million as in NV3, but money that goes to the PAC run by your former aide helps to grease his palm (so 100k goes in and 50k is spent on ads, 50k on the PAC CEO's salary for example), or to similarly grease the palm of your various consultants, friends, and family, or to grease the palms of friendly industry groups who you sincerely hope will hire you on a do-nothing job once you retire from politics.

Money coming in to a certain point is always a good thing, and I speculate being in a foregone conclusion race probably helps limit the scrutiny on how you spend it.

> So yeah, SBF donated to the dems. We need more regulation to get money out of politics. But let's not kid ourselves into thinking the republican party is immune to this. They are in it. They tend to be more in it.

Fair enough and thanks for the context, but politically connected is politically connected. Can be politically connected to democrats or republicans.

Some people will never understand how damaging this level of tech money tied up in politics is. Apparently it's easier to jump on one side and do finger-pointing than to actually accept the level of fraud happening.

SBF spent 99.9% Dems and 0.1% Repub, according to your first link.

You’re telling untrue facts according to your own sources — to minimize that the second largest Dem donor was a criminal stealing customer funds. Your comparison to Repubs is unfounded as none of their donors engaged in organized crime like SBF.

Ok buddy, look, one. You're right, it was a mistake. I misremembered something. I cited a source containing the right information and you pointed it out. Thanks.

> Why are you spreading election misinformation?

Two, Fuck off. This is needlessly passive aggressive. There is no need to throw in a worst-faith assessment of my motivations for posting all of this.

This is more misinformation than the OP - there's more criminal money flowing into republicans by far, the below is just two examples (edit: two examples) from 10 seconds of searching for an article:

Even if talking just about people who are later found to have acted improperly, look at the CEO of FTX Ryan D. Salame, one of the largest Republican donors.

10 seconds of searching is where your argument falls apart, good luck with that.

Anyway you are justifying this destructive behavior with more destructive behavior? It's no wonder you don't take more time to understand these things.

No one is justifying any behavior, criminal activity is criminal activity and the money needs to be out of politics in general. My comment is only calling out the commenter for making an obviously biased statement without even taking half a second to see if it's even conceivably true.

The argument falls apart because two examples were quick to find? If all you can complain about is that it was too easy to find two examples to counteract the commenters clearly partisan and facetious claim then it sounds like you're grasping at straws.

Please enlighten us on how we should have spent more than 10 seconds to understand that there are actually no republican donors engaged in criminal activity and the commenter was just making a factual statement we obviously don't understand.

Nobody is unbiased in their opinions about what politicians do with the money, nor should they be. But if you really want to spend more than 10 seconds I'd say reference something more academic that what google spits out as fast facts. Yes, I am partial to books and history in assessing this situation, and see no issue with complaining about you minions taking their latest "internet research" so seriously.

I'll reiterate my comment to the original OP. Billionaires donating may generally be legally doing their business. That doesn’t make it moral or ethical or completely legal. If the entire billionaire system is corrupt, pointing all fingers at the corrupt Dem party when the Repub party is just as corrupt, if not more so, is weird, uniformed, and biased. Are you spreading election misinformation?

Those other billionaires donating a ton may be mostly legally doing their huge business. That doesn’t make it moral or ethical or completely legal. If the entire system is corrupt, pointing all fingers at the corrupt Dem party when the Repub part is just as corrupt if not more so is weird, uniformed, and biased. Are you spreading election misinformation?

Who is excusing it? I'm not! You have to lock SBF up assuming everything we have heard so far is close to the truth.

I want the lot of billionaire donors to have their and their company's finances and political involvement investigated and made transparent for the public. Keep them all accountable. But ofc SBF is worse than all the rest because of how bad his actions have been. The worst. But overall we shouldn't allow any one to have such outsized power. Don't make it legal to politically donate this much money to any one.

On the other hand, you appear to be excusing the Republican donor's. Your comments are saying "go after this visibly criminal (according to our justice system) Democrat. Focus on that! Ignore all the republican [and other Democratic] ones". Being as partisan as can be.

>Excusing criminality by saying “well, legitimate business isn’t totally ethical!” is nonsense gaslighting.

I think the point was not whataboutism, but rather that the sewer of filthy lucre that we call "campaign finance," regardless of who gives/receives such funds, creates perverse incentives in the political system and should be discouraged/done away with.

It would seem that there are other failures and frauds predating Bankman-Fried, wouldn't it?

While I'm told that the ideological and technical underpinnings of crypto are designed to avoid government regulation, I hope that he is prosecuted thoroughly for any crimes he may have committed.

But further, I hope that this high profile Democratic donor drives Republicans in the House and Senate to support strong regulation on this burgeoning financial asset class/stateless currency (I'm still unsure of what it is). And in fact stronger regulation on the financial industry generally.

Republicans are about de-regulation. Whatever they may do for optics temporarily means nothing for their actual focus and goal. Democrats are not much better but I’m not hoping only one of the two parties is going to do legit sustained regulation against the way they actually behave in the medium and long term.

Why are you only looking to the Repub party? Ilhan Omar for example doesn’t care much if Biden was given corrupt money. She’s not going to suddenly do everything centrist Biden does. Biden has more in common with your average neoliberal Repub than a progressive Democrat, who themselves are normally only center-left.

> And in fact stronger regulation on the financial industry generally.

Both parties and neoliberals across the board have done the opposite since Reagan has been in power. Republicans specifically are publicly about deregulation while Dems will flip how they talk but are also about de-regulation and keeping class divides.

Look at the top donors on both sides. They are all non-working class. They all make more money via de-regulation and a capitalist society where the rich have more power than others. They already show their hands. They vote for the establishment to maintain their money and power.

Banks have regulatory requirements that reduce risk. There are insurance mechanisms to protect bank deposits and securities insurance to protect custodial assets.

The problem with crypto stuff is that it was the Wild West and that atmospheric attracts and breeds crooks.

Wrt loans, people were pretending that these coins were cash. The reality is that they are sort of like virtual silver. All debts get settled in legal tender.

This part is not actually that much different with respect to banks, where the cushion is the equity (the stock). Also, if I'm not mistaken the debt securities (bonds) issued by the bank are below the bank account claims, so that's your regular customer cushion too.

Bankruptcy is essentially drawing a horizontal line across the pyramid of liabilities, where everyone below the line gets nothing, everyone above the line gets fully paid back, and everyone on the line is the new shareholder. This line is called "fulcrum".

The difference is in government oversight (regulations) and the social agreement that bank accounts will be bailed out. Because of the former the latter rarely happens (yes I know, 2008, but this concept has been around for a century and a significant minority of protected liabilities such as bank accounts have had to be rescued since then world-wide).

> In the FIAT world, banks make tonnes of money from things like loans and mortgages so they can handle some risk by holding onto cash.

And by being a member of national and international banks; if a bank in NL fails, there's the Dutch National Bank that will step in and guarantee people's money (up until a certain amount); above that is the European Central Bank that holds a lot of money to ensure stability, reliability and trust in the fiat banking system.

Don't get me wrong, the traditional financial system is fucky (professional term) and they do a lot of weird shit with people's money ($1 invested 10x over) but there's checks & balances at least.

It's not true, they're just dipping into customer funds to make risky bets on extremely volatile instruments (more crypto assets) and losing. Along with straight up fraud stealing customer funds and having shit security and getting robbed.

It gets "fixed" by regulatory bodies like the SEC appropriately and quickly requiring a set of rules and regulations on any exchange that operates in country along with auditing, fines, and general fast and effective enforcement.

These exchanges aren't failing because of accidents or inherent risk, they're committing fraud and taking foolish risks that traditional banks aren't allowed to take.

> In the FIAT world, banks make tonnes of money from things like loans and mortgages so they can handle some risk by holding onto cash.

Also, IIRC, conventional stock exchanges make their money from transaction fees on trading volume. Are there cryptocurrency exchanges not doing that? I suppose even if they are, they're probably in trouble, since once the bubble bursts there will be a lot less trading activity going on.

Unless the exchange is only crypto-crypto they need cash as well.

> can only come from trading crypto

"trading" is a really broad term. They will get fees from trading, but they will probably also be doing things like providing liquidly to other exchanges and arbitrage (crypto is of course very volatile so arb opportunities are all over the place).

Banks don't make money from mortgages and loans, but from deposits. Our financial system uses fractional reserve. When you deposit $1 in a bank account, they are allowed to have ~10x that, or $10. They can literally create virtual money and deposit on other people's accounts (loans).

From $1 deposit, they make 900% instantly.

From $1 loan, they make 5-10% a year.

Crypto exchanges can't create money. Unless they have their own tokens. But even these tokens have more transparency than our current financial system.

So yes, they're pushed to handle their customers' money in risky ways to make a profit.

It's dumb. Against the whole point of decentralization...

>Our financial system uses fractional reserve. When you deposit $1 in a bank account, they are allowed to have ~10x that, or $10. . . . From $1 deposit, they make 900% instantly.

That is not how fractional reserve works. The way it works is when you deposit $1, the bank loans it to some other customer but there is a rule saying that they can loan out at most 90 cents of that $1. The purpose of the rule is to make it less likely that the bank will need to resort to the Federal Deposit Insurance Corporation when the bank's customers withdraw more money than the bank expects or hopes they will withdraw.

No regulation would have prevented this crime from happening.

I want to be clear here, what happened here is already illegal as is, and no regulation would have prevented it from happening in the first place.

Hell, the firm was already being audited, and those auditors didn't catch the accounting discrepancies, so it's doubtful that any additional regulation would have found this earlier either...

Regulation would have prevented it from occurring. FTX didn't sell its services in the US (FTX US did) and they certainly didn't have a NYS Bitlicense. I think this is facially obvious.

back in the day (as in like 30-60 years ago) a popular scam was to create a situation where frontrunning trades was really easy. there are a million examples of similar things.

i don't think regulation is a good thing when a single person is trading with a single person. but, at some point an exchange becomes so big (they deal, seemingly fairly and with honestly, with many people) where people start to trust it. there is an inflection point where people can take advantage of that part of the human condition. then, you need regulation, not because people are stupid, but because we're human and it is easy to fall victim.

in these cases regulation helps to preserve the trust in the systems. otherwise, people just will not use them, or they will use them in ways that are not beneficial to the group.

We need to have regulation that allows startups to open mini exchanges and banks with easy compliance and unconditional licensing but with heavy restrictions on per customer funds and total funds they are allowed to manage.

The problem is that if you want to open an exchange in say Germany that is practically impossible. You can't get equity or loans for a bank if you don't have a bank license. You need a million or more starting capital to start your own bank. It is a chicken and egg problem.

That leaves a huge hole that unregulated exchanges want to fill and they have a massive competitive edge because they aren't held back by these regulations that are meant for megacorporations.

i do think there is a separate problem entirely that regulations are often really hard to follow, i think limiting the involvement in lobbyists may help there, or at least some lobbyists...

(like, turbotax really should not have a say in how i file my taxes... or how hard it is...)

You aren't wrong, maybe it's my wishful thinking. What do you think the solution is here? Do you think the house of cards stayed propped up because a lot of people were in on the fraud? Were the auditors just incompetent or were they in on it? Auditors are reasonably well known firms.

The solution is simple, relegate centralized exchanges to niches that so far can't be fulfilled in any other way (namely fiat-crypto transactions), and use them only briefly and immediately withdraw any assets from it once the transaction you need is complete.

You may also take on insurance against such malfeasance on the part of the exchange, increasing your likelihood of recovering your funds. On the plus side insurance agencies now have a financial incentive to ensure the exchanges they insure are honest.

In other words, see centralized entities as the unreliable partner that they are and work accordingly.

If you're on HN you can be knowledgable and proactive regarding your security with crypto, but I just don't see mainstream adoption without trusted 3rd parties. I don't think insurers would underwrite that sort of thing given crypto's history.

Yes, exchanges shouldn't commingle their assets with clients funds, yet they have large operational outlays (coding &security, traditional financial fees, meth & luxury condos in Bahamas, etc.) that seem unlikely to be coverable with trading fees alone. Even if we allow them to work like banks, they still can't seem to justify the tens of billion valuations.

Pardon for living under a rock, but why are crypto exchanges affected by the mood in the crypto market?

I thought that a crypto exchange functions like a currency market: I put an offer to sell 10,000 EUR for 1 BTC and someone else puts an offer to buy 10,000 EUR for 1 BTC. When orders cross, a transaction happens and the exchange gets a fee, whether in currency or crypto units.

What are crypto exchanges fundamentally doing differently that they are suddenly losing money?

Surely a drop in transactions would make them lose fees and require them to fire some staff, but I expected a "Facebook-like" downsizing, not a full-blown bankruptcy.

Firstly, people keep their Crypto with the exchange for trading purposes and because it is easier than self custody. This means if the exchange goes bankrupt they potentially lose their money.

Secondly, as it is an unregulated space, we have instances such as FTX where they were using clients funds which should be segregated. This arguably crosses into fraud, and we do not really know which exchanges have been doing this and which ones have been properly segregating client funds. Coinbase is probably the only one we know for sure as they are an audited US publically traded company.

Finally, we also have situations where exchanges are doing things such as not matching client deposits to their reserves 1-1, or hold those reserves in less liquid investments. This could range from another fraudulent situation to good practice, but leaves them very exposed to situations where everyones wants their money back now.

Re point #2 - this is one of the crazy things for me. When you work in finance, in the UK at least, you get it drilled into your head what "client money" is, what that implies, what you can do with it, and notably you get reminded during any training session the size of the fines that get imposed on people who fuck with client money.

So to me it suggests that they simply don't employ anyone with any experience in banking or compliance, if they did those people would be raising hell or at least leaking or whistleblowing

Well, yes, it was a startup by a bunch of twentysomethings with no real banking experience. There was no partitioning.

> the size of the fines that get imposed on people who fuck with client money.

This is crypto, law doesn't apply here.

Well, that's the marketing pitch at least. So far a lot of exchanges and such like have gone bankrupt or been blatently stolen by their operators and nowhere near enough people have gone to jail.

I should say that what surprised me wasn't that a bunch of kids started up a company and during that process skirted, if not regulations, at least common sense. But that once serious money got involved and they grew into the millions and then billions of assets under management, nobody was around who could tell them that this was reckless and dangerous

All of the modern startups have skirting laws as a selling point to investors, they want them to be like that. Look at the Greyballing Uber was doing when it was a multinational billion dollar corperation. They actively don't want to play it the right way, they're going for the money.

On the contrary, they were being touted as a shining example of responsible crypto. They paid for a good reputation by donating to the “correct” causes and politicians.

It's worse than that. FTX's regulation and compliance officer was previously the legal representation for a shady online poker operation that used a bunch of offshore shell companies and whatnot to avoid US law for years. It's clear FTX's posture was to maximally avoid regulation.

You have to look at the business model of the exchange. They way you describe it is how it SHOULD work. The exchange makes money directly from you through transaction fees or just account fees. They would not need to "invest" your crypto in anything, because they have other ways to make money. This is (I think) the way Binance and Coinbase operate.

But a lot of these exchanges have attracted customers by offering interest (rather than charging a fee) and/or free transactions. But then how can the exchange make money and keep the lights on? Well they have to "invest" the customer's money. Then the investments go bad and it all blows up.

That most of them, not all of them but, by very far, most of them are downright scams, planned as scams from day one, just like in the FTX case. Evidence is mounting quickly that both Alameda Research and FTX were mounted as scams (despite the narrative that's going to be sold that it was bad luck / bad trades that sent them in a death spiral).

There are people who warned about the very scam Alameda and FTX were putting the very day FTX launched.

For FTX, turns out they called themselves "crypto exchange" but lent the money just like a bank, making them, surprisingly, vulnerable to bank run, which happened.

Unfortunately, this is common, just like $LUNA called themselves "stable coin" but it was stable only against assets in the crypto that were not stable at all.

Live by "Do your own research" and die by it. I guess.

The thing that you are missing is that crypto transactions are slow and expensive. When I say slow I mean hours to complete a single transaction. That's why people keep their money on the exchange, it's far more efficient and usable. Of course it's also risky because exchanges do rug pulls all the time. Knowing when to pull your crypto and bail is a trick. If you're seeing news articles about "minor irregularities" and "temporarily suspended trading" it is too late. Your money is gone.

Name one Crypto chain that takes hours to confirm a transaction. Bitcoin has a blocktime of 10 minutes and Ethereum is 10 to 20 seconds. More modern networks process transactions in orders of magnitude less time, eg. Solana has a slot time of 0.5 seconds and time to finality being 1 or 2 seconds.

Last time I bought something with Bitcoin (admittedly a couple of months ago) it took 7.5 hours for the transaction to clear. This wasn't with a bottom barrel transaction fee either, although it also wasn't exceptionally large. The transaction fee ended up being about 40% of what I spent on the whole thing.

Most of them are committing massive fraud. Gambling with customer funds. Misreporting trading volume via wash trading, and using that to create false impressions in the market that they can trade on. For instsnce, using their own tokens or "stablecoins" and then juicing the numbers for those.

As far as I know, Coinbase works this way. They don't transact, trade, or create derivatives of the crypto coins they manage. They simply make a profit by charging a fee per trade. They are regulated and a publicly traded company (which means certain standards of accounting) so they might be one of the only ones standing when this thing is done falling down.

These other exchanges are doing far more exotic things like creating their own coins to grant status on their exchange and creating derivatives so traders have more leverage and therefore action. Coinbase would be considered boring to these users since it is a vanilla exchange.

Crypto exchanges also function like banks (holding customer deposits, making loans/investments with customer funds), just without reserve requirements or FDIC insurance. The protections against bank runs that we have in place in TradFi are largely lacking in crypto, and the whole sector seems to have reached 1929 in its speed run of modern economic history.

Well, a lot of people will keep some $$$ and some cryptocurrency in their account at the exchange. Maybe because they want to play the day trader, being able to buy and sell at a moment's notice.

So the exchange ends up with a big account of client funds containing cash, and a big wallet of clients' cryptocurrencies.

If a bit of that money goes missing, they can cover it up for a long time, if cryptocurrencies are growing and there's net more money flowing in than flowing out. You just pay departing customers' withdrawals from new customers' deposits.

It is only when the tide goes out we find out which swimmers have lost their trunks.

And once a company's demise becomes inevitable, perhaps insiders decide to help it along. If you've already been hacked for $10 million, why not make it $100 million given the company's going under anyway and you'll be the prime suspect?

Even if an exchange doesn't start out as a scam, it might become insolvent due to a partial hack, or losing a wallet by accident, or some other screwup.

An exchange can be technically insolvent for a long time without anyone noticing, and try to fill the hole with money from fees etc. All will look normal from the outside... until too much money gets taken out too fast.

The only way to be profitable is to fee transactions.

There are a magnitude more ways to be unprofitable, however, and because of rampant incompetence, the the scales are clearly favoring the bold/gullible holding large bags of those who have fleeced.

From a legal perspective there are no required internal controls on the flow of crypto going in and out. Apparently when there is a couple of hundred million worths of crypto sitting in a wallet, it becomes real tempting to go to the racetrack so to say.

Also, most of these exchanges have their own tokens which they control the supply of and keep as "assets" on their books. In doing so they can use these self printed tokens as collateral for loans. Add to that some nicely leveraged positions in all kinds of shitcoins and you start to understand how we got here.

Crypto exchanges always have lots of money because plenty of people keep their money inside. Those lots of money are getting withdrawn by owners and spend. It would be stupid not to do so. Free money yo. It works as long as exchange grows (more money to spend) or at least does not shrink. It stops working when lots of people want to withdraw their assets which are already gone. Time to hide.

> What are crypto exchanges fundamentally doing differently that they are suddenly losing money?

Fractional reserve banking. Exchanges now offer traditional banking services such as savings accounts and loans.

They are unregulated banks with none of the insurance and government protections to bail them out. They cannot resist the temptation to gamble with the vast amounts of money they are sitting on. Only a matter of time before they lose it all and people can't withdraw their cryptocurrencies because there's no money in the reserves.

This all seems like less a problem of crypto as such, and more that exchanges are making a virtual fractional reserve currency by leveraging customer deposits for loans/investments.

ie it's a 'banking' problem, specifically a 'fractional reserve banking' problem, not a crypto problem.

This is exactly why fractional reserve banking is heavily regulated.

None of these collapses have been due to fractional reserve banking, because fractional reserve banking requires being open about what you're doing. These collapses have been about fraud. There are lots of other kinds of fraud; getting rid of this type would barely make an impact.

While there's nothing intrinsic about cryptocurrency that would make it more prone to fraud than anything else, the culture around it seems highly susceptible to it.

> While there's nothing intrinsic about cryptocurrency that would make it more prone to fraud than anything else

There are absolutely intrinsic things that make cryptocurrency more prone to fraud. The inability to reverse transactions, quasi-anonymity, and lack of any central authority to resolve disputes.

To limit fraud to the levels you see in traditional finance, you would need the regulations and oversight by centralized organizations that you have in the traditional space. The entire purpose of cryptocurrencies are to avoid those things, so while you technically could have them with a cryptocurrency, you would end up with no good reason to have a cryptocurrency at all.

> The entire purpose of cryptocurrencies are to avoid those things, so while you technically could have them with a cryptocurrency, you would end up with no good reason to have a cryptocurrency at all.

I will substitute a word from your post that will help you understand this easier:

"The entire purpose of cash is to avoid those things, so while you technically could have them with cash, you would end up with no good reason to have cash at all."

Cryptocurrency is not antithetical to banks just like cash and gold are not. It is a digital version of cash, not credit.

Cryptocurrencies are nothing like cash for one important reason: they are not subject to physical constraints.

You cannot easily scam millions of people around the world out of their hard-earned cash in a couple of days. You cannot easily move millions of dollars in cash without conspicuously hauling objects around and/or engaging many people to help with that. You can reverse a cash transaction immediately by grabbing the person and calling the police. You cannot maintain anonymity when dealing in cash without giving strong cues to bystanders and counterparties and risking being recorded on video. It is not the purpose of cash to avoid any of those “downsides”; but it clearly is a feature of cryptocurrencies.

Cryptocurrencies are a qualitatively new thing humanity has never had to deal with ever, no matter how insistent are cryptocurrency aficionados’ in calling it merely “a digital version of cash”. This serves their wallets, by suspending deserved wariness and encouraging unsophisticated people to invest into a financial pyramid, but not truthful description of reality.

> Cryptocurrencies are a qualitatively new thing humanity has never had to deal with ever, no matter how insistent are cryptocurrency aficionados’ in calling it merely “a digital version of cash”. This serves their wallets, by suspending deserved wariness and encouraging unsophisticated people to invest into a financial pyramid, but not truthful description of reality.

Holding no cryptocurrency myself (I don't need to buy anything with it atm :D) I would hardly call myself an 'aficionado'. But you must understand that to compare does not mean to equate. All I was saying is that cryptographic currencies have some of the properties that cash has, but that they also have the ease of transport and storage afforded to us by credit.

I don't see the issue with being able to transport cash across the 'net. Governments can still regulate businesses, banks, so if you go and buy a car and your government wants to know to tax it, the business selling you the car can just report this income. If a bank held your asset for you, they could just be subject to similar regulations as when they hold other assets for you. Once you stop treating it like credit or like some amorphous blob that cannot be regulated, this stuff gets pretty simple to understand.

> I don't see the issue with being able to transport cash across the 'net.

The very idea of “physically unconstrained cash” is relatively new to humanity so there are some unknown unknowns, but even then I think the issues are obvious by now.

The necessity to handle a physical object limits the scale of potential upsides (help relatives, etc.) and downsides (scam people, etc.) of cash—and it might have transpired that, with that necessity removed, the downsides and exploits are much more sought after and outweigh potential upsides.

I believe that every single sentence in your second paragraph is factually incorrect. I know of all of the things you say aren’t possible with cash are, for a fact, possible and common.

You live in a different world, I guess. In this universe you need duffel bags to move a moderate amount of cash, vans or trucks a large amount, because physics. Ah, and those duffel bags and vans 1) are conspicuous and obvious on CCTVs, 2) require people to handle, and 3) can’t teleport across oceans.

(This is just one sentence you claimed incorrect; I don’t see the the point on going through the rest because maybe I’m missing something but they seem similarly obvious to me personally.)

This sort of rhetoric is suboptimal. It only seems persuasive because you consider cryptocurrency to be analogous in purpose to cash, but the person you're trying to convince likely does not believe this. If they did, then they likely would already see purposes of cryptocurrency other than avoiding regulation, via the analogy.

If you're going to argue through analogy, you ideally need to ensure agreement with the analogy. Since asynchronous discussions make this difficult, we often need to settle for motivating the analogy instead. Simply assuming it is usually not persuasive.

Thanks for the advice. I use synchronous media like chat protocols much more often, and was blind to this- and yep, it does seem like the primary objection to that argument was born out of a flawed understanding of the analogy.

The entire purpose of cash is NOT to avoid a central authority... in fact, all cash has a central authority in the form of the government who issues the currency.

But the WHOLE point of crypto was to avoid governmental control. If the government is regulating it that means they can control it. And it becomes completely worthless. If you want digital gold as an inflation hedge you can literally buy a GLD ETF. It gives you digital shares in actual GOLD.

There's nothing to stop people using crypto to buy/sell goods directly, or to trade directly between themselves, completely outside of government control. And crypto itself can't be inflated away, or obsoleted, or otherwise really controlled by government, except by attacking it; making it illegal to own or trade, to operate nodes, to write code, or use CIA shenanigans, etc.

But if an exchange claims that they hold your crypto 'frozen' and completely separate from their trading activities, and especially if the exchange also deal in government currency, then I think it's quite right for government to regulate, and ensure the exchanges are compliant.

Vendors of goods and services have virtually no interest in self custody. They want deposits going to a bank/exchange. So you are not going to be able to buy many goods or services directly. How many businesses are CASH only today? That is best case scenario for buy/sell crypto directly.

> But the WHOLE point of crypto was to avoid governmental control

I think from a purist perspective that is true. I said this upthread but what people really want is more USD in their checking account. These exchanges are a place where they can roll the dice and maybe make that happen. As I said before, i bet 95% of the people burned couldn't care less about the philosophical aims of crypto currencies and just want a chance to get rich (in USD).

That may actually be counterproductive. If you start regulating crypto, then you are IN. You can't do it half way. Now you have yet another banking sector to regulate.

Maybe what's better and cheaper is to let this wild west "enjoy being poor" nonsense flame out until everyone shoots themselves and it's curtains.