The table really should include revenue, assets and debt columns, along with some notes about how any debt is structured. For instance, Nutanix has $1.6B in the bank, $1.2B in annual revenue, and their annual loss per share is trending down while sales trend up.

They also have a ton of debt. Hopefully there isn't a balloon payment / interest rate adjustment coming soon. Assuming they're not heading to some financing cliff, then borrowing at less than inflation rates, and using the money to buy market share was probably the right move.

Given their debt levels, could some of these companies may take down financial companies with them though?

If these (and other unicorn companies) secured what could be some several billions of dollars in low interest debt with their stock as collateral, that means those loans have been securitized, resold, and leveraged again into the market using other derivatives. It also means that the interest rates hikes coming from the Fed may cause those companies to sell more stock to make their interest payments - which will drive their stock down, knocking the collateral out from under the loan, with a bazillion or so in derivatives hinging on it.

Totally hypothetical though. I am sure they have it under control.

It does sound like unicornageddon if interest rates jump though. The 2008-billion dollar question would be, who is holding the derivatives on those loans? It's probably different this time, it's not like 2008 could happen again, and we learned from history so much so that Margot Robbie in a bathtub explained it to us. The US could probably afford another bailout if it came to it, and it's not like the conseqeunt inflation would trigger rapid de-dollarization of the global economy as big national holders dumped their reserves and created huge bubbles in anything that facilitated capital flight out of USD - like oil, fertilizer, and other necessary things to keep whole continents of people from starving. Co-operation would need to persist instead of nations turning inward to solve their own problems and fend off internal strife, instead of co-ordinating a response. This is fine.

In the case of rideshare/delivery companies on the list like Uber, Lyft, and Doordash, the bulk of their expenses/losses aren't salaries, it's in subsidizing every ride/delivery to compete on price while still compensating drivers enough for it to be worth it to them.

In other words, Uber didn't burn $30B on salaries, it burned it selling $1 bills for $0.70 over and over and over again.

This is just not true. Uber and Lyft definitely sell rides for more than they pay out to the driver. Lyft, as an example, has 3.9 billion in revenue against COGS of 2.2 billion.

It’s not “hidden” in that it’s not on their financial statements. It’s that churn of drivers and adding of passengers is accounted for in their marketing budget so if you want to do a fair comparison of cost per ride you need to figure out how to break out that component.

It’s no different than any other companies marketing budget and is definitely not fraud.

There is a big distance between the unmentioned 0 and your 1.

0.1 - 0.999 - they raised round after round of VC, paying back the previous round with big profits.

1 - they sold the gullible public (which never should have happened - regulators should have prevented the IPO!) on a business model with no real hope of profit.

There was a time not so long ago when you could never get an ICO to happen if you were not profitable for several years beforehand.

Keep in mind that regulation has been relaxed significantly each decade for a long time. There is a political party which exists almost entirely to eliminate regulation, and they boast about it. One would be led to believe that regulation was what was holding us all back from living full lives.

I'm normally pretty sympathetic to all those positions you disagree with.

I think that the state regulation, control, bailouts, and corruption are holding us back.

You can have the state pick winners and bail out idiot investors when they lose their shirt. I would rather make individuals and companies responsible for their own good or bad bets.

For me, part of that means letting people place their bets with minimal state intervention and guarantees about the bet.

In 2008, the bailouts were for the banks and institutions. They did nothing for the people who had already been screwed.

Finance and wealthy interest control US policies. By a large margin, the public welfare is funneled upward to a minority with the power to direct and focus lobbying. The individuals on the ground get far less.

A free market allows some groups to become so powerful that they can exert forces which prevent competition. Then the free market ceases to exist, and the monopolies take control. Whether this is corporations in an industry or wealthy groups in a population, it is the same.

> letting people place their bets with minimal state intervention

What is the value of this freedom when all the bets are placed with "institutions" which will rob (/cheat) the investor?

Any rock you turn over, you will see preference given to people of power or wealth. The accredited financial institutions have been publicly shown to favor insiders or themselves, for example. Retail investors would be advised to invest in things that the institutions knew were bad by the firms they trusted in and paid for advice to.

There is virtually no fairness or mathema†ical equality afforded to everyone in the current systems of government. To believe otherwise is fantasy. If one is in the right group, they have a marked advantage. For the rest, they are almost assured to get much lower results from their efforts.

>In 2008, the bailouts were for the banks and institutions. They did nothing for the people who had already been screwed.

I agree with most of you sentiment, but differ in that I think that government is the broken tool which funnels funds up tow a small minority (eg massive financial institutions).

If institutions and individuals get to freely distribute the costs of their mistakes, there is a reduced incentive to make smart choices.

>What is the value of this freedom when all the bets are placed with "institutions" which will rob (/cheat) the investor?

I think that institutions maintain monopoly power largely due to the help of the government.

>Any rock you turn over, you will see preference given to people of power or wealth. The accredited financial institutions have been publicly shown to favor insiders or themselves, for example. Retail investors would be advised to invest in things that the institutions knew were bad by the firms they trusted in and paid for advice to.

>There is virtually no fairness or mathema†ical equality afforded to everyone in the current systems of government. To believe otherwise is fantasy. If one is in the right group, they have a marked advantage. For the rest, they are almost assured to get much lower results from their efforts.

My point exactly. The government has an ultimate monopoly of power in the US and is a corrupt steward of that power.

Social stability needs to be maintained by government even if that means everyone's getting a bail out.

When a million people lose their savings it is EVERYONE'S problem.

See Roosevelt's New Deal that saved the country (and got America in shape to fight WW2).

ETFs investing in utterly non-profitable companies does not make it valid.

The reason ETFs are putting money in riskier and riskier places is that there is too much money concentrated in a few places, and there are rules as to what % of their investments can be put into one investment.

> Now to be clear, some of these companies are hopelessly screwed.

I'm not sure about that. I imagine that for the founders and top executives of these "loser" companies, they are having the time of their lives: Earning top money fast without doing too much. So, from their point of view, the company is doing fine. Now, sure, employees are always screwed no matter what ;)

With all the unspoken but obvious disdain for the ridiculous cryptocurrency schemes, I wonder if the HN crowd will recognize the elephant in the room here.

TFA illustrates that the venture capital/startup tech scene is arguably the biggest Ponzi scheme in the last 20+ years.

Even ignoring the financial losses, most of these companies have operated in a gray or fully illegal manner. So imagine that the financials don't work and the legalities don't work... and yet this is our HN universe.

Edit: (added) sorry to offend those of you who work for Uber or other companies which operate on fantasy funding with no actual profitable business model; sometimes I forget the illusion is so strong and people immersed don't know better.

> venture capital/startup tech scene is arguably the biggest Ponzi scheme in the last 20+ years

Between VC returns, at the top decile (where it outperforms) and broadly (where it simply performs), and the tangible track record of VC-backed companies from SpaceX to Moderna, this comparison is foundationally false.

Well, I'd rather ride in an Uber than a cab and until very recently stay in an Airbnb rather than a hotel. For better or worse, they truly did disrupt those industries for consumers, much as non-customers might complain.

In Netherlands, most (all?) Ubers are actually cabs. And many of my NL Uber rides have thankfully been in the taxi cars which are well maintained Mercedes E or S class cars rather than some dude's 1995 Toyota Corrola.

What Uber did that was great was provide an app where you could call a taxi. How they got ahead was by ignoring regulation which enabled them to provide lower fares and get more business.

But Uber could not exist without traditional cabs. Or at least, something would fill the void of Uber if there were no cabs. There are many places in cities where cabs congregate to wait for passengers. Airports are probably the best example.

People leaving airplanes often need a ride to their final destination. Imagine if everyone leaving the airport had to find a way to get local mobile service and then call an Uber. Eventually you'd end up with Uber drivers recognizing this need and parking themselves near the airport, ignoring calls, and choosing only nearby airport calls.

The taxi industry needed a kick in the ass; there is no question. But all they lacked was a good software company and service. They did not need a fleet of regular dudes who happen to own cars and who get deluded into thinking they can have a real income from driving people around. The news is full of sad stories of people who struggle to get by as Uber drivers.

> For better or worse, they truly did disrupt those industries for consumers, much as non-customers might complain.

Ignoring all the suffering caused by the externalities on rental market caused by Airbnb in very touristic areas (e.g.: Lisbon, Barcelona, etc.), it's great for consumers.

The issue is that none of these externalities are priced in, there is no compensation or fair counterpart for the victims of these companies. And somehow it all seems ok for some people...

>They aren't externalities and shouldn't be priced in.

If people in my city can't afford housing because of AirBnB, it has negative impacts on my city as a whole. This is an externality, which--by definition--is a thing that isn't priced in. An externality is defined as "a side effect or consequence of an industrial or commercial activity that affects other parties without this being reflected in the cost of the goods or services involved, such as the pollination of surrounding crops by bees kept for honey."

>Should the luddites have been compensated by those who operated mechanical looms?

UBI advocates might say yes; it's the whole idea that once some threshold of automation is passed, you won't have enough consumers to keep the economy running.

> If people in my city can't afford housing because of AirBnB, it has negative impacts on my city as a whole. This is an externality, which--by definition--is a thing that isn't priced in.

That's not an externality - the cost of housing is priced into AirBnB costs. Most "pricing out" happens because cities make it de facto illegal to build new houses, mostly because existing owners are quite happy with the resulting increase in their house prices (and renters don't vote).

I don't remember where it was in the US; maybe it was Cheyanne Wyoming or elsewhere, but it was a nature/mountain area popular with tourists. But their city leaders recognized the problem of tourist vs local housing prices, and they created regulation to ensure that there were enough local houses (affordable to locals).

The problem in popular tourist areas is that more wealthy people can afford to come and stay for short periods and are willing to pay a lot, so owners of houses and apartments can make more money off tourists than locals. Naturally they choose the higher income option and go with Airbnb (for example).

This leads to situations like Aspen, Colorado, where the "local" who work in Aspen have to live 30-60+ minutes away. They cannot afford to live where they work. And it means that in off seasons, these towns are just dead. Many shops close, there's no community, and there's little life. It might as well be a Disneyland which is only open for 8 months of the year.

Amsterdam is a hugely popular tourist area. Granted the atmosphere, architecture, and museums are high value; but sadly I think also the weed focus is high (sorry). Whatever the reason, it means a LOT of tourists. In my small 10 years, I have seen an immense growth. Airbnb and cheap airlines like Ryanair have made it far worse.

But to your point of housing prices, there has also been a lot of Chinese and other foreign property investment in Amsterdam (where the owners never intend to live there). Of course they seek to rent their properties, and short term rentals like Airbnb are generally more profitable in tourist areas. Still, this is not good for the cities or locals, and whether it's beneficial for visitors or not is effectively irrelevant. The city is nothing without happy locals.

I've never really understood this locals-as-utility-monsters perspective. Disneyland is great! We should have more Disneylands, and if a town contributes more to human happiness as a Disneyland than it would as a town, that's something to celebrate.

Long commutes suck (and I'm 100% in favour of land value taxes and legalised homebuilding so that we can build more homes near where the jobs are), but presumably if people are choosing to work in Aspen despite a long commute then the wages or other benefits are worthwhile even without that.

I'm not sure I understand the "monsters" bit... But "if a town contributes more to human happiness as a Disneyland" I can speak to.

The people who live in small towns in the mountains in Colorado do want and need work, but they also want and need to be able to live. When there are some tourists, it helps provide work. And the locals typically do different jobs depending on the season.

But when the area becomes "hot", and remote wealthy people start buying up local property, the locals get priced out. It's essentially gentrification on a small scale.

One could argue that the remote wealthy people deserve to have a good life anywhere they go because they can afford it, but it absolutely comes at a cost to local poor people in the areas they travel to.

With proper regulation, you have hotels and formal tourist stay locations which extract taxes that can be used to help ensure the local workers get a decent life while catering to the visitors. But without proper regulation or planning, the locals get priced out of their own towns.

Realize that low wage workers usually cannot just say, "oh well, it's too expensive here now, so we'll move cross country to find affordable housing and jobs".

Airbnb made it worse, because not only is there the traditional gentrification but now also people who own apartments can seek higher rents from tourists than with locals.

> With proper regulation, you have hotels and formal tourist stay locations which extract taxes that can be used to help ensure the local workers get a decent life while catering to the visitors. But without proper regulation or planning, the locals get priced out of their own towns.

It's actually mostly the opposite. More money coming into a town tends to lift all boats - unless, like many contemporary American towns, building more homes in town is made de facto illegal through regulations and planning.

> Airbnb made it worse, because not only is there the traditional gentrification but now also people who own apartments can seek higher rents from tourists than with locals.

Equally those higher rents are possible because you're making tourism possible for people who probably couldn't afford to travel otherwise. The people staying in (regular apartment) Airbnbs tend to be lower-middle-class at best, and I don't think we should automatically care more about locals than tourists just because they happened to be born somewhere nice.

The sad part is that the most common solution is to simply raise property taxes and subsidize rent for local workers.

This does nothing to address the underlying problem, so worker wages remain low, housing prices increase. As a result, the affordability for locals gets worse, and they become more dependent on on wealth transfers with no end in sight.

Is the cost of housing the people who can no longer afford rent or houses because of AirBnB factored into the cost of AirBnB? No. Therefore, externality.

> Is the cost of housing the people who can no longer afford rent or houses because of AirBnB factored into the cost of AirBnB?

Yes - the market-clearing price of housing reflects all the demand for housing, whether that's being paid by renters, AirBnB, local authorities or whoever.

People often mistake causality for externality, so much so the outside of Economics circles the two are being conflated. Airbnb can cause rent to go up, but that doesn't make it an externality. An externality is an input that you're using up or an output that you're not paying for.

Businesses and individuals can have all kinds of negative effects on others that are not externalities.

Hotels and boarding houses do make an imposition on their surrounding communities. Having taxes and zoning requirements on them to compensate for that is reasonable, and most of AirBNB's "edge" comes from violating those laws.

Noise pollution and additional crime experienced by neighbors from the short-term guests staying at Airbnb locations would qualify as an externality. Higher occupancy in Airbnb locations stresses capacity in pools, parking, gyms and other amenities of the neighborhood or complex is also an externality.

How is it not an externality that local communities in Lisbon, Barcelona, Venice (among many others), who work and used to live in the city, are being pushed out of their own cities purely by landlords renting out their properties on AirBnB instead of offering as housing. Emptying cities is not great for any part of society, not even for the tourists that are the driving force of this.

Venice is a hollow city, there's very few real people anymore in the center. Lisbon has been suffering for years with ever-increasing rents mostly driven by tourism pricing out the local population. There might not be enough dwellings and the housing market is much more complex than this but it's an enormous externality on local populations that they don't get close to fair compensation compared to being kicked out from your home.

How exactly is this not an externality?

Luddites and looms is a very different issue than a necessity as basic as shelter. When you found an analogy related to food or water we can use it instead.

> How is it not an externality that local communities in Lisbon, Barcelona, Venice (among many others), who work and used to live in the city, are being pushed out of their own cities purely by landlords renting out their properties on AirBnB instead of offering as housing.

Increased demand pushing up the price is not an externality.

> Venice is a hollow city, there's very few real people anymore in the center.

And it contributes a lot more to overall human happiness that way.

> Luddites and looms is a very different issue than a necessity as basic as shelter. When you found an analogy related to food or water we can use it instead.

The Luddites were losing their whole livelihood - you can say all they lost was money, but without money they couldn't buy food or water or shelter. (Also, outside of a few climates cloth and clothes are every bit as much a basic human necessity as those)

> And it contributes a lot more to overall human happiness that way.

That's not the metric I look to optimise for, not sure why you believe I should take "overall human happiness" as the ultimate goal, some kind of weird min-maxing of real life, even less when dealing with things such as whole cities and communities, seems quite ideological to me. I really don't buy it.

Any coherent approach to morality min-maxes something. You either do it explicitly or you do it implicitly and make dumb mistakes; the only reason to do the latter is it lets you avoid thinking about the unpleasant parts of your worldview. The view implicitly underpinning "Venice for the Venetians" is "One of this handful of sophisticated upper-middle-class Europeans is morally worth far more than dozens or hundreds of boorish tourists"

> The view implicitly underpinning "Venice for the Venetians" is "One of this handful of sophisticated upper-middle-class Europeans is morally worth far more than dozens or hundreds of boorish tourists"

Not at all, this is an oversimplification trying to equate and analyse a social issue in purely economical terms, which is inhumane and unempathetic.

A place like Venice, or Lisbon, or Barcelona, so on and so forth, are only desirable exactly due to generations of people who lived there and built them up. You are trying to force a pure economical view on this issue which I completely disagree with. It's not that morally the residents of Venice are worth far more than tourists, it's that these places only became somewhere tourists would go due to the collective effort of generations of people who are now being forced out so some tourists can pass by, consume and part away with their money after a week. Leaving nothing else in its wake.

Also, the people being pushed out are not the "upper-middle-class Europeans", those have the means to afford living in the city for longer than the poorer ones who are pushed out first, those poorer ones might be elderly, or low-income workers (such as is in Lisbon the past 5-8 years, and Barcelona maybe for longer) who might have been born and lived in those places until a rich landlord purchased a bunch of flats to rent out for 3-5 months of the year on AirBnB and make a buck. You destroy local communities to allow what? Some economical activity due to tourism and enrichment of a wealthy class.

Yes, morally I believe that's wrong, you are min-maxing the return in purely economical terms to a class of people who in large part had no hand in creating what they are profiting from, indiscriminately hollowing out cities for pure profit-seeking motive with no regards for the social issues that will be created in 10-20 years for those people who are forced out just due to a lack of regulation of AirBnBs.

The issue is not boorish tourists, the issue is allowing the rental market be completely distorted in favour of short-term rentals for a tourism industry that exists solely due to the generational work of whomever built those communities and cities, and who actually live there, day in and day out.

If you don't believe this is fucked up I feel we have very different moral compasses...

> only desirable exactly due to generations of people who lived there and built them up.

Disagree. Much of what makes these cities so desirable was built on the backs of vast numbers of poor peasants in the surrounding countryside, or looted from foreign lands, or generated by travelling merchants, or built by people who were expelled from that city between then and now.

And even if someone does happen to be descended from some distant ancestor who contributed something to creating a place, well, so what? Just as no-one should be punished for the crimes of their ancestors, no-one is entitled to be treated better than others just because their ancestors did something good.

There seems to be a personality type that is willing to entertain wild ideas and ignore "reality". Sometimes that results in actual new possibilities that nobody else was crazy enough to consider before. So there is potential value.

But often it just means ignoring reality and reallocating the resources that are available in favor of a few.

Tesla was a great company because they proved that electric cars could not only succeed but could accel (and accelerate! ... I do love seeing a family car kick a stupid ICE car's ass on the dragstrip.

But they pushed too far, promoting self driving at the cost of lives.

And for the anti-government people out there, Tesla would not exist had it not been for government funding.

Even so, the guy at the helm had enough chutzpah to believe his own crazy big ideas and follow through with them. Unfortunately, he followed through well beyond the real successes and far into lunatic territory.

I don't know what the actual economic term is (or if there is one), but what I am referring to is when a loss-running firm undercuts the competition until the competition no longer exists, and then because they have a monopoly, charges more and/or delivers a worse service than previously.

Musk was a visionary, but a visionary without funding is nothing. His funding for Tesla came from the US taxpayers in the amount of $451 million.

This turns out to have been a good investment for the US and Tesla and arguably the world in general, because it proved the capability of electric cars (as well as their market desirability).

But make no mistake, without that investment and the success of Tesla, Musk would not have a fraction of the "success" he appears to have now.

SpaceX is something to appreciate as well, but as they say - it takes money to make money. Building a space company is even more crazy than an electric car company. So to do that, you need a TON of money or a lot of powerful investors (or both).

Musk should have sat quietly with his successes in Tesla and SpaceX, but instead it seems he has bighead syndrome. He believes his wealth and success means that he is an expert in everything.

> His funding for Tesla came from the US taxpayers in the amount of $451 million.

This is wrong. Tesla was founded in 2003. Around 2009 they received a loan from the DoE for $451 million to build the Model S but this money they only started getting around 2011 if I remember correctly.

By that point Musk had already put in 90million of his own money plus some more money from friends.

The government just happened to have a program for this and Tesla took advantage. Tesla re-paid this loan in full ahead of schedule, so the DoE made a nice profit on this.

And btw, the same program made much bigger loans out for GM/Ford and they still have not paid it it back.

> But make no mistake, without that investment and the success of Tesla, Musk would not have a fraction of the "success" he appears to have now.

I don't think this is accurate. By that time Tesla had a number of funding option. It might have cost stock payers more or Tesla would have to pay more interest. Tesla might have been slowed down slightly but I don't think it would have changed as much as you suggest.

> SpaceX is something to appreciate as well, but as they say - it takes money to make money. Building a space company is even more crazy than an electric car company. So to do that, you need a TON of money or a lot of powerful investors (or both).

SpaceX was almost fully self funded. Musk initially wanted to invest 70 million $ but had to invest an additional 20 million $. He got some additional investment but not that much.

Until the received the COTS program they had very little ability to raise cash.

> Musk should have sat quietly with his successes in Tesla and SpaceX, but instead it seems he has bighead syndrome. He believes his wealth and success means that he is an expert in everything.

I think he believes he can become an expert in everything if he focuses on it.

> This turns out to have been a good investment for the US and Tesla and arguably the world in general, because it proved the capability of electric cars (as well as their market desirability).

Did the taxpayers get shares for this investment? If not, I fail to see this as an investment … it would be a gift to Tesla shareholders.

I think/hope the crime companies are a minority. I wish the industry would do more to root them out, but I guess there's no profit motive in it. I've never understood why the government didn't come down hard on Uber/AirBNB/etc. and those who invested in them. (Isn't this why RICO exists?)

The venture capital investment rounds are absolutely Ponzis.

Every round is for a higher valuation, and so every investory knows they are paying more for the same number of shares as a previous round. But they believe that a future scenario (investment round) will increase the valuation such that their investment will become profitable.

Show me _any_ startup where an investment round was at a lower valuation than the previous round. Unless you can do that, and show that the company was currently profitable, then it is a Ponzi scheme.

Why would an investor invest in something that has no profit? They would only do that if they believed that in the future there would be enough profit to increase their value given the time cost.

If you look at Uber, the amount of investment, and the 8+ years of zero profit, the only conclusion you could reach is that each round believed that there would be a subsequent round that would increase valuation and provide a profit for them.

Offering drivers generous bonuses to sign-up, encouraging them to take on loans to buy cars (even extending credit - as they did here in India) - and then pulling it all away, leaving poorly educated drivers with loans they can’t service anymore - that’s the definition of recruitment.

Uber, AirBnb, Door dash etc. have added tremendous value to my life and society in general. That’s not a Ponzi scheme. At worst you could call it a social wealth redistribution program of sorts.

Look at Uber's funding rounds. They have had round after round, and each round increases the valuation such that previous rounds' investors make a "profit" (their stock value increases). Yet, Uber isn't making a profit.

Airbnb did the same on a much smaller scale.

Ignoring the investment round topics of both companies, they also both made their actual financial progress by blatantly ignoring local laws.

Airbnb walked right past hotel laws even though their hosts were clearly party to those laws. Uber drove right past the local taxi laws.

On the human side, life got far worse for people living in cities where Airbnb became popular. I lived in Amsterdam for a few years as Airbnb was growing, and very rapidly you started to see people buying apartment just to rent out for tourists through Airbnb. That pushed apartment rates up, and it added a lot of really shitty short term visitors to the neighborhoods.

Every tourist destination has confronted this problem, and now many laws exist specifically because of Airbnb. I would not tout this as a "success".

And in some parts of the world, the ability to sign up and become an Uber driver has resulted in harm to passengers. Prior to Uber, many of these places had regulations which made it difficult enough to become a commercial driver that no driver would risk their business for the opportunity to rob or rape a passenger.

If you take out all the crime (unlicensed taxis/hotels) and subsidies, is there any value left? I never used them but I've seen a lot of people saying that e.g. airbnb isn't actually any cheaper or easier than a hotel nowadays.

Once in a while you can find a good Airbnb which you would not find an equal to in the many hotel apps. But over time, more and more legitimate 'homestay' rooms can be listed on real hotel apps.

I'm a hotels.com or booking or agoda user, and I've booked dozens of stays in the last few years. My partner has some hippie fetish which leads her to start with Airbnb in searches for stays. 9 times out of 10, the Airbnb opportunities are far less than they appear to be. Less often, the hotel options are.

The ancient original Airbnb idea was good - someone comes and stays at your place (while you are there), and you make a little extra money while they get a decent place to stay. But unsurprisingly that got corrupted into maximizing profits. Airbnb also recognized early that they could not make $$$ with their original idea, so they pivoted to the broader "take my whole apartment" concept which is the current norm.

You mean, the fucked housing and rental markets? Or perhaps you were referring to the rent seeking on the restaurant industry? Or do you mean the "contractors" who subsidize Uber with their cars? Or was it the taxi drivers whose livelihoods were destroyed?

The tide is going out: higher interest rates mean the economic decisions of the last 15 years will need to be recomputed. Cheap money is no more. Easier to earn a good return with a CD or bank account even.

Where good return == lower than inflation rate. TIPS are positive rate now but unless in a tax advantaged account could fail to keep pace with inflation too.

TIPS are not the everyday investor's product. You need to hold them to maturity to beat inflation - and few people are willing to lock up their money for 5, 10, or 30 years. In major market drawdowns like the ones we've seen, TIPS returns have not done well.

A high yield checking account is a better product for the typical investor - assuming they understand APY and that the yield resets periodically (monthly).

I-bonds (lots of restrictions apply) are the instrument that loses the least value in this macro. Bonds have seen a spectacular haircut over the last 18 months [1]. You’re up against duration risk. Treasuries are only federally taxed, CDs are fully taxed, so a strategy some adopt is a short term treasury ladder until Fed go forward benchmark policy crystallizes (which leads to more firm asset class pricing information), at which point you possibly rebalance or reallocate.

There's a pretty low limit on the amount you can invest in ibonds per year. It's in no way a solution for people looking to protect assets in a bear market.

I had a similar question, and I would really like to know how "cumulative losses" are calculated.

As someone else posted, it is possible that, in addition to equity financing (the "amount raised" number), the company also received debt financing, and they've spent most of that, but I don't think that can explain everything, e.g. the huge delta in Teladoc Health only raising $170 million but having $11.2 billion in cumulative losses.

Doing a little searching, it looks like Teladoc recently took a $6.6 billion goodwill impairment on its acquisition of Livongo in 2020 that it did for $18.5 billion. The original acquisition was for "Livongo shares will be exchanged for 0.5920 shares of Teladoc plus cash of $11.33 each consideration per share." So if a lot of the merger deal was done with inflated Teladoc stock, and then that stock fell, it would be considered a loss in a particular quarter, but I feel like it's weird to call the non-cash charge part of its "cumulative losses".

In any case, the numbers are at least "funny" in the sense that they're not comparing apples to apples (or, more accurately, "cash to cash").

Yeah looking into it a bit, my guess is the real explanation is that this is due to sloppy math on the part of the original authors, especially since they neglected to even address this most obvious / basic question.

It's directly addressed in the linked Marketwatch article that the table comes from, in the 2nd and 3rd paragraphs after that table. The "Funds Raised" column is startup funds. It does not include additional funding rounds, selling stock, debt, etc.

I'm pretty sure "startup funds" would include additional funding rounds (i.e. Series B - whatever). But you bring up a good point, I'm not sure if it includes, for example, funds raised in an IPO. But it makes 0 sense to include funds in private rounds and not includes funds raised in an IPO - they're both equity purchases in the business.

It would make sense to not include debt raises, because as the article points out, those debt raises need to be financed. Still, not at all a useful comparison without more detail.

A very large chunk of GAAP losses are attributable to stock comp expense (a quick and easy way to check cumulative profits/losses is looking at the balance sheet’s equity section for “accumulated deficit”) which still gets counted as an expense but since it’s non-cash it’s not a drain on whatever the company has raised. If you look at Uber’s last three FY’s, they’ve cumulatively reported losses of about $16 billion, and stock comp has been about $6.5 billion of that. For the vast majority of public companies this isn’t as material but for all these VC-backed, Bay Area-type tech companies they have this systemically dysfunctional culture where they dole out stock and options to no end.

If stock-based compensation information is made public to investors, what's the problem with it? I don't see why compensating people in stock rather than cash makes it a "systemically dysfunctional culture".

I think the right way to handle that in a chart like this would be to include the stock comp on both the “funds raised” and “cumulative losses” columns, or neither of the columns.

When you issue stock comp, you are trading dilution for money, just like you are when raising from VCs or doing an IPO. The money is just spent on paying an employee immediately instead of sitting in the corporate treasury for a while.

If you include the spending part of the stock comp as a “loss”, but don’t include the creation of that stock as a “raise”, you end up with these nonsensical results.

Why does Uber need debt? They’re a software, logistics company. It makes sense for a real estate company to be loaded with debt as that’s the nature of the beast. But I don’t see an argument for logistics.

Their product isn't some software, and they're not making money by selling software or a software-based service [1], so they're not a software company.

They're selling taxi rides, the fulfillment of which is outsourced to semi-independent contractors. Therefore, they're a taxi company.

[1] Yes, they have an app – who doesn't, today – but clients aren't paying for using the app, they're paying for the service arranged via the app.

As I understand it, they claim their worth comes in the algorithm getting someone to their user more efficiently. Still not seeing why all the leverage. For a cab company I suppose it’d be car and insurance/gas costs. This gets more fuzzy because I remember cab companies renting vehicles to drivers per day. I think the rent was the companies effective share of the rides.

But the whole point of "cumulative losses" is that one would assume losses means revenue - expenses. If "revenue - expenses" is a negative number that is far larger than the amount you have raised, how are you not bankrupt yet?

Uber has a market cap of 58 billion (cf. "$25.2 billion funds raised"). Teladoc Health has a market cap of 5 billion (cf. "$0.17 billion funds raised"). The Funds Raised column in the article does not seem to include stock issuance.

Say you received 1,000 when graduating high school. You then got a job making 100/month, signed a lease and moved out of the house. You have expenses of 180/month. How long before you are destitute?

It's a combination of the two reasons cited by others here.

1. They may have revenue which is adding to total cash pile; and

2. They may have taken on additional debt

Maybe obvious, but probably worth repeating is that raising capital does not raise debt for your company (i.e. you're selling off a piece of your company, not taking on debt which you have to repay). I'm assuming that the "Funds raised" column is the amount they've taken in venture funding, and not debt. If it does include debt, you can ignore point #2.

Raise money. Use raise as an asset to secure credit. Accrue liabilities during normal business operations. Fail to generate revenue and raise more money and credit. Demonstrate growth without profit. Rinse, repeat.

They used their high stock price to buy Livongo, and then did massive write downs on it when it ended up not being that great (~$9 billion in total). They had two quarters in a row where they did good will impairments of 30-40% of their market cap.

Depends a bit on what failure means. "Sold for less than raise" perhaps counts?

My guess is one of the first two, Uber or WeWork. Uber doesn't seem like it's cheap anymore as a customer. How is that going to compete? And WeWork is already competing with standard rent-an-office businesses that are worth a lot less.

Not sure about Robinhood being on this list. They actually have billions in cash on hand right now.

They also have some valuable IP that a lot of people don't give them much credit for. One example being a brand new, in-house trade clearing system. This is similar to rewriting an IBM core banking system from scratch.

Spoiler alert: they had help. Robinhood is a wolf in sheep's clothing - they are controlled by, and beholden to, criminal enterprises such as Citadel. This "in-house" trade clearing system is actually Ken Griffin's personal honeypot. It is built for one, and only one purpose, and that is to fleece retail investors at all costs while simultaneously creating the appearance of being retail's champion.

It's a neat trick, and I'd almost respect their enginuity if they weren't robbing people blind. I wouldn't touch Robinhood's products or common stock with a 100 foot pole, and neither should you.

Edit: See my other comments below for an idea of how/why this works.

I also would ever use Robinhood instead of a reputable broker like TD Fidelity Vanguard IB etc. But not for the reasons you stipulated. Back office systems aren't put in place to "fleece" anyone.

Back office systems are exactly where Citadel, the market maker, could put a tiny little window to peep at data they shouldn't, so they can frontrun every trade retail investors make!!

Wouldn't it be wild if a market maker also controlled a hedge fund, and also had members installed on regulating bodies, but then like, PINKY PROMISED they wouldn't abuse their positions? And then imagine if the SEC were complicit because it's run by an ex-Goldman henchman?

I really hate to do this because it sounds lazy, but I strongly encourage you to watch The Problem with Jon Stewart's episode on this. He explains it very well, and it's a lot of information, so if you are genuinely curious, I would highly recommend it. It will open your eyes to a level of criminal activity at the highest levels of our markets that will hopefully surprise you. It explains this, and more.

This is straight out of /r/superstonk or /r/wallstreetbets. The conspiracy theories about Citadel, Ken Griffin and Robinhood rival QAnon levels of culting. I've heard it said that these theories, including GME, are like QAnon for people interested in personal finance rather than politics.

Lol, right, because things like this have never happened before. In particular, the years 1998 - 2008 were devoid of financial crime, and are a decade of restrained, ethical capitalism that we should all aspire to. Gentlemen of Wall Street today are just trying to return us to that gilded age, and any suggestion to the contrary is conspiratorial madness I do say, good chap!

Thank you for pointing out my severe mental illness and inability to think clearly about such lofty matters. I'll go take my meds now.

Well, I suppose there is no rehabilitating cult members. Your reasoning also doesn't make much sense, we can agree that there is financial crime in that time period while also acknowledging that superstonk-esque manipulation isn't happening. You're basically trying to equivocate that just because something in the category of financial crime happened before that it must also be the case that your Ken Griffin conspiracy theory is also true. It's a more general fallacy that is often seen online, not just in this instance.

You very strongly compared my theories with QAnon, which is actual Alice-in-Wonderland level crazy. To compare financial crime theories that (given the precedent) could very well be true , to fucking QAnon is ridiculous, and I found it extremely condescending.

You can disagree, and you can bring up valid arguments, but your posture was offensive and has no place here.

Crime had very little relevance to 2008. I'm sure there was a certain amount of fraud going on, just as at every store there's a certain amount of "shrinkage", but the crisis was a good old-fashioned boom-and-bust cycle.

Right back at you. You're making a whole bunch of assertions which are, to say the least, not widely accepted, and unsupported by any evidence or logic.

That falls under "a certain amount of fraud going on". Yes, there were a lot of bogus AAA ratings going around. But everyone knew they were bogus - you don't get AAA paper that pays a 10% return. Any investment banker from the GFC era who tries to tell you they're a poor innocent rube who was taken advantage of by a dastardly ratings agency is having you on. The people buying the CDOs were sophisticated professionals who did their own analysis and bragged about how smart they were.

"Cumulative losses" is meaningless in the way they are using the term. You need many, many more datapoints to judge the overall health and value of a company. And even after that you are likely going to be wrong in your prediction.

Uber raised $25 billion and is worth $60 billion in public markets today. By what criteria is it a bigger failure (or a failure at all) over Theranos, FTX and thousands of other companies that raised a significant amount of money and are worth exactly $0?

In the same way that Shibu Ino coin is "worth" 4.9 billion - ie, meaningless and entirely fictional; lacking any substantive value.

Uber stock is worth what it is because there are still more fools available to buy it. Theranos failed and was completely exposed, and even the fools are no longer interested.

That's not to suggest that Uber did not do some things very well. They identified a need and provided a solution (mostly software-based), but their actual on the ground solution wilfully ignored local laws globally. Even ignoring legislation and regulation which costs money, they still tried to use loss-leading tactics to win markets. So they burned vast amounts of money to undercut the market.

Had they ever rectified those two HUGE issues, they would be struggling to make a profit. Even not rectifying them, they are struggling. So holding them up as a success is just naive and wishful, but wrong.

Having worked with Nutanix, I would bet on them failing. Their products are consistently medium good. Not great, not terrible, just… “okay”.

The problem is that the competition is getting very good very fast. Nutanix competes with the cloud, which means that as Azure and Amazon get better they get less compelling.

Most of our customers that choose Nutanix previously are on Azure now.

Oddly enough, this can be a sign of an excellent business. Microsoft originally provided some very mediocre products, but in a world fulled with absolutely shit products, being predictably mediocre was astonishing! Before 2000, when Microsoft produced a lemon, they always seemed to recognise the problem and then replace it with something that was crappily useable (and they also had a few products that were actually good).

Your comment makes me think that products and services are higher quality now, so it is harder to compete by being merely mediocre or even “medium good” (as you point out).

> Oddly enough, this can be a sign of an excellent business. Microsoft originally provided some very mediocre products, but in a world fulled with absolutely shit products, being predictably mediocre was astonishing! Before 2000, when Microsoft produced a lemon, they always seemed to recognise the problem and then replace it with something that was crappily useable (and they also had a few products that were actually good).

People in here including me dream of living in an era where there is such a giant leap such as the leap to GUI provided by Win95, or even the revolution of the chip.

If you didn't like being around when Win95 was coming out, I guess living in today's timeline where innovation has reached stagnation must be pure hell! /s

Nutanix's website gives absolutely 0 real information about what they do. There's some fluff about apps, cloud, and transformation - are they a body shop? AWS competitor?

Their core product is very comparable to VMware vSphere -- a system for managing virtual machines on a cluster of on-prem hardware. Nutanix was one of the first to do storage virtualisation, whereby each node provides some local storage that is shared across the whole pool. I believe they were one of the first (if not the first) to offer this as a turnkey product. The initial version was just an add-on to vSphere, but they now have their own hypervisor as well to make it a more complete offering.

These days you can achieve the same thing with VMware vSAN or Hyper-V on a Windows cluster using Storage Spaces Direct. The latter is practically free for organisations that use mostly Windows Server workloads, because those orgs typically license Windows Server Data Center Edition for every physical host anyway. In my experience Storage Spaces Direct was also much faster, especially when used with SSD disks. The protocols used by Nutanix were very inefficient compared to the RDMA and Infiniband capabilities in SMB3. Think millions of IOPS instead of tens of thousands.

In some sense, the cloud provides a similarly abstract view of storage. You ask for a 1 TB disk, you get a 1 TB disk. You don't have to worry about formatting a disk array or securing a fibre channel fabric. There's no "maintenance" tasks to be performed on cloud storage. It's just... there. All the time, with zero effort.

This is why I think Nutanix is in trouble. They provide a partial but good solution to a problem that the public cloud providers eliminated entirely.

Back when I first looked at them 5 years or so ago, they were trying to sell me "hyperconverged infrastructure" which was basically just a thoughtfully designed blade chassis. Their software seemed very nice, kind of a software-defined-storage type thing that Just Worked and by all accounts it did work very nicely.

BUT, and this was a big but back then - their prices were obscene. Vaguely equivalent hardware from Dell was less than half the price and was readily available (Nutanix in my region had long lead times on gear at the time).

Need to add a column with the IPO valuation to answer this properly. I'm guessing when you add that column all of these were massive successes except WeWork which went public via SPAC and their IPO imploded.

Valuation is meaningless from the perspective of analyzing if a company has been a success or a failure. Valuation concerns the players who sit at the poker table and how each and everyone of them managed to fare during the game. The table being the company and the players being the investors.

The OP is right in accounting funds raised vs. losses incurred as the metric to watch for.

The funds raised belong mostly to public pension/private funds and insurance companies, with the intermediation of PE/VC funds.

It was a half-joke, designed to illustrate that goals of successful company and successful IPO dump have been conflated the last several years. Ultimately the poker game as you call it is what the people holding the money care about so...

Ha sorry for not getting it. You are mostly right, but I still hold out that very smart and competitive people might want to do all.

Meaning having their fingerprints on a company that achives the trifecta of being a financial success in terms of profit/FCF, marketcap valuation and also makes a trademark product/service used by everybody.

Would be interesting to see cash flow, which is probably more relevant when comparing against capital raised. If this is EBITDA, then included in those losses for these companies is a ton of stock based compensation which really has zero effect on cash flow.

> "...the business plan of some of these companies was to become so useful to the decision-making class (business executives, government officials, and rich people) that they’d ultimately get some sort of government support."

This! The speculative investors have tasted blood during the 2008 financial crisis and the general public has already been conditioned to accept the idea of "too big to fail". So this music chair game is going to be played for a long time.

> the general public has already been conditioned to accept the idea of "too big to fail".

No, the general public has been made aware that once businesses hit a sufficient level of financial entanglement with people in government, they will not be allowed to fail. The general public was not consulted on this, because it doesn't matter what the general public thinks when something is bipartisan (which is true for all but <10 "wedge" issues.) Handing wealthy people tax money is bipartisan, for example. Handing poor people tax money is a wedge issue.

I've alluded to this in other comments, but these fundraising numbers have to be incomplete. Rivian raised 10.7B, lost 11.1B, and yet they have close to 14B in cash on hand? They've overlooked a lot of fundraising. I'm guessing others have similar mistakes.

Unless it shows the nature of the losses (opex losses? taking on low-interest debt? huge write-off of acquisitions made with stock?), this chart is somewhat unhelpful.

For sites like airbnb it's not possible for the story to be "not real". It's just a website guys, there is no per-unit costs that makes the economics not work out.

Palantir is not going anywhere anytime soon. They are about to sleaze their way into the british healthcare system. Uber is likely to go under, sold for their rider and driver base at a discount value. Airbnb’s bubble has burst. Door dash? Why is even door dash such a popular thing. And why do these companies need so many people to maintain their apps? Should be max 100 devs and everyone else in sales and support.

You can definitely run Uber-scale systems with <100 engineers. Whatsapp was famously run by like 30 people or something. The problem is when you expand your business at the rate Uber has, or any VC-funded startup, in which case you gain massive (absolutely massive) amounts of tech debt in the form of bandaging new features onto old code without proper refactoring. Then you start doing "microservices" and you hire 10k engineers and now you have even more problems, and your infrastructure and codebase expand exponentially.

I think for a good scaled architecture, the keys are: having at most ~30-50 developers, good planning by a few key architects, controlling what's in your database with an iron fist, knowing exactly which bits of data are where and what they are used for, and having strict codebase standards.

However, to really be successful in the goals above, the business needs to support a rigorous software process. Normally, this is where things fall apart, since business people and sales people (who are otherwise great people) will push you to work faster and cut corners to get things done. In the end, they also pay the bills, so if the business isn't run by people who understand why software development has to be strict, then you get sloppy software processes.

You can only run Uber with <100 engineers if you cut out a substantial amount of the systems Uber requires to actually function as a company. Goodbye Fraud, Risk, Safety, Insurance, Compliance, etc. That may be true for things like Whatsapp with a simpler feature set, but is certainly not generally true. For instance, people often underestimate the amount of ongoing engineering effort to stay up to date on changes in tax law in all the countries Uber operates in.

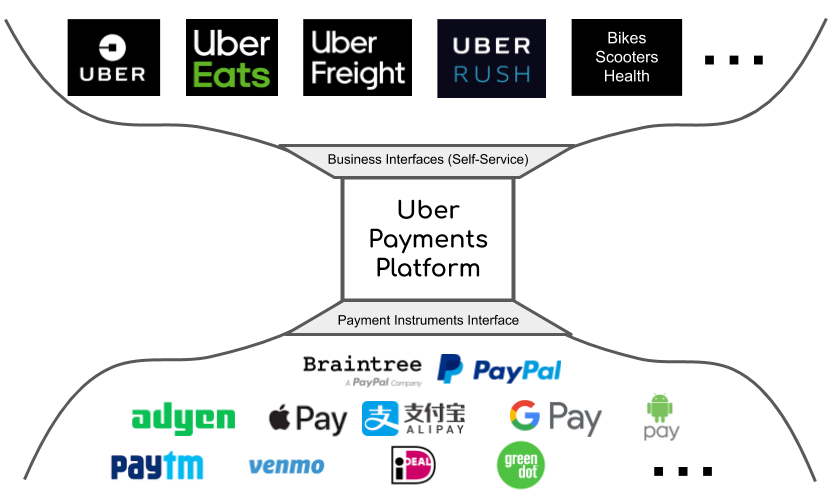

Usually the way these kinds of things evolve is it will start with some business requirement: "We want to launch in country <X> but our existing PSP <Y> doesn't support the country's most common payment method <Z>" (Uber operates in 71 different countries).

So you build out a system to abstract over multiple different PSPs (such as Stripe, though Stripe isn't listed in that graphic so not sure if Uber uses it at all) to unlock new business growth. Then you find out that some PSPs are cheaper than other PSPs, so you can save the business money by supporting additional PSPs. Then you find out that some PSPs are more reliable than others so you can increase availability by dynamically selecting PSPs based on availability and transaction costs etc. etc., layering on complexity over time.

All these things are actually built for very good reason (in this example, built to grow the business and reduce costs), but the reasons aren't obvious to the outside observer. But the work easily pays for itself many times over.

So could you run Uber with <100 engineers? Probably, if you were okay running in just a single country instead of 71. But that would be a very different Uber.

and then there is basecamp and you wonder whether maybe there's "experience" and ... experience. (though I agree that regulations and fitting to markets just requires people)

Uber isn't likely going under; they're going to squeeze and squeeze and squeeze their way to getting by. Lyft is quasi going away (they'll be acquired), which will further benefit Uber's survival chances.

Uber's sales hit $29b with a $2.2b operating loss, over the past four quarters. It won't take much to keep squeezing that loss further downward to the point where they can trivially float it indefinitely. They continue to become more dominant in their space, not less. If the US economy crashes hard (and nobody can predict that accurately at this point), that would be the only serious risk to change that.

Yes and Palantir is deeply embedded into many US government agencies. They are somewhat protected by this, but they may need to slim down to justify the bailouts they might receive.

I argued with my doctor that I would not tell them confidential health related information that could have consequences for me, or held against me. They said "do not worry, it is entirely confidential".

I did not share the information, told my doctor lies (as I said I would if they were putting their notes in a database).

{kind=link}

They also have a ton of debt. Hopefully there isn't a balloon payment / interest rate adjustment coming soon. Assuming they're not heading to some financing cliff, then borrowing at less than inflation rates, and using the money to buy market share was probably the right move.