The model described in the book does work. Spend less than you make, invest the excess in long term assets that have compounding interest rates above the inflation rate. It does produce millionaires. It also requires tremendous discipline over a long period of time. The math is relatively simple, the behavior is not.

While the millionaire described in the story had $8 million in assets, you will find almost no one "next door" with 10 to 100 million or a 1 billion. That level of wealth requires a return on investment that can't be achieved using the earn and save model. It usually requires creating/controlling an assets that can grow in value many orders of magnitude faster than the stock market (real estate, businesses, intellectual property).

> Spend less than you make, invest the excess in long term assets that have compounding interest rates above the inflation rate.

It does work. But the cost is your life.

My issue with the whole idea is that the wealth comes in the latter years of your existence. Decades of work have dulled your curiosity and desire to enjoy your wealth. You don't need much to exist and could survive off a more humble nest egg.

Wheelchair wealth is considerably less valuable than wealth when you are young.

... not really. savings is a percent, you can set it wherever you want. the math works out just the same only over more/less time.

you don't have to be a frugal miser, and you don't have to spend like it's burning a hole in your pocket. saving a responsible amount isn't going to dull your curiosity for decades.

whether you consider it intentionally or not, when you choose how much to save you're also _directly_ setting your future wealth. the most prudent thing to do is optimize _both_. how 'well' do you want to live vs how much wealth do you want and by when.

what actually costs you your life is spending unnecessarily in your youth, which implicitly sets your future wealth nearer to zero and burns the time to fix it.

“But the cost is your life”: cultivate less-expensive tastes and hobbies, and live a great life while saving up for when the silly tech money stops rolling in (by your choice or not).

In fact, I’ll be so bold as to say that the more mind-expanding ways to spend free time involve spending less money than their competitors.

Want to fly? Join a gliding/sailplane club instead of getting a powered flight license and buying a Cessna. Love good food? Learn how to cook new dishes instead of finding exciting new restaurants. Into high-performance luxury cars? Rent a different one for a long weekend a couple times a year instead of leasing the same one to sit in traffic for your boring commute. Like to regularly update the look of your living space? Learn how to lay tile and do upholstery instead of shopping for more crap.

My husband chose the first one (gliding vs. powered flight), and I’ve fallen into the second one. Both have significant financial benefits, but also health - gliding club involves a lot of scurrying around the field to help the other pilots, and just about anything I cook at home is healthier than a similar dish from a restaurant.

I still have one stupid money-sink hobby, downhill skiing, but have found less expensive ways to enjoy it — day or weekend trips by train to an ok ski area instead of a week at higher-end resorts.

You are absolutely correct. It sounds like we have different ideas about the amount of free time required.

When retired or semi-retired (thanks to youthful wealth), you can do a lot of cheap but time consuming things like backpacking overseas, hiking the pacific coast trail, spending a summer diving in Cuba.

Indulging in my hobbies one day a week in between running errands and going to the gym just feels like a watered down version.

I makes less than 100K usd per year. I have a wife (who also makes less than 100K), a car, a kid, and hobbies. I don’t live in the valley, or even the United States. I work 8 hour days, employed by somebody else.

I should be a millionaire by my mid thirties unless the stock market explodes. I don’t think I’m all that frugal, but we do try to save more than we make and live within our means.

I do recognize that I’m extremely fortunate - I have not suffered any significant setbacks in my life, my health is relatively good, and I have a good family structure, all of which have been immeasurably helpful.

Doesn't ring true for me. Some of my favorite things to do are free or very cheap. Biking around town or on local trails, taking the dog for a walk, changing the oil in the car - yes, really.

I love to travel, too, but you can go amazing places for hundreds or a couple thousand dollars. You don't have to spend much to have an amazing life and go amazing places.

It frustrates me to see my peers who earn far more than me feel stressed about money and feel that they have to do very expensive things or else they're not living, but what can you say?

The question is: do you need money to live a happy life?

My opinion is that you don’t. But to each their own.

Maybe some people are saving because it makes them happy. In the article Nassim Taleb is quoted saying something about how it’s dumb to accumulate so much wealth but still live in a starter home (not sure if this was directed at Buffet or what). But sometimes people just feel happier having a cushion, or it Buffets case, feel happier having investments pay off.

I think it is possible, but not if anything goes wrong.

For instance, I used to live off of ~300 / month in the US by living mostly in forest. However, after having a kid my wife demanded regular housing. I could divorce her and go without housing again, but then the state would impute my income and order child support at 20% of the income I _could_ make (which is very high) even though the actual cost of the necessities for a child is minimal (maybe 200 a month maximum). If you fail to pay you will be charged a felony and go to debtor's prison.

So the answer is in many occasions you and your family could live a happy life on basically nothing, but you would have to live with the fact you will be imprisoned and lose all your professional and driver licenses and have all your land and assets seized because you don't earn at your imputed income.

For this reason I abandoned a fairly happy life living off almost no money and instead slave away at a keyboard dreaming of the life that once was. Just don't make mistakes.

> They say money can't buy happiness, but do you know what money can buy? A jetski! And when have you ever seen someone not happy on a jetski. You'd be smiling as you ride that thing into the pier!

> The question is: do you need money to live a happy life?

IMO you need a certain baseline amount. There are some necessities that you need to be able to afford (hard to be happy when you're starving). In the USA, I'd say you also need to have a cushion in case of some unforeseen medical emergency, in other places that may not be as necessary.

At some point the question is - "is it really worth it?" Sure, if you save 10-20% on a regular basis, you're just being prudent. But if you go out of your way to save 50-80% of your income and lower your quality of life significantly, just so you can have more money in your investment account, or so you can not go to work (but still live that same extremely restrictive lifestyle)... it really doesn't seem worth it to me. But some people obviously disagree.

I'm one of those that save/invest 70% of their take-home income. It's not about frugality at all - I would gladly pay for an increased quality of life - but it's simply not on offer.

Past a certain threshold, a threshold well within the reach of western upper-middle-class households, the exchange rate between money and the quality of life becomes essentially zero.

What's left are pointless status seeking games, scams and useless trinkets. The Bible's Book of Ecclesiastes describes it poignantly:

> I denied myself nothing my eyes desired; I refused my heart no pleasure[...] Yet when I surveyed all that my hands had done and what I had toiled to achieve, everything was meaningless, a chasing after the wind; nothing was gained under the sun

Fully agree with you. I believe a few years ago there was research stating that roughly speaking, 70K per year (in spending) is the happiness threshold.

Any spending above it leads to no, marginal, or only temporary extra happiness.

I put that bar far lower, personally. We already have the stuff we need and don't enjoy shopping. We're basically stuck at a particular spending level whilst income grows over time. Saving a large portion of our income is effortless, and not at all a sacrifice of quality of life.

The secret to life is to not want so much. It makes life so much easier and better.

The study is cited frequently but it’s misinterpreted frequently or in a disingenuous way. It merely says that among people earning so much, more money does not contribute as much for happiness. This has some sad realities: by and large the wealthier / higher income are much happier than our poorest, and giving money to our poorest have the largest gains in aggregate happiness. This is consistent with other studies on happiness - money makes everyone a little happier at least, and not having enough is a big problem. Sure, other studies also show how our poorer may be fairly happy and connected to communities and all that, but if you take a look at the data they are from decades and decades ago and include retirees as well.

There is certainly an argument that diminishing returns is true in terms of happiness, but at the same time incomes explode beyond a certain point and data points become a lot more sparse and difficult to correlate back to the population.

It’s quite difficult to not want so much given much of social pressures in developed countries are around consumption. This, the criteria to me is more broad than merely not wanting much - the question is about resisting social pressures and to be comfortable and thankful, and this seems to be inline with the data so far on happiness and social relationships as a whole (happy couples tend to have certain habits and innate drives prior to marriage like being selfless, gracious, etc for example)

I think the direct implication of saying that 70K is the point of diminishing return is that people making less than it are less happy? I think the study therefore is consistent with what you're saying?

For very high incomes, even without research data, I still find it only logical that excessive spending doesn't add much to happiness. This is due to almost every product/service not linearly improving as you spend more on it.

A sports car is awesome but after 2 weeks you realize it still only takes you from A to B, and you internally normalize it. You can buy 30K worth of audio equipment but it will not sound 30 times better than 1K equipment, more like 5% better.

Note that I'm purely looking at it from a spending perspective.

As for societal pressures, I disagree. There's a lot of room for a compromise here. For example, our expenses on daily consumables is zero. We don't do Starbucks, going out for lunch, or any of it. Zero.

Nobody is pressuring us to make those daily expenses and by looking at us, you can't tell whether we do or don't. This alone is a considerable monthly savings.

We may use our clothes and shoes twice longer than a typical person, yet the wardrobe is large enough that absolutely nobody would be able to tell. Or care, for that matter.

When you enter our house, you won't see some stripped down project by a frugalist. In fact, it is above average luxurious. We have furniture that is of such quality that it is effectively ever lasting. We have very high end electronics, not budget stuff. And so on.

We may even appear richer than average whilst spending less than average. So the societal pressure is zero, because we don't appear poor or poorer compared to our peers.

Cut daily expenses, buy quality and utilize the longer lifespan, put this delta into additional savings. Spend part of savings to lower cost of living (mortgage, energy bill), and get even more savings.

The difficulty isn't for folks like you and myself - curtailed, very conspicuous, TCO-conscious consumption is not that hard if one has the brain cycles and will to defy a lot of social norms. But given the efficacy of advertising campaigns and how spending tends to go up with income it's clear that people spend more on average when they make more money even with more time and brain cycles to spare.

As someone that's had a great deal of difficulty justifying a lot of longer lifespan timeline consumption patterns due to moving constantly weighing living circumstances and career I'd say that difficulty varies considerably for households even when one's aware of the TCO. I'm not going to tell an undocumented migrant family that they can just save more and spend less with more conspicuous consumption like buying a reliable econobox car like I did. Decisions and habits are also much easier when one has a partner or support system aligned with one's longer term goals and habits. It seems quite tone deaf to outright declare all of these factors are simply "easy" because it is easy for one's own intrinsic and extrinsic factors.

With "easy" I mean that our strategy does not deny quality of life in any significant way. That's what got this conversation started: the perception that saving a good portion of your income is painful. A massive sacrifice. It isn't.

I started saving at age 6, on a 1 guilder (I'm from the Netherlands) weekly allowance.

When I landed my first job, still single, low income, I still saved 30%. I save significantly regardless of income. This to say that I'm not some privileged armchair commenter. I come from the lowest of the lower working class, and have plenty of experience with poverty.

So it's not tone deaf, it's an attitude. Which indeed most people don't have. That's a lack of education or awareness. Not a matter of it being difficult. A few minor tweaks do wonders.

I do agree with one point: it won't work if you don't have a partner that aligns with such a strategy.

Maybe, but most people who do have the option to save 70% of their take home pay don't. Perhaps our definition of what it means to live comfortably is partially to blame. I know a family of 10 that live very comfortably in a small 3 bedroom home, but most people wouldn't define it as comfortable for themselves.

same experience here. i can afford everythihg but i dont need much. i dont think people understand what kind of stress relief is to say that u can live the life you want for 30-40 years without having to work.

A lot of truth to this comment. I can’t believe the amount of money I wasted in my early 20s on…junk. Things that, with the benefit of hindsight, actually brought me no pleasure at all.

I’m glad I realised this, and I totally agree - once you realize that consumerism doesn’t materially improve your life, your “minimum income threshold” drops considerably.

For me, the biggest exception is travel, which really adds up if you want to take a couple of overseas trips per year.

There's a saying on the fire subreddits 'live the life you want, and save for it'. No one is suggesting one should live a miserly, miserable life just so they can retire in their 30s.

For me, FIRE is a side effect of trying to live a fairly simple life with little impact on the environment. I don't deprive myself. I genuinely struggle to find things worth spending money on.

Very little gives me more pleasure than seeing my investments and net worth grow. Certainly very few things I could buy. The sense of peace and security it gives is worth more than any gadget.

The easy way to increase your savings rate is to save most of your raises. Most people working in decent jobs will get raises as they gain experience or increase their billing rates. Certainly, I expect most people on HN working in tech to make significantly more in year 5 than year 1.

If you can save most of that, pretty soon you'll have a good savings rate and pretty soon have some good savings.

Also, when you start thinking about retirement and look at rules of thumb about savings amount vs income, you can discount your income significantly if you have a high savings rate. (Looking at needed savings vs predicted expenses is a better methodology though)

No one says you have to save 50-80% of your income. The savings rate in the US is 5-10% historically (ignore the 33% spike in 2020). If you're saving 10-20% you're well ahead

I suspect that 5-10% number is actually a bit deceptive - a huge number of people are saving 0%, so among those who do save, the average must be significantly higher.

And I tend to agree with the conclusion of the article - what's the point in saving that money if one has to live on a shoestring budget to acquire it? Specifically the "work all your life, end with $8 million" case. FIRE is different, with the value being the option to stop working much much earlier than 65 years old.

Hard in the "lots of elbow grease" sense of the word. Maybe also in the "unlikely for you, personally, to have the perseverance for" sense, for a given person.

Not hard as in conceptually difficult to implement.

Security. Knowing you have the wealth to subside on if need be is really nice. Some people call it “fuck you money” which is freedom.

It’s funny they reference Taleb here but he also makes the point that can’t be “cancelled” and is “anti-fragile” precisely because he’s rich and depends on no one.

Depends. There’s a fair bit of value in knowing you have more than you could ever possibly need your whole life.

Like say you spend $500,000 a year and have $10 million, which earns about $700,000 in returns. And you’re happy at that level of spending.

You then have massive security your whole life. Whereas if you time it to run out on time, a reversal could leave you destitute when you’re least able to recover.

Past a certain point it’s hard to think of what to spend on unless you step up to much more expensive things like personal jets etc.

The point of dying a millionaire is that it is really hard to plan your finances such that you die with exactly zero dollars. Because investments are so variable, you want to choose a plan that will likely end up with too much money because that avoids complete disaster in the bad cases.

When I'm dead, all the money is going to charity. Generational wealth is a cancer.

There are financial instruments if you want to die with nothing while having plenty of money when you are alive. If you think it is a terrible thing for a grandparent to want to leave money for their grand child's college tuition, then I'd encourage you to make sure you don't help your grandchildren, but it is important to some people even if it isn't something you want to do.

> Annuities require more starting wealth than safe retirement with equities.

How would you create a "safe" retirement (meaning you won't outlive your money) and still end up with zero at the end. A "safe" retirement implies you are going to have money left when you die unless you spend you last dollar and then commit suicide.

Annuities are the only option if you want to end with zero. But you can instead obtain an amount of money that will almost certainly not go below zero when invested in equities and then donate the remainder upon your death. This amount of money is lower than the amount required for an annuity.

Thus, the distinction between "I want to die with precisely zero dollars" and "I don't want generational wealth transfer".

People loudly decry inherited wealth because it is anti-meritocratic and we're raised with delusion that our system is ostensibly one where wealth is related to merit.

I suspect that most people decry subsidized inherited wealth through things like stepping-up the cost basis for inherited wealth. Generally, I don't think people have a problem with parents giving their kids gifts in some form - though I do acknowledge that there probably is some notion of what is considered a (un)reasonable upper limit.

Most peoples biggest asset is their home which just costs more in property taxes and doesn't provide much benefit because they still need a place to live, preferably near their workplace.

I don’t get what you mean. I have no children, am in my 50s, and still try to maximize my wealth to the extent possible while still having the particular lifestyle I like. I work hard because it’s fulfilling and I work to generate wealth so I’m not screwed over after one health mishap.

Your second paragraph hits the nail on the head. Income is scalable, saving is not. Expand your income, and invest. It's all a lot easier when your income is pumping.

In my country (Germany) afaik a little over 10% of the population are at least millionaires. So I think the likelihood to have a millionaire living next door is quite high.

Anecdotal (but nevertheless true): I have (at least) two millionaire neighbours (less than 3 doors/gates away). Both won the lottery - one euromillions and one national lotto draw.

And if we are talking average income, then everyone on this side of the village is a millionaire simply because of those two. However, most of the rest of us seem to struggle daily.

There is some chance that the bank owns their house, or at least some sizeable fraction of it. Mortgages are more common than houses that are paid off.

A friend of mine "retired" from the military at 38. She joined right out of high school. The Navy put her through med school, then she served as a ship doctor for over 10 years, traveling to dozens of countries. She "retired" with a military pension and an MD, having never spent a penny on med school. She works basically part-time now at a local healthcare provider.

Did that come across as jealous? Well, I am. We all told her she was stupid to join the military, and now we're all still paying off student debt, and she's livin' her best life. :(

If it makes you feel better it sounds like your friend got the golden path; VERY few people hit the milestones and get accepted into the programs that allow that career path. STA-21 and/or the Public Health College were in that path if she got retirement credit for going to school and there are very few spots in those programs.

I know the feeling. But that doesn't mean that you were wrong, or that your advice was bad. It's safe to recommend your friends not to play the loterie if the goal is to derive predictable revenue. It doesn't mean that everyone lose at the game.

Your friend and people drawing conclusion from her anecdote will end up with beliefs typical of the Gettier problem.

Correct me if I'm wrong in my understanding on vocations, but didn't it also require quite a bit of luck that she got to take on this vocation in the Navy?

If you are a decently talented software engineer and you can't match or exceed a non-specialist MD in earning power then you are doing something wrong. Especially in the current market.

Excellent comment. I’m now 70 and well-to-do. But I was a fool to go into private enterprise with all its interpersonal dishonesty. Government jobs at the national labs had superior NPV’s— the pensions are absurdly expensive taxes on struggling workers when carried out to the 85-year typical lifespans of workers. There were layoffs, true. But I understand the psychology and passivity of persons who managed to get themselves laid off.

You also have the choice to take action to avoid risk. That choice is not available in the military. You're trading a lot of freedom over those 20 years. (Did I mention how expensive getting divorced is?)

you guys are kind of using NPV ambiguously. You mean that when you retire at 38, the NPV of your retirement plan at that point (for when you are 39, 40, ... etc.) is $1.3M, and if you haven't retired yet then it's really a FV? what discount rate are you using?

or did you mean the NPV when joining at age 18 is... see what I mean?

Military retirement is worth like a minimum of ~$700k for an E-7, before tricare. It's worth like $1.3M for an O-5. People who seperate from service at like 12 years astound me.

Edit- People who seperate thinking they can earn more money on the outside. People who seperate for family, mental health, or similar reasons make total sense.

I separated at 11 years from the AF as an air traffic controller; September 2023 would have been 20 for me. For the past three years I have been working for home as a senior data scientist - my life has been far better as a civilian.

RPA / Drone flying community is the exception. literally doubled income overnight trading a uniform for polo and khakis, same job, same trailer, same airframe, different airspace

Wait, so are you saying there's non-military people flying drones that are flying in other countries? Although I suppose that last bit is an assumption.

Yes I always considered reenlistment to be committing to 20 years minimum. I got out after 4 years, but some of my friends stayed in because they were lazy and institutionalized lol. Then of course they decide to get out later because they hate it. Two of the worst decisions they’ll make.

It works out pretty well I've been told. But there are plenty of dead ends in Federal service, where people are underutilized and undervalued, but last it out for their pension. Some jobs just don't exist in commercial settings, and it can be really hard to re-adjust to new work.

You can start drawing a DOD pension after you've worked for 20 years (so potentially as young as 37). That also gets you tricare (health insurance for you and your family).

It's not rare for people to double-dip: do your 20 in the military, then go work as a teacher or DOD civilian or something that'll give you a second pension.

If you don't blow all your expendable income on a sports car financed at 30% APR, it's also possible to build up a good nest egg by the time you retire. You can also take advantage of other veterans benefits. A friend of mine got more money from his GI bill benefits (tuition + stipend) than from the actual salary he made during his army years.

Quick edit: the military has a mishmash of different retirement plans depending on when you signed up. I think the most recent one is more defined contribution focused and makes it harder to get money before you're in your 60s

>If you don't blow all your expendable income on a sports car financed at 30% APR

Or knock up a stripper, or lose half your net worth when you divorce your dependa, or all the other bad life decisions that tend to plague people in that line of work.

If you can get through the first 4yr unscathed you're probably on a good path.

There's also the risk you could get sent to a war zone and get your legs or other parts blown off. Though i have the impression that's national guard work now.

This. Of course, you can mitigate the danger by choosing an appropriate job. I did four years as a Grunt and fortunately didnt sustain any injuries, but I've been in a truck and watched the guy in front of me lose three limbs. I've watched a friend who was next to me on patrol take a few rounds and die while we tried to get him out of there, and I've seen a truck roll over in a shit trench and the gunner drown in feces. Fast forward 11 years, 10 people from my company have committed suicide.

So, for anyone just chasing DoD pensions and GI bill benefits, make sure you end up as a lithographer or some shit.

My wife's grandfather did almost exactly this: navy pilot (I forget the exact details but he had at least one of those "firsts" like "landing on an aircraft carrier at night"), survived WWII, got out, was a teacher for 20+ years, and developed a keen interest in equities at exactly the right period for that.

As I understand it, the flipside of this was that not very many people in his (very early) cohort survived, in case someone is thinking of this as "easy government money".

Might not even need to do 20. There was a time around a decade ago when they allowed an early retirement after 15 years. I don't know the details, I guess the pension was less. I believe the early retirement option comes up from time to time, possibly when the military is looking to down size.

That was the force draw down after the end of the Cold War. It did not go well for the Army, at least, and they had to boost recruitment in the late 90's to keep up with normal attrition.

There's still occasional early retirement for certain MOS's I believe. Earlier this year I believe some USMC tankers got hit with a reorganization and at least some were allowed out under the early retirement authority.

Under the old system your retirement pay was 2.5% per year served. So 37.5% instead of the 50% you would get at 20 years. Last I know of early retirement happening was after the Gulf War in the mid 90s when everything was downsizing. Wouldn't be surprised if it was happening now too though.

I looked it up, it was 2012 to 2018 (unless it was cancelled before the date in the ALARACT). Not sure if it was all the military or just the Army, though. Being in the Army, I didn't concern myself with the lesser branches ;)

20 year mark is key. Sign up when you're 18, do 20 years, you're now only 38 which is < 40.

Edit: if you're super ambitious, you take the skills from your military specialization (pilot, nuke engineer, etc) to the civilian world and work another 20 years. you're now 58 which is still younger than the typical 65 for retirement, but now on 2 pensions or 1 gov't pension plus a really nice portfolio.

At the national labs, you can basically walk out with proprietary technology, as long as it’s not classified, with many modules and processes dual use, where the civilian use has yet to be exploited. I’ve seen this done many times. Proof of concept is extremely expensive for the gov’t: rack mounted heavy-duty modules, premium subsystems bought from market leaders. A good engineering team can whittle costs by 90%.

depends on if we're in an entrenched shooting war on the ground needing frontline infrantry. usually, that type of service doesn't come with a sign-up bonus

It used to. As soon as you retired you started getting paid every month for the rest of your life. At 20 years you make 50% of your base pay, so you say you join at 18, 20 years is 38. You make it to E-8 and now you retire. That's currently around $2750 a month.

If you join now there is an age it kicks in I think, rather than immediate.

Plus you still have access to things like the commissary if you live near a base. As well as medical insurance for life.

About to execute this right now and I see some interesting numbers being thrown around for the NPV of my pension.

The numbers you are seeing are really the top of the iceberg; my actual take home as a retired E7 is likely to be about twice what the pay numbers would tell you due to VA disability.

So after a take home of around $72k/year and essentially free medical for my family for life, as well as my children’s college paid for (my degree was paid while on AD so they get my GI Bill), we still need to factor in Space A flights, tax free shopping, cheaper gas, gym access, beach accesses, cheaper groceries, etc. etc.

The most recent numbers I saw were something north of 2 million for anyone E6+ who gets 100% VA disability, which is pretty common.

That said, I rarely recommend the career to people. The costs incurred really aren’t worth it unless you get the equivalent of a lottery ticket.

All of that is conditional of course; you are correct in suggesting that those benefits end at those times typically.

Some situations change that; one of my children is special needs and may never be independent so would stay in my healthcare for life. The transfer of GI Bill is relatively recent but if your father was even 0% disabled (I don’t think there’s a vet that isn’t) California would have waived your tuition to any state school after you became a resident. There are other situations that result in free college.

Having been in the military myself (albeit a short stint) it's absolutely a viable option, but just be sure you choose the right path for yourself. And be aware of the obvious downsides.

Too many people just don’t understand what car ownership costs. If we had decent public transportation a lot people currently at the margins would have their lives greatly improved. Far too many people are slaves to the debt servicing their cars and the costs of gas, insurance, and maintenance.

Cars can cost a lot but a lot of it is avoidable - especially if you are just replacing public transport. I estimate that a cheap used car has a total cost of ownership of ~$3200/year or ~$266/month.

Looking at places with public transport, a good average might be ~$130/month between the regular cost and a few special costs like going to the airport, etc.

Saving $136/month is pretty good. On the other hand, public transport costs about 50% of owning a vehicle and has a lot of limitations including only covering a single city & one person.

If not having a car means you have to buy groceries at more expensive/closer stores then the savings are not as much. If you spend more time each day on public transportation then the savings might not be worth it. If you do recreational activities that require a car then rentals/ride-shares will quickly cost more than you save.

Even in places where public transportation is used extensively it seems to be driven by factors unrelated to cost:

1. Parking is limited or very expensive

2. Traffic congestion is very high

The high cost of vehical ownership seems to be driven by consumer preferences. It's a trope that many low-income areas of the US are filled with expensive trucks. People have the option to buy luxury & new vehicles but public transport doesn't have that option.

Essentially, comparing public transport to the typical vehicle in the US isn't fair since the vehicle is more functional - wether the average American needs that extra utility is a different question.

I lived in Germany for a while and used a car twice. Both times it was a rental. Was able to take public transportation to almost every place including national parks. The U.S. needs to make investments in public transportation. It would greatly benefit the environment, our health, and our pocketbooks. In 1995 there were 0 miles of high speed rail in China and today there are tens of thousands of miles of high speed rail. We could have made similar investments into our people and the environment but haven’t.

Cars do have a utility and car sharing programs coupled with good public transportation can obviate the need for everyone to own one. Most cars spend most of their time not being used. We collectively are a nation of people who by and large spend our lives driving a car from to go from one building to another. We have people who drive somewhere for the purpose of going on a walk.

We’d be much better off without such a car centric focus.

If the U.S. could shift from a car centric culture then population density would go up. Of course having bus routes to every national park is not feasible in the U.S. but we can have a robust public transportation system beyond urban centers.

There is a cost to not having a good public transportation system. Overall, I think we and the world would be better off if the U.S. transitioned from a car centric culture.

As I see it people in the U.S. can live in spread out cities because of cars. If cars were somehow to be made undesirable then we’d want to live in more compact spaces.

Urbanization in the US has consistently increased throughout the entire time the car has been in existence.

> If cars were somehow to be made undesirable then we’d want to live in more compact spaces.

Poor people, mostly. Wealthy people could continue to live where they want. Forcibly making car ownership more undesirable seems like an extremely regressive choice.

I would rather see the trend towards mega-cities reverse. Not to rural, but to small & medium sized cities that are more livable, which are then connected by good transportation.

A livable city means a city that is not car centric. Such is my opinion. Far too much land and resources are used for parking spaces and those spaces are largely unused. Our cities are hostile to pedestrians as well as our law enforcement. Our car centric culture is regressive due to the large cost of car ownership, mandatory land usage for parking spaces and subsidies to pay for roads.

Public transportation in Prague, Czech republic, costs $15/month subsidized or $60/month if you include the taxpayer money. Also, the quality is quite good - underground, tram, bus, waiting times between 2 - 10 minutes and a dense network.

Similar for Berlin - 60 EUR/month, not sure about subsidies on top of that.

The cars in Europe cost the same or more than in US, so financially the public transport within a city is a no-brainer here. Cars are used mostly for convenience or status.

I think your costs for public transit might be a bit off. It cost me over $150/month just to commute via BART, from not too far into the East Bay, when I was doing that.

It looked like the Bay area's public transport is a bit more complicated & expensive. A NYC metro card is $127/month and from what I could fine most places in Europe were a bit below or a bit above. Currently I consider the Bay area cost to be an anomally but it could unfortuently be a indicator of much new public transport would cost in the US.

I tend to agree. A few years ago someone totaled my car, and I decided to try living without it. At the time I calculated the cost of ownership, and for a 5 or 10 year old car, it really isn't all that expensive. Part of the problem is that external costs (road, parking, etc) are amortized over everyone whether or not they own a car.

That seems high, although I don't know how you are amortizing purchasing cost.

It's worth noting that there is the middle class used car market and car repair market, and a lower class used car market and car repair market, and the lower class one is much cheaper and more grey market.

As a senior with three cars, I’ve looked at this in depth. The inconvenience isn’t worth it until I’m a hazard to myself. So I’m certain it’s unfeasible to prime young workers without a mass transit situation.

I specifically talk about people at the margins. It costs an average of $5,000 per year to own a car. There aren’t enough junk cars for everyone to own one. Roughly $0.50 per mile driven.

Bringing up owning a junk car is not relevant if there aren’t enough to make that feasible. I suspect there aren’t enough to make that a feasible options except for a small percent of the people at the margins given that junk cars are likely already prevalent for such people. I quote an average cost of ownership because I have no other stats. Junk cars do cost more to maintain and a person at the margins likely ends up paying credit card debt to service repairs.

Car ownership is expensive. It would be much better for a lot of people if we have good public transportation. It would also be healthier for the nation.

>Bringing up owning a junk car is not relevant if there aren’t enough to make that feasible.

All cars go through that phase eventually. It's a simple problem of economic friction. If more people who could afford much nicer drove those kinds of cars more of those cars would be on the market because there would be demand and people would sell stuff private party rather than taking stupidly low trade in values.

> Junk cars do cost more to maintain

More than a car under warranty, sure. If you don't maintain them to "subdivision of McMansions in a good school district" standards they are quite cheap. <Insert pearl clutching and low effort comment about road safety here.>

If you wanna drive junk you have to go all in and really play the part. Driving junk and trying to maintain it like it's not junk is a fools errand. I don't really want to go into specific examples because people will just hand wave it all away as anecdotes but basically if you buy any old running and driving shitbox for $1k, keep all the fluids topped up and changed on some semblance of a schedule and only fix the things that will imminently (like next week) keep the vehicle from operating you'll probably be out no more than the purchase price in a given year. That leaves a hell of a lot of money to buy gas before you even get close to your $5k average number.

To put real numbers to things, a 90s/00s economy car that runs some sort of 14" tire will cost you under $300 to put new tires on. A transmission replacement (which you probably wouldn't do, you'd just get another shitbox) using a medium-low mile junkyard transmission (say $250 used) will likely be under a grand after shop labor (unless you live in a HCOL urban area). A lot of crap has to break to get you to your $1k/yr cost.

Plus, if you can do the work yourself it often becomes more than worth it. A mechanic's time is expensive—yours probably is not. If you have alternative transport to get to work or fetch parts and can work on it in the evenings, stuff can be done very cheaply.

For example, paying a mechanic to repair an air conditioner (replace compressor, condenser, drier, and associated parts, with a flush out and refrigerant recharge) is prohibitively expensive. I was quoted $2000 plus labour to do this work last month by a reputable mechanic. I did it myself for about $600 with parts from rockauto.com and very basic tools (socket set).

Hyundai i10s are reasonably inexpensive and you get them new for a fair price. There are good enough options at the margin. The bigger issue is that cars not only cost the driver money but also the city. Roads are expensive and sprawl can't finance them.

It really doesn't have to be "junk" though. My last 2 cars have been 5 or 10 years old, and they both drove great, and didn't have any maintenance issues I wouldn't have expected in a new car. Both were in the 5 - 10k range, with pretty limited depreciation. The costs were gas, and a few oil changes.

You also assume that someone that's poor pays the same amount of money for a junk car than you do. Poor people pay 2-3x more than the value of a car over its lifetime, due to credit issues and predatory lending.

Why are cars terrible? Don't you think people have an innate desire to move and go places? Our ancestors moved a lot before they settled down because of farming.

Cars create suburbia which is depressing, isolating, land engourging, and plain ugly. Cars mean traffic. Traffic means going nowhere. Cars crowd out alternatives like a gene drive. Cars also contribute to obesity.

I never said transportation is bad. Take rail at all scales, and ride bikes and schooters.

Cars/bikes offer unprecedented freedom of movement. A lot of people would still own cars even if they didn't need them for driving to work. You could say the same thing about Netflix subscription, dishwasher, holidays, sports, coffee, cigarettes,..., they are all expensive and unnecessary and yet they make life nicer.

Not owning a car in a car in the US / Canada, your taxes are probably disproportionately going toward maintaining car-oriented infrastructure as opposed to public transit (depending to some extent on where exactly you live, I guess). So you're kinda screwing yourself in a sense.

Where he lives - i.e my hometown - public transport is absolutely non-existent. Twice a day you can take a bus if you need to visit neighboring towns, but that's it.

Cars are expensive. Some people enjoy buying new cars every 3-4 years, but that's also money that could be spent on retirement funds.

Didn't say that he didn't have a car - just that he didn't splurge on buying a new car every 2-4 years, like many of our peers do. I understand their rationale because they want the warranty, but still, trading in your car for something newer ever x years will cost money.

If you can "survive" driving a 10-15 year old car, and have some mechanical aptitude to do regular maintenance, then that's A LOT of money saved.

Not sure how that would work out. Contributing $30,000 per year to a fund that averages 8% per year for 20 years only gets you $1.4 million. If he lives to 80, this is only $35,000 per year, which will be next to nothing eventually due to inflation. If he left it in the market and drew 5% per year, he could get $70,000 per year, but that becomes extremely risky as you would have to draw during market downturns, which would quickly deplete the account.

The problem with early retirement is how many years you still have left. It requires far more than a normal retirement. Everyone has their own standard of what is acceptable, but IMO a comfortable retirement at 40 requires somewhere in the neighborhood of $5 million. You could do with less if you want to eat ramen noodles for the next 40 years because you can’t really afford to enjoy retirement.

Rule of thumb is withdrawing 4% per year is a safe rate that will weather market turmoil if your assets are returning market average rates. A $1.4M portfolio will allow for a safe $56,000 withdrawal per year.

The problem is that a rule of thumb is about averages, not edge cases. For a really long retirement, you are going to hit a lot of edge cases.

The 4% rule was based off the Trinity study, which looked at 30 year retirements and assumed the retiree would deplete their principal. It is not a safe basis for a long retirement.

“ Notably, it appears that the safe withdrawal rate does not decline further as the time horizon extends beyond 40-45 years (given the limited research available); the 3.5% effectively forms a safe withdrawal rate floor, at least given the (US) data we have available.”

It should be mentioned that this is not in the USA, and that even if he chose to just start burning through his investments, he will also receive a (at least minimum) pension when that time comes around, as well as not having to worry about any healthcare costs.

With that said, he's not 100% retired in the sense that he's just doing nothing - last time we spoke he was doing contracting work as an Engineer. I guess the retirement meant more "free to you want - possibly nothing if you don't feel like it"

In California a $100k salary results in the take home pay of a little more than $5k/month. So saving ~$30k/year is roughly equivalent to saving half of your take home pay of a $100k salary in California.

That's pretty good. Please keep in mind that other people do things such as support a family or go on dates. They have expenses and may live in costly cities. Even on a salary of $200k a year that's decent.

> He didn't splurge on excessive travel, electronics, cars, etc. lived a modest life.

This, I think, is the biggest hurdle for most people. Everyone wants to be a millionaire, but few are willing to sacrifice the short term pleasures and status of their consumption. See also the infamous "avocado toast" debate, which, from my personal experience with fellow millennials, had a lot of merit as a criticism.

The working/middle classes are getting screwed by housing, childcare, education, and healthcare costs that are a greater proportion of income than past generations. Avacado toast is not the problem.

In Australia, I find the Childcare is interesting. Federal government subsidises childcare significantly, like 90%.

But commercial real estate hunts out childcare providers like gold mines because you can't move your childcare to just any building. At a rough guess, $20 a day of almost every child placement is going to the landlord.

Say you want to start a childcare business. You can't just run it in any old shopfront. Some kids match their parents 40 hours a week.

So there are standards regarding kids in daycare, including the requirement for an outdoor space for play.

Now this can't be achieved in all cases but you better have a good reason. And if your competitor has an outdoor space you know where parents are likely to take their kids first.

Well, the needs are similar even if the reason is different. Parents want to know their kids will not go wandering, so yeah, it very much is a "detention" centre in the sense the kids will be detained there until pickup.

If you've ever been to a daycare centre... it pretty much is a prison. For little kids. With hopefully caring guardians and an exercise yard. :-P

And if you've ever known a 2 year old, some of them can be little sociopaths at times.

In southern California, a starter home goes for $800k or more. Which means it will be a jumbo loan, which means you will likely need the full 20% down. So around $160k plus $3,500 a month. ($1,000 of which is for property taxes and insurance).

Just for the down payment, that's 73 years worth of avacado toast at a slice a day. Millennials must be eating so much avacado toast.

And that's for a house that was built in the 80s and the boomers selling it paid $75k and whose property taxes are still capped at a max growth rate of 2% a year.

So don't live in Southern California? This is exactly the type of sacrifice people refuse to make to which I refer.

"Avocado toast" is a metaphor for conspicuous consumption at the expense of savings and investment.

Ex: $20 avocado toast at a brunch restaurant is absurdly unnecessary given the available options for sustenance.

No one actually believes avocado toast alone is what prevents younger people from getting ahead. Show me a young person making over $40k per year and I PROMISE you I can find savings opportunities in their spending habits. This, coupled with long term compounding of returns, does make a real difference over the course of a life.

Millennials are far more likely to change cities than their boomer or gen-x parents.

Avacado toast or not, I'm not sure the data is settled on whether millennials waste more money than boomers or gen-xers. They just waste it on different things.

Show me an older person making over $40k and I promise I'll find savings opportunities for them as well.

The price of a median house has gone from 3.6x the median salary to 5x. The ratios are worse in the cities that have added the most jobs. Framing this as a failure of personal behavior is missing the point. The current generation has to work harder than previous generations to achieve the same thing.

The biggest hurdle is rent followed by health care.

Most people could live like a monk and not save anything substantial.

If everyone did suddenly adopt those saving habits, it would crash consumer spending and launch the economy into a death spiral, and those exact "frugal poor" people would be the first victims.

The infamous "avocado toast" debate has absolutely no merit as a criticism.

I see a bunch of people who are so disheartened with their prospects of buying a house etc that they are YOLO/FuckItAll regarding money.

There was a HN story a few onths ago saying they are borrowing big to gamble on the stock market. And why not? They have little money. To go bankrupt is not much of a loss compared to a potential financial lotto payoff. I wouldn't try it, but I see why some think that way.

It's possible to live a very comfortable lifestyle and save a lot if you're not consumed by the idea that you need to live in SF or NY to enjoy your life. I always see these stories about how it's impossible for millenials to own a house etc. I bought my first house at 24 and sold it for 80k profit 5 years later, paid off my student loans. I'm on my second house now and it's appreciated considerably in the last few years. Both houses were below 250k with and over 1400 sqft. My wife and I have pretty modest incomes and only bring in about 100k a year together.

While there are certainly things I would like to buy that I cannot afford I can buy most of the things I enjoy when I want to without having to worry and still save a lot for retirement.

You bought your first house at the absolute bottom of the real estate market following a global crash, sold it at a profit, and bought another house during what continues to be a rapidly appreciating market.

Would a 24 year old today in the same financial position you were in at 24 be able to afford that same first house?

You applying this personal anecdote as some kind of geometric proof that living outside a major city is a pathway to simple financial independence is to me a bold-print example of how the very same people who had to fight their way up the ladder of success will promptly become oblivious to the fact that the rungs are becoming further and further apart every year, advising those behind them that "climbing it isn't that difficult, just try as hard as I did."

Okay, after reading that reply I will respectfully bow out after this reply, rather than try to force a rational conversation into an emotionally driven one.

For your information I do work very hard and afford a comfortable life, but feel great empathy for the people for whom working hard is not enough to achieve basic comforts. I did not grow up in as challenging an environment so maybe I am overinclined to that empathy, because I feel lucky my own pathway up the ladder was aided by privileges others are not afforded. But that is not relevant to the original point, it is just the reply I feel obliged to make in response to your attack on my character.

I didn't say I want anything for myself in my original reply. Broadly, I want equal opportunity for all. It was harder to get a job to repay loans in 2009 than today, but in the last 12 years college tuitions have continued to balloon while college graduate earning power continues to drop relative to the size of loans.

I do not particularly understand or appreciate your decision to season your explanation with personal attacks but that certainly accomplished nothing as far as educating me (or anyone else) about your perspective. HackerNews can be a great place to learn from a diverse set of opinions. Nobody has the opportunity to see those opinions if they are getting downvoted to grey for bad community conduct. If you are new to this community, you may find you are more successful at communicating your perspectives if you do so respectfully.

I don't want to poopoo on your point about you and your wife having "pretty modest incomes" at about 100k together.

However the median household income is only $68k a year[0]. That is 50% of households in the US earned less than 68k/year. You're actually in the top 30%[1] of US households if your income is about 100k together.

I wouldn't call that modest by any stretch of the imagination.

The median income is brought down by two factors: 1) people completely out of the workforce (the labor force non-participation rate is nearly 40%), and 2) single-earner households. Neither of these are relevant to what we'd expect to be "reasonable" or "modest" for a married, employed couple.

$100k/year for two full-time workers is $25/hour. This is a pretty reasonable wage for someone with a modicum of stability and employment consistency. For example Bank of America tellers now start at $20/hour and move to $25 in a few years.[1]

I hate to be the person to quibble about the semantics of words but when one says the word modest one doesn't usually imagine a situation that is more than 70% of all others.

I agree, it's a reasonable expectation that two people working should have a lifestyle that something like 100k/year would support.

That being reasonable doesn't change the fact that it's still more than what 70% of other situations get, regardless of how those situations came about.

If you want to compare that on an individual level then it's still not modest. The median Individual income is only 36k/year. Even on an individual level they're still doing better than 70% of the population on that level.

Yes, it's possible to be comfortable and live a nice life no in NYC or SF. But let's not delude ourselves into thinking that just because it's reasonable to expect that level of income for a household, that it's modest, or even the norm.

Imagine a world in which everyone has exactly the same income and the same expenses, saves up the same amount of money for retirement, and lives exactly the same amount of time.

In that world, someone just about to retire would in one sense be somewhere in the top 1-2% of wealth holders and in another sense be exactly average (and median, and mode), as regards their consumption patterns.

The point being, lifecycle effects matter a _lot_. In the US, ~17% of the population is 65+ (not all of them retired, of course, but many retired and living partially off their savings) and ~6% of the population are college students. Let's assume that "individual income" does not include children (though it might, depending on how it's measured. It certainly includes various people who only work part-time, but let's ignore that. If we assume that college students and retirees are all below-median (not entirely true, but no worse than the other assumptions we just made), 70th percentile of individual income is something like 60th percentile of "income of non-students and non-retirees".

> That being reasonable doesn't change the fact that it's still more than what 70% of other situations get

The point is, if you look at actual consumption (as in, how people actually live), not everyone's consumption comes entirely from income. So it's extremely misleading to look at incomes and say anything about what people "get".

It's modest for coastal people which is where most of the users on this site are from. This is pretty easy to spot when they're discussing not being able to buy homes for under $600k.

Had you not bought the first house, would you be able to afford you current house on your salary? People who bought houses in the last 10 years were lucky enough to get in when the market was historically low. People currently shopping for there first house are not so lucky.

Exactly.. I couldn't afford to buy before but for a brief window my salary allowed me to buy a home in the area of my city most people were choosing to avoid. I wouldn't qualify the following year and I would be very far off now as my salary did not rise at the same level.

What I see smart young people doing is moving away from bigger cities. They get a decent house / lot compared to a condo in a bigger area.

Every generation has to move further away (or make more than others) if a city is growing. You don't have to live in a growing city.. you could move to a declining area or a neutral area. There are advantages to living in a declining city.

> Every generation has to move further away (or make more than others) if a city is growing

I mean... maybe to some extent, but ultimately not really. Growing cities becoming unaffordable is a result of our choices. We can make different choices.

I don't know why but people love the idea of scarcity and exclusivity. If we had a star trek like post scarcity society in 2031 and transported people from 2021 to it they would try and figure out how to reintroduce scarcity back into the system.

that's kind of a weird strawman. I don't think people (in general) love scarcity, but you don't have to think too hard to realize that some desirable things are inherently scarce. even in star trek, there are only so many penthouses with a view of central park.

The market is always "low" in the areas I've lived in. That's my point. My brother also just but a very nice house for 180k. There are plenty of affordable places in this country.

>People who bought houses in the last 10 years were lucky enough to get in when the market was historically low.

You realize those same people also had to deal with a shitty job market and college loans to pay off as soon as they graduated right?

> You realize those same people also had to deal with a shitty job market and college loans to pay off as soon as they graduated right?

I think this is a good point that's worth repeating in these conversations. It's easy to forget in better times, but economic crashes are really scary. The financial crisis scared the shit out of me; my job situation was tenuous and our finances were shaky, but my wife and I took a big gamble and bought a foreclosed house at what turned out to be the bottom of market.

It seems like an obvious choice in hindsight, but it could easily have gone very badly.

Growing up in the midwest prior to working FAANG in the Bay Area, this is my exact experience. With a graduate degree and making ridiculous money, I and my peers had no realistic path to homeownership on any reasonable time-scale in the Bay. Family members working HVAC, plumbing, electrician or other skilled blue-collar jobs in low-cost of living areas bought beautiful craftsman bungalows within walking distance to a decent school for $80K. Professionals with either no student debt or a few thousand from land-grant state university degree paid off in 5-7 years. This has knock-on effects to family formation and number of children. Many of my high school classmates had their first kid at 24-25 and have 3-5 kids now, versus Bay Area average of what seems like 1-2 starting in your late 30s. When you feel like you can finally afford it. I started making plans to leave as soon as I got there, it truly was "structurally hostile to families."

You make a very good point. People dramatically underestimate how much more you need to make in the Bay Area to have the same quality of life as living in low cost of living areas.

Not that this is entirely wrong in principle, but it sounds like you got into the market for a house right around 2009. "Happen to enter the market at the exact bottom of a historic crash" isn't exactly a strategy. It's just luck.

I think it will be fascinating to watch the FIRE movement and the broader trading communities through the next crash. It is easy to feel like a genius when the market is going up 30% in a year.

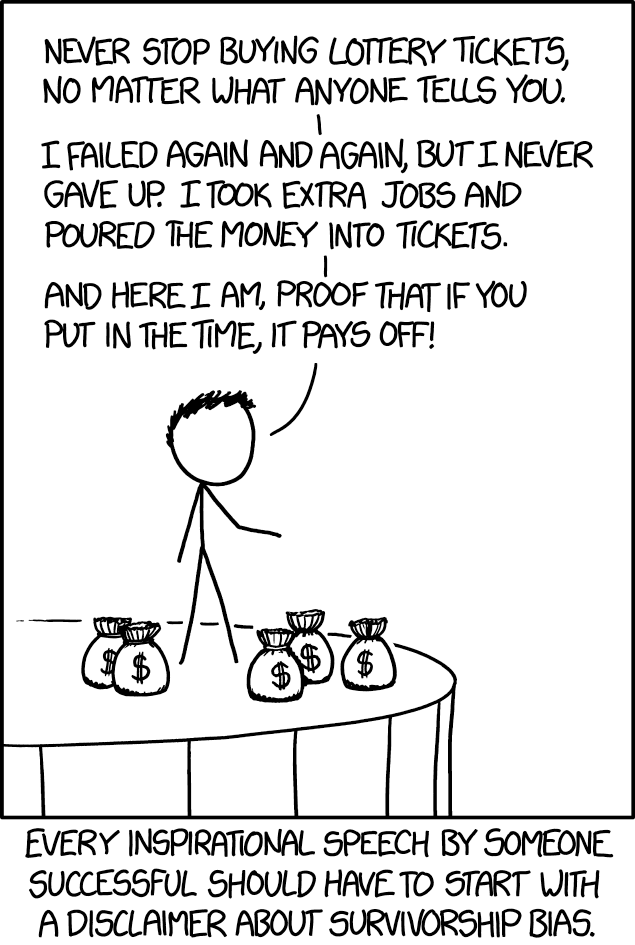

Well sure, but perhaps also it's just survivorship bias. It sure seems like there is always somebody that just got lucky, no matter what is going on. 10 years from now, there will be a group of people that "just got lucky" with something they did right now.

I guess what I'm saying is that the right attitude is to decide that no matter how terrible everything is and no matter how stacked against you the world is, there is an opportunity - somewhere, somehow.

Oh you mean the same time I graduated into a shitty job market with thousands in college loans?

No, I made smart decisions about purchasing a house in a good low col area and fixed it up.

Honestly, this whole idea that anyone who's achieved some success is just down to luck is pretty disheartening. Do you think this is a good approach to improving your life? I don't see any advantage to thinking this way.

I think it's a perfectly fine approach to life to acknowledge the role played by luck. I don't pretend I'm completely in control and all my success is solely due to my superior grit and intellect (and, of course, even having those traits at all is still just luck). Nonetheless, I've done perfectly fine. My life has improved fairly consistently for about 20 years to the point it is better than I ever reasonably expected it would ever be.

So no, I don't think you need to buy into myths to improve your life. By all means, make the smartest moves you can with the hand you're dealt, but you have absolutely no control over what hand you're dealt. If you got lucky, good for you. Plenty of others got lucky and squandered it. I'm not saying don't feel proud of yourself. But don't forget the many people who never even got the chance. You're not better than them and neither am I.

> superior grit and intellect (and, of course, even having those traits at all is still just luck).

I don't think this is true. Sure, it's trivially true that we don't earn the traits we're born with in any way. But it should be equally obvious that people can and do cultivate these same traits deliberately throughout life. People cultivate grit (i.e., discipline, persistence, courage, etc), and everyone has to fulfill whatever innate intellect they were given with knowledge and experience, which don't come for free.

There's certainly a lot of luck involved all along the way, but labelling it all "just luck" is a pretty broad stroke is it not?

> You're not better than them and neither am I.

"Better" is a heavily loaded term. I suspect you're angling for a "worthy of life, liberty, and the pursuit of happiness" sort of meaning, which is dangerously close to a strawman. But if "better" is given a more specific and practical "better steward of their resources" meaning, then I assure you there are lots people better than me.

Oh boy this so much! I'm fully aware of how lucky I've been. Grit and intellect are pretty much down to luck in choosing your parents.

It's so easy and so natural to look down on other people. Everybody does it, and the best we can do is try to fight against it by having some humility.

I think you might be catching too much flak on this thread but to add to the discussion:

>Oh you mean the same time I graduated into a shitty job market with thousands in college loans?

I think this is actually to the same point. Compare what you stated with someone who, say, graduated in the 1960s where they could have a middle class lifestyle without even graduating college, or if they did graduate, without mountains of debt or relatively high home prices.

Both points can be true. There can still be paths forward while also acknowledging it can be more difficult. Exceptional people will always find a path to success; that's what makes them exceptional. What worries me is when we (as a society) make it exceedingly difficult for large swaths of people to succeed at achieving something as modest as "middle-class".

Also a millennial. Also bought my first house at 24. Sold it 6 years later for a loss of $90k. Timing is important. Not everyone was fortunate to buy at the beginning of a huge bull market and right after a historic crash in real estate prices. (Bought my house in 2006)

> if you're not consumed by the idea that you need to live in SF or NY to enjoy your life

And yet some people enjoy big cities more than they'd enjoy living in a small town and it is not a moral failing or a sign of stupidity or weakness.

Many people enjoy the multiculturalism found in cities, and many immigrants or minorities feel out of place in small towns while major cities offer them the opportunity to connect with people like themselves.

Obviously owning a big residence in a city will never be affordable but as a society we should ensure that people can affordably live where it makes sense for them.

Why bring multiculturalism into it, or minorities feeling out of place? the parent comment never mentioned it, and I have been to small towns that were extremely welcoming to all groups. I agree with his statement, why live somewhere where housing is astronomically expensive, unless you enjoy it so much that living somewhere else would bring you sheer misery, be prepared to either rent forever or hustle your life away to afford that lifestyle.

Because that is one thing i know that people mention a lot in moving to cities. Maybe part of it is american perspective. Is there something WRONG with talking about multiculturalism?

eg. gay people leaving their small towns that don't have other gays, immigrants moving to a city full of people of their nationality (eg. "china towns, little italy").

No amount of "is renting forever not bad?" will rectify this advantage of a city for many people.

Having a preference for multiculturalism is something mostly expressed in the west. People in Nigeria, Iran, Iraq, Peru, India, etc. Live just fine with it without it. They don’t feel inadequate living in a city or village that is monocultural.

Neither is right or wrong. Cities develop over decades and they will have their unique histories. But seldom do people in other places say, oh my town is so monocultural, I wish it were a stew of cultures. No, mostly they are okay with their towns character. Interestingly besides Singapore, we have Beirut, Teheran, Khartoum, Baghdad which have lost multiculturalism over time, but those are mostly due to civil strife caused in part by the different cultures at violent odds with each other.

Cities have always collected people from further outside the local area than suburban or rural areas. If you have lived in cities with a monoculture and cities with significant minorities, the multicultural city has more dynamic options for food, drink, music, everything. New York is one of the only places in the world you could probably walk from fantastic bagels to great Italian food to a real HK-style diner. This is a great privilege that residents of these cities value highly.

Really, I would suggest you read up about Peru. They're one of the more multicultural countries in the Americas, they've got multiculturalism enshrined in their constitution.

They have indigenous, mixed race, Japanese and others, that’s not in dispute. What I’m saying is I’m sure in the hinterlands the locals aren’t saying “oh, woe is us, we aren’t multicultural like those folks in Lima”

Multiculturalism can be good, it can be neutral or like Beirut or Baghdad it can lead to violence. What I’m saying is most people overseas are totally okay with it, with few exceptions, but they don’t bemoan it’s absence.

honestly if they enjoy it that's their call and they make the choice to live in a place that is not affordable. If they struggle due to that decision that is on them. If they could move somewhere else and live in a much more comfortable financial position the long term outcome is their choice. I am not denigrating their decision just saying that it is their decision.

"we should ensure that people can affordably live where it makes sense for them" It makes sense for people to live in an area they can afford, not where they decide they should be able to afford. Its simple economics, supply and demand.

"Many people enjoy the multiculturalism found in cities, and many immigrants or minorities feel out of place in small towns while major cities offer them the opportunity to connect with people like themselves". Not to be rude, but so what? I want to live in Napa Valley but I cant afford it, is it society's job to get me an affordable house there?

The calculus is a bit more complicated than you make it out to be. People have to live where they can afford to live -and- get a job. Many lcol areas do not have many jobs. Especially if you have an expensive education that you are trying to pay off.

Some people might be able to take a pay cut and move somewhere cheap and come out ahead. But those options don't always exist. If you have $200k in student loans and a degree in biotechnology, good luck finding a job within 100 miles of cheap housing. More remote work opportunities might change this, but at least in the past, those were very rare. Housing is expensive in hcol areas for a reason. It's because there are lots of good paying jobs nearby. There is also a reason some areas have very cheap housing.

You make good points but the comment I was responding to was very focused on people choosing to live somewhere based on what they like regarding the social atmosphere and feelings as opposed to economic concerns.

Living in a big city isn't much of a problem, only real difference is that almost all your equity will be in your house / real-estate assets. And that can be just fine - in certain areas the real-estate market has performed as well as the stock market, for the past 20-30 years.

But it's difficult to retire on that - unless you decide to sell your house, and move somewhere cheap.

Heh, I don't understand why you are getting downvoted (well I do, but it's not a charitable interpretation). Yep, totally agree - people are not entitled to buy a house wherever they want. At least before the money printer went brrrrr, housing prices as compared to income in the US (median) were one of the lowest among the developed countries. Even now, median house is $375k [1]. Get out of your bubble.

And I say it from the position of someone who actually made this mistake - I bought in Seattle and regret it. A much better decision would have been to buy a cheaper, better house somewhere else. Still, I'm not going to be mad at people telling me this truth :)

Lol, now I'm getting silently downvoted. Come on, tell me which specific statement from my post (or the GP post) is false, or non-factual and doesn't contribute to the discussion :D

The book's claim is something like "most millionaires are people who own ordinary small businesses without a luxurious lifestyle".

This article seems to be trying to refute the different claim that "even a low-income person can easily become a millionaire". But I don't think that's ever been true, and it's not really the book's message. Someone making $130,000 as a small business owner isn't "low-income" - the book is mainly contrasting this group with highly educated doctors, lawyers, MBAs, etc, who also have high incomes but spend much more.

And in the context of becoming a millionaire through investments, adjusting by more relevant factors than consumer goods inflation result in the following:

* Residential real estate inflation: $355k [1]

* Stock market inflation: $770k [2]

* Dollar supply inflation: $712k [3]

You'd have to earn between $350k and $700k/year for your dollars to have the same asset buying power as $130k/year in 1996.

> You'd have to earn between $350k and $700k/year for your dollars to have the same asset buying power as $130k/year in 1996.

This is absurd. There has certainly been inflation, but the value of the stock market (and dollar supply) are not directly relevant to a person's buying power.

The residential real estate price rise is a real factor, but even that is offset by the fact that most people buy homes with mortgages and mortgage rates are so much lower today (7.8% in 1996 vs ~3% now). I can't find the numbers now, but as I understand it the median home is more affordable now for the median income than it was in 1996 (again mostly due to cheap mortgages).

To come at this from another angle: in 1996, $130k was not in the top quintile of earners. Today, the top quintile starts at ~$250k[1]. People earning $350k-$700k are well into the top quintile of earners and likely into the top 10% or beyond; they are much richer than someone earning $130k in 1996.

Summary: $130k is still a relatively solid income (top 25% of earners), but $350k-$700k today is not the equivalent of $130k in 1996.

But in this case they are simply stating the truth, so I don’t think they need to say much. Rising prices for an asset cannot be called inflation, since the owner of the asset benefits from the rising prices. Inflation is specifically the opposite: the loss of value. Words need to have some meaning or we will have no way to communicate with one another.

Why would you switch perspective when describing assets vs consumer goods price rises?

When considering the price of assets, a generalized rise in prices has the same relative effect as inflation in consumer goods; the decline in the purchasing power of money relative to other assets.

The fact that some people benefit from assets inflation because they owned outsized amounts of assets compared to the rest of the population, is orthogonal to that base mechanism. Someone with a huge stock of oil would also benefit from an increase in oil prices following consumer goods inflation.

Beware using convoluted gymnastics to hide simple truths. "Inflation" is first and foremost an English word. Human languages are abstract and powerful, there's more value in generalizing words to understand other realities, than restricting their use to a single "dictionary of economics" definition pointing to a single metric with predefined inputs.

That is incoherent. What are you talking about? This is completely untrue and doesn't even make sense:

"When considering the price of assets, a generalized rise in prices has the same relative effect as inflation in consumer goods; the decline in the purchasing power of money relative to other assets."

Someone owned the asset before you bought it and that person became wealthier as the asset prices rose.

If I buy a house for $250,000 and suddenly it is $500,000 then I am suddenly $250,000 wealthier. If I buy 2 liters of milk for $6 and a week later I want to buy more but now it is $12 then I am poorer because the things I consume cost more.

Economists use the term "inflation" to refer to the loss of value that some consumables suffer as the money supply grows. But the concept doesn't apply to assets because the owner of an asset can sell the asset and reap the rewards. By contrast, if I buy some milk, and keep it in my refrigerator for 20 years, I can't then sell it and benefit from inflation.

When we talk about economics, inflation refers to a loss of value. Rising asset prices refer to a gain in value.

Under your crazy definition, where inflation applies to assets, there has been no gain in wealth since the beginning of time, since the rising prices of all assets are thought of as a loss instead of a gain, under your definition.

About this:

"than restricting their use to a single "dictionary of economics" definition pointing to a single metric with predefined inputs"

Every profession uses certain words in specialized ways. If you don't like the way some topics are discussed in a given branch of knowledge, then just don't participate in those conversations. I will assume, since you are on Hacker News, that you don't have a problem when engineers give special meaning to "message" or "bus" or "event" or "queue" or "broker".