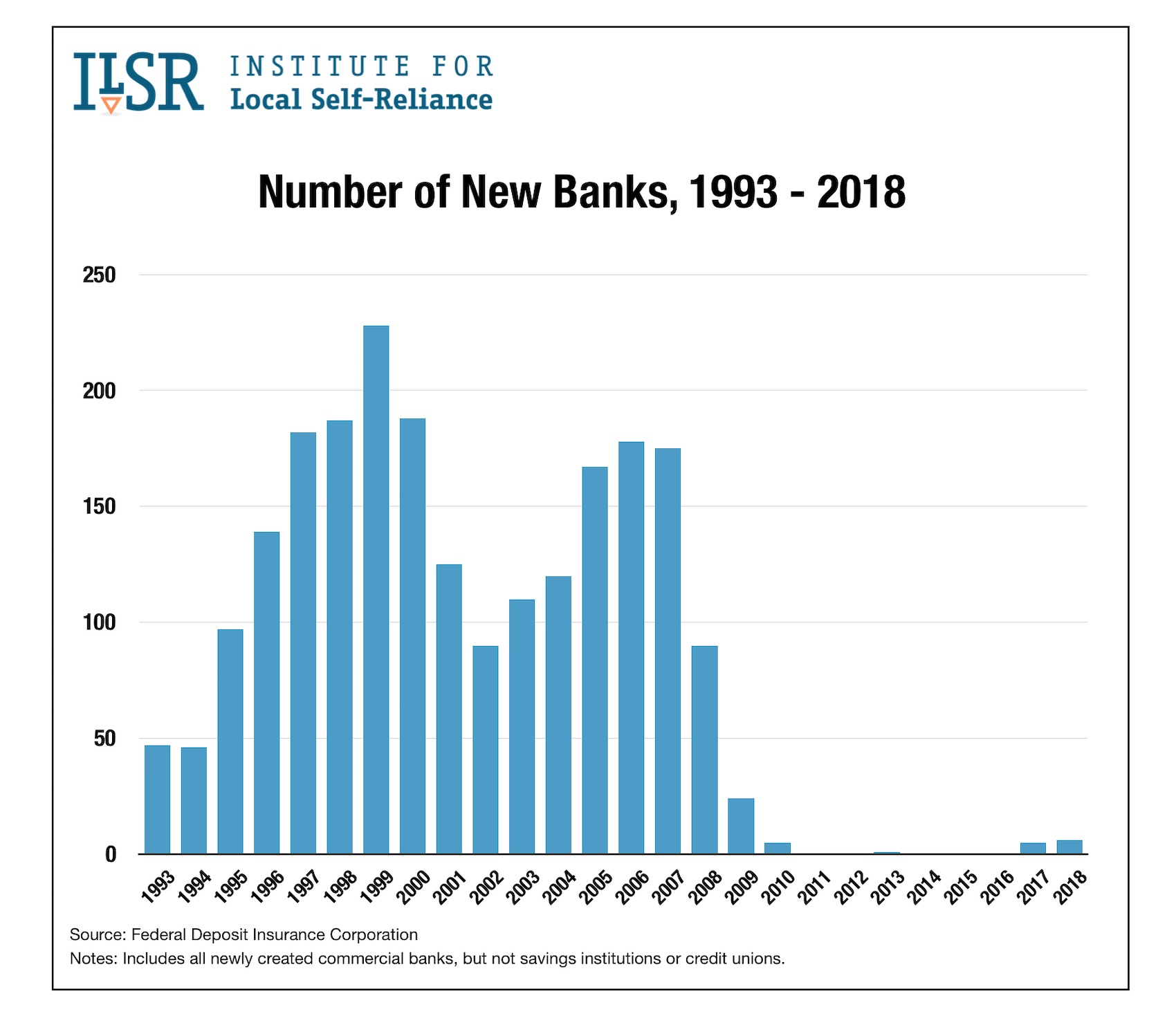

I know someone who was seriously trying to start a bank. After all his research he concluded that starting a bank from scratch was cost prohibitive. However buying an existing bank was way easier.

For the US the amount of regulation that banks have to comply with is enormous. I'm not entirely sure all of it is value add. In contrast bitcoin has almost no regulations or controls around it. Is there not anything in between?

As they say, most safety regulations are written blood and banking regulations are written in lost gold.

Pretty much every regulation is there because at some point someone figured out how to steal money from someone else, and the regulation prevents that. I don't really think there can be an in between.

You either have a totally unregulated market like Bitcoin, where it's incredibly easy to steal from people with absolutely no recourse (not even the courts), or you have what we have now where your money is "safe" and if something happens anyway you can be made whole through the courts, which would then lead to new regulations to prevent that thing from happening again.

I understand the concept, but that doesn't justify the level of government interference we have in the banking industry.

I'm in IT security for a financial institution, and we have regulators checking the permissions of our NTP configs and that IPV6 is disabled on our cloud instances.

Those are two trivial examples out of 10,000 I could give on how there is a cottage industry of regulators and consultants and auditors making things over complex, milking money from banks, and generally making it harder to do your job because one time, this one place had this one issue.

Frankly, I'd like to get out of the banking industry because of how stupid all this shit is - most auditors don't even know what they're talking about. It'd be like hiring some HN commenters to review the schematics of the 737 for safety.

If your firewall isn’t configured correctly then it’s really easy to directly access a host from the internet. It’s easier for the regulator to just make sure ipv6 is off (and all of the ipv4 are private addresses) instead of verifying the firewall config.

Maybe "incredibly easy" isn't the right term for _stealing_ it - but once it's stolen it's easy to get away with it. This is especially true if you're managing your own wallet/private keys/etc.

If you're not careful with your machine, all it takes is some piece of malware lurking in the background to keylog your password, decrypt your wallet's private key, get the funds transferred from your wallet to the hacker's, and poof all your crypto is gone. That's game over. It's gone. No court or government can get it back for you unless they send a SWAT team to go steal the private key from the people who stole it from you.

If you're relying on Coinbase or another exchange to host your wallet for you, that's a different story, but at that point they're fulfilling a similar role that a bank does for you.. which to some is entirely what they're trying to get away from by using Bitcoin and such.

The amount thieves have gotten away with (several $100m+ crypto heists) is comparable to the total amount that has been legitimately spent using crypto for actual goods and services (not counting “investing”) in the entire crypto economy.

Remember that stealing isn’t just one person taking it from another. It’s also institutional theft. See Mt. Gox as a prime example. Lots of people lost a lot of bitcoins.

If that were a regulated bank, the government would make them whole.

I didn't get that, but it's a legitimate problem. There's a chance that at some point some organization (say the Chinese government) will have enough resources to takeover the blockchain, at which point you're at the mercy of them, with no recourse.

Why do you need a banking license? There are lots of challenger banks that have no banking licenses. In between is a money transfer license and just dealing with anti money laundering and know your customer regulations. I don’t even think PayPal or square have a banking license. Neither does apple with their apple wallet cash functionality.

Banks make loans. Banks are expected to have sufficent cash reserves to service all of their customer accounts. If a bank fails, account holders dont get their money back aside from whats insured by the FDIC and only up to 250k$.

Bitcoins are literally just pieces of a digital ledger system. No loans and all units of account are depedant exclusively on the ledger.

Regulating a bank is required because banks take in capital from account owners and take on additional risk by loaning that capital to others which may or may not get paid back. If banks lose money from bad loans to a point they dont have the cash available to service customer accounts the only thing they can tell people trying to make a withdrawel is 'tough titty'.

You don't have that problem with bitcoin. You get many other problems with it, volatile pricing and a complete inability to control money supply, but that's not one of them.

I looked into this as well. The most amusing aspect in NYS is that to get a banking license at least one of your board members has to be a good ol’ boy.

That still doesn't mean that starting a bank in the US is harder (or at least as hard) than it is elsewhere, right? Or maybe that person owned banks all around the world?

From reading a little online, it sounds way easier to start a bank in the US than it is in Israel.

I was employee #3 at a startup funded in part by a guy who started a small local bank. I talked to him about his real estate investments and the bank. Upon my inquiry of how one actually starts a bank he replied, “owning property is a right, owning a bank is a privilege”. Meaning, merely being wealthy enough to start a bank does not mean one can do so. I wonder how many children he had to sacrifice to moloch to get into the club.

This article doesn't tell me what I really want to know, which is why a country with enormous FDI and GDP like Israel has gone almost 5 decades with no new banks. Is there a regulatory hurdle? Cultural taboos?

Branchless banking seems like a capability enabled only in the last 15 years by widespread internet adoption among customers as well as a transition to a cashless economy in the last 5 years.

Before then I'd imagine the physical startup costs and physical network effects of having hundreds of branches/ATMs, combined with low retail margins would've made it prohibitive for new competition.

I don’t think corruption has anything to do with it (unless you can give any concrete example).

Israel didn’t have new banks because the regulator preferred to protect the stability of the existing players, which are heavily regulated themselves. Israel had its share of troubles caused by banks in the 1980s and 1990s, and today banks are kept away from many asset classes and operations to ensure their stability and limit their clout.

You could say that the banking regulators gave a limited amount of players a license to print money but they had to play by very particular rules on who owns them, what they do and how their balance sheet looks.

> Israel didn’t have new banks because the regulator preferred to protect the stability of the existing players

Well said. Whatever the justification, protecting the profits of incumbents at the expense of new entrants is regulatory capture.

And to your latter point, here is an example: in the US telecom providers are highly regulated, but they also have largely captured the FCC.

Onerous amounts of regulation, contrary to perception, are good for incumbents. It makes launching a new business hard.

Fighting through regulatory barriers is one challenge for some European startups trying to achieve scale and displace or match an incumbent. (Very low turnover in top 500 EU companies vs US too 500)

Lastly I’d like to note that Israel has some room to improve on the corruption front - they are ranked as having higher perceived corruption than Spain and South Korea, two countries where the rich stay rich, and on par with Botswana. [0] And a bit below the US, where we already struggle with corruption and regulatory capture.

The list you cite is “corruption perception”, not corruption per se. other lists such as GCI rank Israel (20th) roughly on par with Japan (18th) [0]

The banking regulators in Israel are quite upfront about their objectives of maintaining banking sector stability even at the cost of competition or cost to consumers. They even oversee banking boards.

Israel does rank very favorably on this list - I wonder why the perception of corruption, among businesses, is so much higher the measure posited by risk-indexes.com?

Perhaps one reason is that the perceived corruption ranking that I shared is just that, while your measure dilutes "Corruption Perception," and "Corruption Experience," to just 42.5% of the measure, filling in the majority of the corruption measure with:

- Ratification status of Conventions

- Citizen's Voice and Transparency

- Government Functioning and Effectiveness

- Legal Context

- Political Context

- White collar Crimes

Which to me, in the context of evaluating "Why have there been no new banks in Israel since 1978?" are not as useful as just the combined experiences of companies who are financially exposed to Israeli government decision making.

One difference is that corruption in China is often local (federalized corruption?): if you can't get something done in Guangzhou maybe you move it to Changchun and you can. That option doesn't exist in Israel.

>Israel does rank very favorably on this list - I wonder why the perception of corruption, among businesses, is so much higher the measure posited by risk-indexes.com?

A few factors:

- In Israel corruption is very aggressively prosecuted and will be featured on national news (the only kind of news. no local news there) repeatedly. It creates impression that corruption is everywhere

- Orthodox sector due to it's influence gets non-proportional amounts of money from budgets

Some very interesting anecdote points - I'll say my personal references are an old boss, who is close to Israeli politics in the US, and Israeli emmigrants. (Main complaint was they liked forests and green more than the desert.)

I appreciate your context; and I did request the dataset from the risk-index organization, and will update here if I receive it.

Banks are so tightly regulated that they all offer pretty much identical options at identical prices. Shopping around, it's virtually impossible to find any differentiator between them. They don't even advertise based on differentiation, it's more things like 'our call center people are more polite than theirs'.

Absolutely the opposite. Fintech and online-only banks have allowed so much new things to differentiate to the old banks. The concept of privacy.com with securing your online credit card purchase, revolut‘s ability to get rid of money exchange fees or just the many app banks.

Not that the current state of affairs is any different. I long for a transparent algorithm (in the sense of "clear set of rules") that determine whether you can get credit or not.

I was a customer of Simple's for several years and while it didn't pan out and they weren't really a "bank" but lipstick over one, I LOVED the modern touch on what is normally a cumbersome and painful experience.

Kudos to any company that is trying to update the banking system. It could really use it.

I’m not sure it will last, Israel has an extremely tightly regulated banking sector, and major banks already offer a competitive digital platform.

Unlike the EU where digital banks can start in a small market and then expand by using their passporting rights a bank in Israel is constrained to a rather small market.

> major banks already offer a competitive digital platform.

Did this improve a lot recently? Only 2 years ago, the Wall Street Journal described the inconvenience of Israeli banking this way:

> Banking occupies a special place among the complaints of Israelis. Banks refuse to give out the phone number of a designated representative. Most basic functions can be dealt with only in person at the branch where an account was opened.

> Tech workers - many of them American and European immigrants who came of age with mobile banking - can toil all day on some of the world's most advanced projects, only to find they can't email their bank any documents. Many Israeli banks demand documents in person, sent by mail or by fax.

> when [Aliza Landes, a] 35-year-old American-Israeli [,] recently tried to send money electronically to pay for her wedding dress, the experience was less than high tech. It took two hours on the phone, and then a trip to her bank branch, where employees manually added the send-money function to her app.

I’m an American that had to work in Israel for a couple of years. Israeli banking is weird. For example I was often asked by my banker (Hapoalim) to hand write instructions/permission to do something on a piece of paper, take a picture of it with my phone, and text it to him. It’s hard to imagine a salty Chase Bank rep back home asking for this. Israel is this strange combination of first world and third world improvisational organized chaos mentality.

I wanted to close an account from a credit union in the States, mid-pandemic. I called, they said to email a support person. The support person told me to write a letter, photograph it with my identity card in the picture, and send it over. It felt strangely surreal.

Can do almost anything on the web. Can even cash in checks by taking a picture of them on the app. Calling the central number for the bank directs the call automatically to my personal banker based on my caller ID. I haven't been to the branch in years.

Although it is true that when you _do_ need to go in, you need to go to your own branch, which is something that surprised me coming from the UK.

This is probably because accounts are branch specific and all your paperwork is there. If you want to move branch, your account number will change.

Maybe one day they will "fix" it .

been with bank hapoalim, which is one of the larger banks. maybe this article relates to one of the worst banks.

- i have a designated representative for 20 years or so (usually it happens when you have income above average I guess)

- most of functions I could do via web site for many-many years. probably also via mobile app.

- been emailing documents to my bank for 5 years at least

- can make either local same day transfers or international transfers online, forever.

with regards to "trip to branch where employees added send-money function to app", you need to sign agreement for performing operations online and stuff (probably part of regulations). till you do it, web banking is a bit limited. those days you can agree to it online i think

This has not been my experience. It's quite easy to send money to any bank account even in another Bank. The online portal at my bank is pretty easy to use

The most popular money transfer app (think Zelle), with about 80% or so of the market last I checked, iscalled Bit and operated by the largest bank (Hapoalim). It will not let you receive money or send it, unless you give it full access to your contacts -- even though it allows sending and receiving from non-contacts.

Doesn't feel like there's any real competition there - the other competitors (Pepper and Paybox) don't seem to leave a mark. Hapoalim is definitely leveraging their might for digital dominance.

I’ve got a true admiration for this mobile eye cto, after seing a presentation he gave 4 years ago (can be found online), where he explained the current theoretical limitation of ML for autonomous driving, at the time where tesla was saying it was just around the corner.

It takes some guts to publicly state « we have no clue how to do that thing our ex-customer now competitor claims is able to do , and we think nobody knows how to do it safely, and here’s why ».

It’s even more exceptional when you compare it to the gigantic amount of crap that many israelis startup advertize , surfing on the reputation of the country for being a startup nation (i can’t count the number of cancer cure that i’ve seen israelis biotech companies claim)

{kind=link}

For the US the amount of regulation that banks have to comply with is enormous. I'm not entirely sure all of it is value add. In contrast bitcoin has almost no regulations or controls around it. Is there not anything in between?