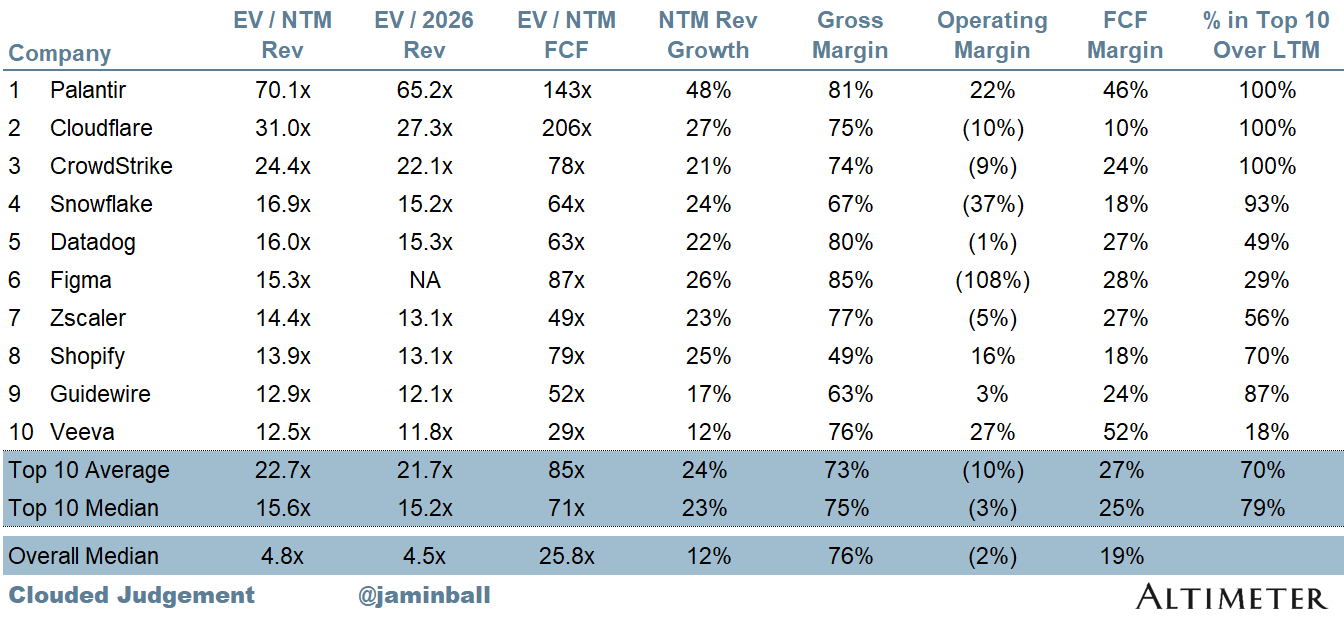

Cloudflare is one of those companies similar to palantir where the valuation just makes you scratch your head. But bringing in AI to try and fill out the AI valuation makes some sense I suppose

I wrote this comment [0] very recently and when I wrote it had in mind that Cloudflare might very well end up being a key player in a more centralized Internet that has developed far away from its original architecture.

Defense against threats is a pretty strong centralization incentive in different kinds of networks - social, biological.

I could imagine that a lot of people are investing based on similar scenarios in their minds.

Joining the big three requires capital investments orders of magnitude beyond where they are. Nevertheless I'd like to see someone do it, and if not Equinix then it could be them. But sadly the #4 right now appears to be Oracle.

I havent looked into the financials but the reasons I really like cloudflare is that its workers are free without card for 100k and even after that its ridiculously cheap and cloudflare tunnels and a lot of features are free and really appreciate it

I feel like people like to rub that one time cloudflare messed up when I mention it but it was a gambling website and I feel like cloudflare could've better communicated it but overall its got so much less drama than the other cloud providers and its genuinely being really nice imo

But imo, cloudflare is really dirt cheap for just starting out and at scale as well especially if using cf workers

I feel like cloudflare can make a bank in enterprice section but their pricing model also feels the most saner compared to the shady tactics used by google or others with our marketing and privacy

I know that the internet is getting centralized but I feel like there are some ways of de-centralizing it, (by example archiving web pages and then seeding them, helping on internet archive or something similar as well)

As an internet user, cf feels mid but sometimes as a guy who just wants to deploy shit or basic apis, I "vibe coded" a cloudflare worker api which I actively use so much for my own purposes setting up a custom redirector and everything without paying anything at all, I think I like it.

Honestly, nothing is as good or as bad as it seems except palantir's evaluation which makes me feel like 448 pe ratio or something similar drove me nuts the other day.

Edit: Although I still stand with what I say, this comment has also aged like fine milk with cloudflare taking down aws,chatgpt and x and sooo many others that cloudflare outage had more upvotes on HN (if I am correct, I can be wrong tho, nothing new about it as well ) and thus more impact...

Honestly now the only stable provider which doesn't have an outage is google cloud in sick twisted fate

I am wishing when google cloud has its outage so I can recommend everybody to use hetzner (yes I know its not an apples to orange comparisons but hetzner has some crazy good uptime)

Cloudflare isn't solely a CDN anymore. CDN and DDOS-protection were the most logical "first" products to build based on their SDN ( Software Defined Networking).

A cloud is the next thing and there's a lot of money involved with the cloud. I see them as the only real competitor/challenger to Azure, AWS, GCE, ... because they aren't bound to regions ( less DevOps)

I'm not saying they're not an interesting company I'm just reflecting on their extraordinary valuation multiple which puts them in a unique league that are predominantly AI bets. Their founder is uniquely strong storyteller. If you look at their capital investment it's just not anywhere close to a top tier cloud player.. so while they offer some interesting building blocks it's just not clear that large workloads move there anytime soon

It's not a question of crazy or not, it's just an extreme end of the multiple spectrum.. and the company is not in a positive operating margin position. So you're right they have a strong track record and there's optimism they turn a profit, but it's highly speculative. Nothing wrong with that. Just makes sense they are fleshing out their AI story while they're in a position to invest with equity IMO

Well I'd assume the acquisition is with equity and that much of their employee compensation comes from equity, neither of which show up in a free cash flow view. Still you do make a good point. I'd have expected bigger capital costs that even if amortized would show up on cash flow some of the time.. but they appear to run a very tight capex ship. So more security SaaS than cloud provider IMO

{kind=link}