I'm skeptical of that argument. Historically when technology has advanced, it has created new roles for people whose jobs were obsoleted. Why is now the time when the majority of the population becomes too dumb to cut it in the "new economy?" Especially when technology acts as a multiplying effect for what someone without specialized education can do? Generally, depressed wages (i.e.: decreased price of labor) should drive up demand. If that doesn't happen, that means there is a bottleneck somewhere else.

I think a key observation missing in all of these analyses is the most obvious one: that bottleneck is energy. What's different between 1995 and today? Well a barrel of oil cost about $25 2010 dollars back then, and costs almost $100 dollars now. We have an economy that is entirely driven by oil. When the cost of that goes up, because we've run out of the easy-to-reach stuff and have moved to expensive and difficult methods, then it's no surprise that the economic equilibrium shifts to a point with lower activity.

It may be because a lot of 'the rich' don't really need anything other than what they already have. There's not much to buy that's important to a lot of people with the money to buy it. Frankly, there really aren't that many truly useful or interesting products or services.

It was illustrative to me while reading the other HN articles on wealth. Some of those who have already sold their companies for millions haven't changed their life style much. They still buy the same things, still live pretty much the same way. Maybe travel more. Otherwise, the extra capital just goes into more investments that help to further inflate the established capital markets.

Wha? The price of oil is going up because there are billions of new consumers of petroleum on the world stage. Speculation has caused prices to spike in recent years, but you'd be crazy to think that we'll ever see $1 gas again.

Oil production is relatively inelastic in the short term, in the sense that it takes years to scout new fields and make the necessary investments in infrastructure. But then, so is demand, and future demand is relatively predictable. Even hypothesizing that oil companies didn't predict ten years ago that demand for petroleum would be at its present level today, and didn't plan for enough capacity, we would expect that by now they've realized their mistake, and that prices should go back down as additional capacity comes online.

It doesn't matter what they predicted; global oil production likely peaked in the last few years and no amount of wishful thinking is going to make more of it suddenly appear. Almost nobody in the industry seriously believes that production will increase in the medium to long-term; a lot of people don't even believe a short-term increase is possible. Falling production, rising demand and the lack of effective substitutes are all driving up prices. Over the next 10-20 years there is just no foreseeable means of reversing _any_ of these trends.

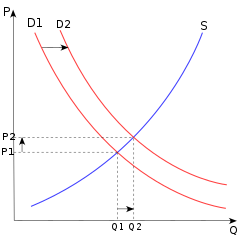

When costs go up, producers become less willing to supply product at a given price. This shifts the supply curve left, and establishes a new equilibrium at a lower quantity but higher price. Of course, with regards to oil, demand has been exploding in developing nations, which has pushed the demand curve to the right. Now, picture pulling the supply and demand curves to the left and right, respectively, at the same time to see how that causes the equilibrium price to spike.

As for speculation, it's hard to tell what speculation is really doing here. Speculation is, to an extent, the mechanism through which the market incorporates knowledge about the future scarcity of a good into the price of the good. Whether or not we've hit "peak oil" we're clearly in a situation where oil extraction is getting more complex and expensive and demand is exploding. And oil resources are clearly finite and we'll run out sooner or later and there is no alternative in sight. Given these factors, the price of oil should be exploding.

Not really. Yes, demand is exploding, and supply is increasing rapidly apace. Development of new extraction technologies is expensive, because we've used up most of the really really cheap oil, but there is way, way more that we simply haven't cared enough to go after yet. It will be more expensive, for a while, and then the cost will go down until it's gone, and we need to go after a slightly more expensive energy source.

But the insane volatility of the market, and rising prices completely out of proportion with the slowly, steadily increasing cost of extraction, is most definitely because of speculation.

And come on, how is that even slightly controversial? When someone with the capital to affect the price is in a position to profit whether the price goes up or down, what do you expect to happen to the price?

{kind=link}

I think a key observation missing in all of these analyses is the most obvious one: that bottleneck is energy. What's different between 1995 and today? Well a barrel of oil cost about $25 2010 dollars back then, and costs almost $100 dollars now. We have an economy that is entirely driven by oil. When the cost of that goes up, because we've run out of the easy-to-reach stuff and have moved to expensive and difficult methods, then it's no surprise that the economic equilibrium shifts to a point with lower activity.