It looks like the Depository Trust & Clearing Corporation (DTCC) increased margin requirements on GME stock on Thursday -- which forced Robinhood to post more collateral -- which drove Robinhood's decision to prevent users from buying more GME shares.

This adds another piece to the puzzle.

We need more clarity on: Why did the DTCC make its decision? Was that decision properly communicated to the market, or did some firms get early access to the info? What conflicts of interest do they have? Was the DTCC lobbied by other Wall Street players to make that change on Thursday?

You're right. But the problem is, DTCC is a monopoly. They cover 95% of trades on wall street. Would anyone, even the SEC, dare risk destabilizing the global financial market by constraining them from taking supposedly-prudent measures to limit their risk? Because that's how they'll spin it, perhaps.

>Would anyone, even the SEC, dare risk destabilizing the global financial market by constraining them from taking supposedly-prudent measures to limit their risk? Because that's how they'll spin it, perhaps.

I mean, it makes sense. Anytime financial regulations get removed the popular narrative is that it's done by greedy wall st companies who want to destabilize the financial system ...until this time, when it's pesky regulations keeping 99% from rising up against the 1%.

I can't help but wonder if the DTCC was pressured into raising those GME collateral requirements up to 100%. After all, there is a subjective element to this decision.

DTCC needs to be investigated again. They were previously accused of allowing naked short selling[1] and their complete control of the system is problematic.

>We need more clarity on: Why did the DTCC make its decision? Was that decision properly communicated to the market, or did some firms get early access to the info? What conflicts of interest do they have? Was the DTCC lobbied by other Wall Street players to make that change on Thursday?

> We don't have to guess at the formula. It's public, as are the rules and procedures for implementing them. I've read them. They have an add-on for situations like this. The add-on has a calc. That calc has a parameter they pick, which just multiplies it by whatever they want.

> This discretionary part is intentional. It was open to public comment. People commented. DTCC responded. SEC approved.

> DTCC is definitely going to see their discretionary use of this "knob" as the system working as designed.

I didn't share this post on HN. I just wrote the article to summarize the ongoing story for my readers.

This is a developing issue with new facts and explanations coming out every day.

For what it's worth, I am trying to explain the facts in this case. A new section has been added:

> Clearing Houses & the Plumbing Behind Financial Markets

> To be clear, there isn’t any hard evidence that Citadel directly influenced Robinhood’s decision to prevent users from purchasing GME shares. The CEO of Robinhood has denied any connection whatsoever. Instead, the decision has been attributed to clearing house requirements and “market settlement mechanics”.

> This claim by Robinhood does appear to be valid. The Depository Trust & Clearing Corporation (DTCC) — a “clearing house” where shares are exchanged between buyers and sellers — is a core part of modern financial architecture, which serves to reduce risk to the system if one broker were to go bust. The DTCC requires members to post collateral. As trading volume and volatility grows, the collateral requirements also increase.

> However, it looks like the DTCC increased margin requirements on GME stock on Thursday — which forced Robinhood to post more collateral — which drove Robinhood’s decision to prevent users from buying more GME shares.

> This adds another piece to the puzzle.

> We need more clarity on: Why did the DTCC make its decision? Was that decision properly communicated to the market, or did some firms get early access to the info? What conflicts of interest do they have? Was the DTCC lobbied by other Wall Street players to make that change on Thursday?

I went back in my revision history. Again for what it's worth (perhaps nothing), at 7:53AM ET this morning, I added this sentence:

> Citadel is a hedge fund and market maker. Its success has vaulted founder Ken Griffin to a net worth of more than $20 billion. Technically, the two sides of Citadel (hedge fund / market maker) are split into two separate arms -- but they are both under one parent company and owned by Ken Griffin.

This was posted on HN (again, not by me) after I added that sentence.

Robinhood is a shady company preying on the uninformed and as such deserves every punishment it gets.

However, Robinhood clients do not get to wash their hands of responsibility, because let's be honest: what did they expect to get for a free service? Are all these people seriously so deluded that they have expected that a company will provide them free service out of the goodness of their heart? Again, Robinhood outright lied, and they must not get away with this. But we have to educate people that there are very few (if any) "free" services that won't have to resort to these antics. They have to make money somehow, and if it's not obvious how, that should be an immediate red flag.

Fortunately, there are rules that Robinhood must abide by. Perhaps in the near future, the SEC might find that Robinhood violated those rules by preventing people from buying more than one GME share.

(I get that the clearinghouse was the reason, because they upped their collateral requirement from 3% to 100%, so Robinhood just couldn't cover the trades. Nor could anyone else. But that doesn't change the reality of what happened. I wonder if it's too much to hope that the SEC will aim at the clearinghouse, or congress enact legislation to prevent the clearinghouse from shutting down specific segments of the market by suddenly requiring 33.33x more collateral for certain stocks.)

Isn’t the reality that the DTCC was forced to increase collateral requirements?

You understand that if GME drops to $80 today, a large number of GME trades from last week are going to refuse to settle. What is Congress going to do? Force the DTCC to eat the losses?

A simple solution would be to turn the 3-day settlement period into 1-day, or 0-day. But of course, DTCC has all the incentive in the world not to go along with that.

The trouble is that the 3-day period is a "leaky abstraction." It's the sole reason any of this became an issue. It's not a law of nature that "DTCC must insure 3 days of risk."

>A simple solution would be to turn the 3-day settlement period into 1-day, or 0-day.

Unless you cut the settlement to 0 the issue will remain. The fundamental issue is that 1) deposit is required, 2) there's a spike in demand/deposit requirements, 3) current reserves can't pay for deposits. Going to 1 day settlement will just cause brokers to reduce their overall reserves in response (no need keeping all that money around!), so the next time a spike occurs the same issue will occur.

It's well-known how Robinhood makes money. They sell data they have based on tracking their user's habits within the app.

This "it's free so what do people expect" is such a ridiculously lame excuse as well. No, it's not free. The user is just not the one paying. If the app sells the data and offers a service in exchange then they better offer that service.

But the user is the one paying - they get a worse execution than they could have gotten. The difference is split between RH and Citadel. The user does not have to shell out cash per transaction, but they will pay for the service one way or another.

TBF there's an enormous precedent to these kinda of financial infrastructure things being free: Retail Banking.

And it's worth noting that Robinhood isn't the one who forced big brokerages to do zero-free equity trades; it was Schwab doing it purely because 1) their income streams were generally not dependent on trade commissions and 2) they were predicting that executing retail trades was going to quickly become a commodity that costs pennies or nothing, so why not get a big PR boost by just cutting straight to zero, while dealing a large blow to competitors who did rely on that (outdated) business model?

So I'd argue that their service being no-charge-to-most-users (you do have to pay for "real" margin accounts, extended hours trading, etc) is actually unrelated to all the shady and, imo, negligent things they do.

I agree that they're shady, and moved my account out last week, but their pricing is exactly the same as Fidelity, Schwab, and Vanguard. Would you recommend using a broker that charges a commission to buy?

There are countless controversies involving Robinhood.

One that I only learned about a few days ago involves an investor who was erroneously shown a -$700K balance on his Robinhood account and then killed himself as a result[0].

Back in September of 2019, I made a deposit into Robinhood. The next morning I received an automatically generated email saying that the deposit had bounced and that my account was now limited. I checked my bank account and saw that the funds had indeed been removed. The email included the ACH error code "R26", which corresponds to a malformed ACH file. I quickly learned that every single deposit on that date had failed [1].

No worries, I thought, I'll just email support and let them know. Unfortunately their support was completely useless and did not follow through with what they said.

I switched to TD Ameritrade (and the thinkorswim platform) and have not looked back.

I think Robinhood needs a sort of Uber-style restructuring. It's clear they do not care about their clients.

Robinhood did not show an error in that first example, that was an option spread where one leg was exercised and waiting on the other. It’s the whole reason for using option spreads and any other broker would show the same.

Stories like this are why I've stayed away from Robinhood. After doing more research before starting any trading, I learned that I can buy stocks through Vanguard, which is a platform that I actually do support a lot.

One question I have is: what's a safe, secure, reliable alternative to Robinhood for buying crypto as an American? I've read about Coinbase and Binance but seen that some people have had shady experiences with them too.

No company has perfect service but Coinbase has always done right by me. Great security and super easy onboarding. Whenever a friend asks me how to buy crypto, I send them to CB. My only criticism would be the lack of some coins with real value and communities like Monero, NANO, or NEO.

Thanks! Is the process like with traditional trading, where you transfer money into the Coinbase account from your bank, and then buy whatever? Do you transfer coins to a physical wallet?

Yeah! You'll connect your bank account and do some security verification. Once approved you can buy whatever you want.

Although depends on what you mean by traditional trading. If you want see details charts and create market orders or limits, things like that, then you'll want Coinbase Pro.

Coinbase is great for easy buying and then holding there in your wallet. You can either leave your coins on Coinbase or transfer out to a hardware wallet like Ledger or Trezor. If you go the hardware route, stay away from Ledger. Pretty solid wallet but the handling of their customer data break was pretty unfortunate.

When their servers were under heavy load, you could attempt to place and it would error, but then you would get an order confirmation later saying it went through. The best part is that even though it didn't execute, you weren't able to cancel it because the transaction didn't display anywhere.

The author only presents the GME

Citadel conspiracy theory without even presenting the "capital requirements" theory. He even says that there is no evidence of this conspiracy theory.

This is what writing looks like when the author appeals to your emotional distrust of wall street, rather than to actually try to inform you.

It looks like the Depository Trust & Clearing Corporation (DTCC) increased margin requirements on GME stock on Thursday -- which forced Robinhood to post more collateral -- which drove Robinhood's decision to prevent users from buying more GME shares.

This adds another piece to the puzzle.

We need more clarity on: Why did the DTCC make its decision? Was that decision properly communicated to the market, or did some firms get early access to the info? What conflicts of interest do they have? Was the DTCC lobbied by other Wall Street players to make that change on Thursday?

Please don't cross into personal attack, even when someone else is misinformed or you feel they are. The cost of a putdown like this is higher than its benefit. Perhaps you don't owe article authors better, but you owe this community better if you're participating here.

If you know more, that's great, but then please share some of what you know so the rest of us can learn.

"That Robinhood sold its order flow is unremarkable, but the scale of its activities certainly merits comment. Forbes reports that in the first quarter 2020, 70% of Robinhood’s revenues derived from payments for order flows, as opposed to 17% for E-Trade and just 3% for Schwab. Yes, Robinhood has observed standard practice–but with distinctly above-average enthusiasm."

I, too, am curious what these conversations sound like, or if they even happen at all. When I googled GME this morning I saw article after article claiming that 'Wallstreetbets has set its sights on Silver', however every single post on the WSB subreddit was against the idea.

The explanation is probably innocent. Most of these websites rely on ads, and when 1 of them reports on 'the hot new GameStop - Silver!', they probably all jump on. Still, it doesn't help the image that the media is being bought left and right.

I'm not really sure how Robinhood survives this debacle. Their brand is toast, and the moat of free commissions is gone now; it's the industry standard at this point. They were looking at being the most anticipated IPO of 2021, all down the drain for a few poor decisions.

They’ll be fine. Not only do they have a massive increase in their equity base (though at a high cost), they’ve also had a record number of downloads the last week, and the entire episode has grown their client base significantly.

Most people haven’t heard whining of the Reddit Stonks-Newbs about Robinhood, they’ve heard “Robinhood gives you free stock trades”

I'm getting really sick of the Saga. Plus the poor are not the people buying $$$ worth of gamestop last week, they're trying to afford basic bills. Bored middle class millennials maybe, more likely just other rich people and hedge funds.

I would agree but I would say all bored Millennials are buying stocks because the RH app is truly addicting and makes buying stocks as easy as giving a like on FB. It’s pretty much a slot machine in your pocket. The biggest problem though is “Millenials” is no longer a term for the young but rather a term for majority of the countries work force.

> more likely just other rich people and hedge funds.

I have at least two friends with absolutely no experience in any kind of investments who installed mobile trading apps and bought GME shares a few days ago at $300+ a pop

I'm fairly certain that a lot of people who are far from rich are buying GME stocks right now because a lot of other people are telling them the stock will "likely go over $10k a share" (I've seen it on the wsb subreddit a lot).

FOMO is a serious thing, low barrier to entry + constant media coverage = people want to be part of "it", even if they don't know what "it" is, especially when you tell them they could get rich.

Wow, they put so much effort into a multi page blog post, yet

1) Misreport the Melvin funder as the market maker Citadel, when it was the investment fund Citadel. Two different entities.

2) Hand waves away settlement issues altogether (never mentioning the DTCC), when they are the heart of the issue. If Robinhood has to post large amounts of collateral for every GME purchase (and sales reduce the collateral requirements), doesn’t that directly explain their behavior? No conspiracy needed?

So little actual insight in a blog reporting to do a “deep dive” into the situation.

And what market maker has not been fined for rule violations before? How is this pertinent?

We know the DTCC raised the collateral requirements by 30x for GME. Does Ken Griffin own the DTCC too?

We know Robinhood suffered a cash crunch and was required to raise an emergency $1B. We know that every GME purchase by its customers increased its collateral requirements, and every sale reduced them.

Don’t all known facts directly explain Robinhoods behavior? Wouldn’t Robinhood simply move to another market maker if Citadel got out of line?

Does anyone know that Ken Griffin made any demands of Robinhood?

So why are we pursuing baseless conspiracy theories when the facts already explain the behavior?

> Citadel is a hedge fund and market maker. Its success has vaulted founder Ken Griffin to a net worth of more than $20 billion. Technically, the two sides of Citadel (hedge fund / market maker) are split into two separate arms — but they are both under one parent company and owned by Ken Griffin.

> Over several years, these short trades drove down the price of GME shares to ~$4 per share.

People keep saying this, but I just don't see how this would work in the real world.

NOTE: I am not a financial professional, what follows is my meager understanding. Please feel free to correct me with facts and information.

Here's how it COULD work, but DID NOT work: Hedge funds short so much stock, SO QUICKLY that the increase in virtual inventory drives the share price down. Here's why it DID NOT work that way: The hedge funds did not actually do this. They kept their short position open expecting GME to go to 0.

In fact, if hedge funds DID attempt this, it would certainly be market manipulation, which is something the SEC definitely watches for, especially when large players do it.

People keep saying things like predatory shorts drove the price down. As far as I can tell, these hedge funds told a story about why they though GME would go bankrupt. In turn, someone started a story about how this particular trade by these particular hedge funds was EVIL, which is just zany to me.

----

I do think that Hedge Funds and Traders accumulate too much money for themselves. I don't think the GME trade is a particularly good way to fix this. There are plenty of other Hedge Funds out there.

Right, I would need some strong evidence to believe that actually happened in this case. In the linked case it was a VERY low value stock aka Penny Stock, aka OTC (over the counter, as opposed to a listed stock as in listed on a stock exchange), and the SEC DID take action against the guy. In the case of listed stocks, there is a lot more attention and regulation built into the system.

Those contracts are generally secret. You have to trust your broker will negotiate a good split on your behalf. (Or hope the SEC will smack them if they don't, as happened to RH.)

> This practice meant that trades placed on Robinhood weren’t executed at the best price, costing customer tens of millions of dollars, even after taking into account the savings from not paying a commission

This is why I stopped using them last summer. They messed up a few of my trades. Either by giving me a worse price than was quoted or my reversing the trade after it had already gone through.

After it happened a second time in a short time frame, I knew something was up. I closed all my trades and took all my money out.

What's really weird is that these "errors" started happening only after I started making good trades. When I lost money on a trade (which happened a lot for the first few years of casual trading), I NEVER had an execution error. Then, when I had my first good run of trading in years, all of the sudden I had TWO trades messed up within a week of each other???

It was all too conincidental for me. Either they were messing up my trades because of incompetence or they were letting someone take the other end of my trades.

Whichever it was, I left.

Robinhood had an insane run of good press and was able to within years of crap product. Now they are finally getting what's coming to them.

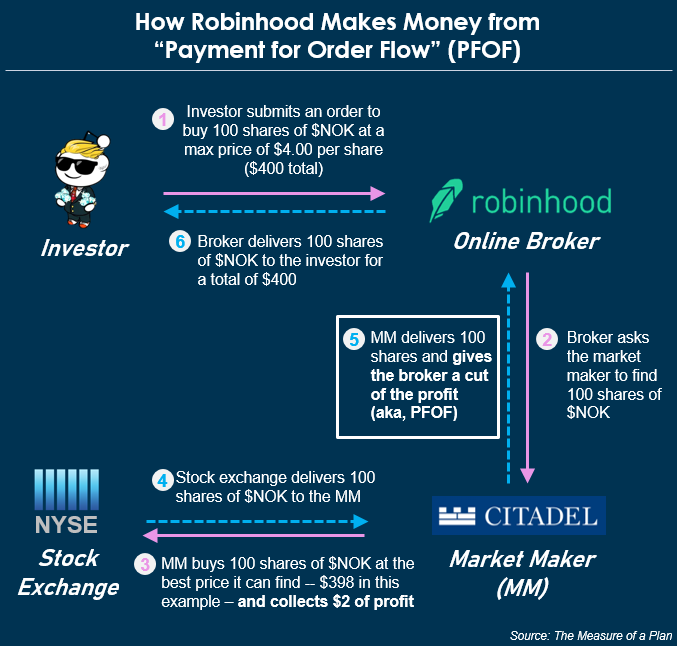

> As we saw above, Robinhood’s main revenue source comes from selling customer trade data to other firms. This is a controversial practice known as “Payment for Order Flow” (PFOF in financial regulatory lingo).

It's only controversial among people who don't understand how market transactions work.

The article is a bit confusing. There's "PFOF" which is basically middle-man profit taking. That's not particularly shocking unless it's egregiously delayed. But then there's selling data to high frequency traders.

This sentence in the article conflates these two very different things...

> As we saw above, Robinhood’s main revenue source comes from selling customer trade data to other firms. This is a controversial practice known as “Payment for Order Flow” (PFOF in financial regulatory lingo).

I am not getting this? Is it the case that ordering stock shares from a market maker like Citadel is identically selling data to high frequency traders?

FWIW, I admit I don't _really_ understand how market transactions work, and I definitely don't feel alone!

>The article is a bit confusing. There's "PFOF" which is basically middle-man profit taking.

Not really. The middle-man profit taking (aka market making) will exist even without PFOF, it will just move onto the open exchanges. The only difference would be that the market makers would have to offer worse spreads because they can't separate "dumb" order flows from "informed" order flows. This is an overall negative for retail traders but a net positive or neutral to hedge funds/institutional traders.

Payment for order flow can certainly be controversial among people who understand the market. Also, there are plenty of people who understand the market who find the concept of the market controversial.

Your circles might all be comfortable with PFOF, but I wouldn't say it is controversial only with those who don't understand the market -- it's dismissive of contrary opinions.

Oh, enough with the conspiracies already. It's probably flagged because of the poor quality of the article that other commenters have pointed out. The first illustration alone was enough for me to think to myself, "meh, best skip the rest, I don't think the author is knowledgable about how this works."

I stopped reading at the first image: https://themeasureofaplan.com/wp-content/uploads/2021/01/Rob..., which implied that the market makers were offering robinhood a worse price than the exchanges, and pocketing the difference. This is not what happens. Matt Levine explains:

>Market makers stand ready to buy or sell stock from or to customers; they try to buy for a bit less than they sell at, and pocket the spread. If you go out into the market and say “hey I’ll buy anyone’s stock for $10,” and a really smart hedge fund comes to you and sells you stock for $10, that’s probably bad. You’ve probably made a mistake. The hedge fund is selling you the stock for $10 because it knows it’s worth $8. This is called “adverse selection.”

>More subtly, if a really big mutual fund comes to you and sells you stock for $10, that also may be bad. The mutual fund is probably selling lots of stock, because it’s so big; it sells you a little, then sells a little more, then a little more, until it pushes the price down to $8. The mutual fund isn’t necessarily smart, but by virtue of being big and doing big trades, it moves the price; if you are on the other side of its trades, you get run over. This is also a kind of adverse selection: You buy at $10 and are stuck selling at $8. Part of the spread that market makers earn in public markets—the difference between their buying and selling prices—compensates them for adverse selection, the risk of being run over by a counterparty who knows something they don’t.

>Market makers, the textbook theory goes, would much rather trade with retail orders. Retail investors generally don’t know much, so if you buy stock from them you’re probably not making a mistake. And retail orders are generally small and uncorrelated: One investor buys a little, another comes along a moment later and sells a little, it’s all pretty random, and you’re not facing an avalanche of steady sell orders that push the price down. Trading with retail is so nice that market makers—wholesalers—will both give retail orders a tighter spread (pay more to buy their stock, charge less to sell stock to them) and pay their broker for the privilege of doing it.

In fact, they're specifically prohibited from offering a worse price than the public exchanges due to regulation NBBO (national best bid order). The SEC penalty last year was only for failing to ensure best execution, which is slightly different than offering worse prices than the NBBO, since the former also requires them to take into account other market making firms that might offer a better price.

> We should reserve final judgement on this matter until all the facts come out, but it’s clear that this deserves a thorough and transparent investigation. The conflict of interest between Robinhood and Citadel is just too great.

This. A thousand times this.

I'm so sick of people dismissing everyone's concerns as as conspiracy theories. There is a clear motivation for RH's actions, basically nothing stopping them from acting on that motivation, and billions of dollars on the line. Their alibi seems to check out, but that doesn't mean they acted appropriately or that we shouldn't investigate them to be sure.

There is zero conflict of interest between Robinhood and Citadel investment Group (the investor in Melvin), because they do no significant business together.

Robinhood pays Citadel Securities for order flow, which is an entirely different company.

Citadel Securities is a subsidiary of Citadel LLC (aka Citadel Investment Group). If RH upsets Citadel LLC (the ones who invested in Melvin Capital), then you can be certain they will also upset Citadel Securities (the market maker who account for 45% of RH's PFOF revenue in Q3 2020). The conflict of interest looks pretty clear to me.

So if I understand this right, Robinhood destroyed their own reputation and greatly damaged their business, not because the DTCC increased collateral requirements 30x for GME and forced them to raise a billion dollars, but because an easily replaceable market maker asked them to?

The destruction of RH's reputation is irrelevant. Thanks to the increased collateral requirements, They were facing liquidity issues and had to restrict buying of GME. There was no way around that.

The problem is that they continued to allow customers to sell GME and lied about their rationale to their customers who could no longer buy it.

If a large broker exclusively allows a stock to be sold, not bought, the trajectory of that stock's value will be pushed downward. It's in RH's interest to see GME go down (or at least go up slower). Lower prices mean less of a liquidity problem for them. It also really helps out their biggest market maker partner.

It would not have been a conflict of interest if RH prevented customers from trading GME outright while they got their liquidity issue patched up. It would piss off potential sellers and, if the stock price went down, would result in objective losses for them which, IMO, RH should be liable for. That is a tough choice to make, but it would eliminate the conflict of interest.

A stockbroker's value is in enabling customers to easily trade their stocks. If they cannot do that, they deserve damage to their reputation. If they cannot do that without engaging in conflicts of interest, they deserve to be investigated. Last week they failed on both fronts.

So basically you agree that Robinhood stopped purchases of GME, despite the massive reputational risk it entailed, because they faced a very real risk of insolvency.

Nearly destroying your firms Brand as a favor for an easily replaceable market maker doesn’t pass any rational test.

> So basically you agree that Robinhood stopped purchases of GME, despite the massive reputational risk it entailed, because they faced a very real risk of insolvency.

I never said anything otherwise.

> Nearly destroying your firms Brand as a favor for an easily replaceable market maker doesn’t pass any rational test.

I cannot speak to how "easily replaceable" Citadel is. Given that RH chose them so much more over other market makers in recent years, I can only assume that Citadel's destruction would result in at least some financial loss for RH. I do not know what the extent of that loss would be, though. I suspect they would probably not consider it alone to be worth the damage to their brand.

While their action might have improved their relationship with Citadel, I agree that they would probably not consider it alone to be worth the damage to their brand.

There is also the matter of it being in RH's own best interest to have GME stabilize (and ideally decrease), regardless of any relationships they have with any market makers. As collateral requirements decrease they would be able to facilitate more trades, which is how they make money.

As someone speculating from the outside, I cannot say whether all or any of these factors were considered as part of the decision to restrict GME purchases while continue to allow sales. Maybe the idea of restricting sales never even crossed their minds. Maybe they just thought it would hurt their reputation even more. Maybe they thought it would open them up to liability if the stock value decreased.

The thing about conflicts of interest is you can make rational decisions despite them. But those on the outside can never be sure about your motivations. Hence why I believe an investigation is needed - especially when there are billions of dollars on the line.

> Citadel is a hedge fund and market maker. Its success has vaulted founder Ken Griffin to a net worth of more than $20 billion. Technically, the two sides of Citadel (hedge fund / market maker) are split into two separate arms — but they are both under one parent company and owned by Ken Griffin.

What are you talking about? I read that in the article before I even made my post. Don't slander people with false accusations like that.

EDIT: I even still had the browser tab open from when I first read it. I opened the page up in a new tab and ran a diff between them. There was no difference anywhere in the article.

I wrote one of the first comments about the article when it was first posted. I specifically noted the authors confusion on Citadel because the new language was not there.

I went back in my revision history. Again for what it's worth (perhaps nothing), at 7:53AM ET this morning, I added this sentence:

> Citadel is a hedge fund and market maker. Its success has vaulted founder Ken Griffin to a net worth of more than $20 billion. Technically, the two sides of Citadel (hedge fund / market maker) are split into two separate arms -- but they are both under one parent company and owned by Ken Griffin.

This was posted on HN (again, not by me) after I added that sentence.

{kind=link}

I've been learning more about that over the past 24 hours thanks to reader comments on reddit.

Some background info:

https://www.washingtonpost.com/business/whats-the-dtcc-and-h...

https://twitter.com/KralcTrebor/status/1355356755690139650

It looks like the Depository Trust & Clearing Corporation (DTCC) increased margin requirements on GME stock on Thursday -- which forced Robinhood to post more collateral -- which drove Robinhood's decision to prevent users from buying more GME shares.

This adds another piece to the puzzle.

We need more clarity on: Why did the DTCC make its decision? Was that decision properly communicated to the market, or did some firms get early access to the info? What conflicts of interest do they have? Was the DTCC lobbied by other Wall Street players to make that change on Thursday?