This is really scary. The whole western world is in for a rude awakaning in the coming years with regards to retirement.

Retirement is the golden carrot dangled in front of us for all our working lives, an embodiment of Protestant work ethic - "work hard and you will be rewarded in the end". However, very much has changed since retirement and pensions were designed. I can't find a good source, but (in Sweden) when pensions were introduced after WW2 people worked from their late teens until they died (40+ years of productivity), produced 3 or more children per woman (good population age distribution, the classic "pyramid") and the average lifespan was 64 years (1 year before retirement).

Nowadays, many of my peers don't get a "real" job until their early/mid-thirties (work for 30 years of producitivty), produce 1.7 children per woman if they reproduce at all (leading to a top-heavy population where fewer and fewer young people must support more and more old people) and life expectancy is much, much higher. Now, these things are in of themselves good, but they break the original design horribly. I really, _really_ hope that we can cross the chasm to a robot-centric/base-income society before it all breaks down.

"Nowadays, many of my peers don't get a "real" job until their early/mid-thirties (work for 30 years of producitivty), produce 1.7 children per woman if they reproduce at all (leading to a top-heavy population where fewer and fewer young people must support more and more old people) and life expectancy is much, much higher."

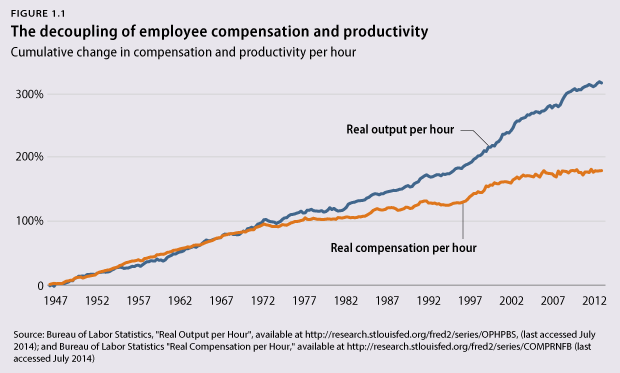

With increases in productivity, this could be sustainable, but as this article points out, wages have basically stagnated in comparison since ~2000.

This is the basic issue. Liberal capitalism made a de facto deal in 80s. Lower taxes for business, create more jobs but with less benefits, resulting in lower intake for governments but the losses will be made up through income taxes through higher wages. Except that deal has turned out to be rubbish, businesses continued to find ways to lower taxes (Ireland, BVI, Netherlands, transfer pricing etc). At the same time wages were held down. The gains of course were largely grabbed by the top 1 percent.

I'm a capitalist but I know that this is no longer sustainable. Fundamentally there comes a point were failure to raise wages means your customers can longer afford to buy your stuff. So your biting the hand that feeds you. Then you end up with the customers creating a credit bubble to try and replace what they have lost through low wages, resulting in sub prime crash, US student debt etc etc

The situation was never sustainable from the beginning as the economy has actually been rigged and obfuscated since the collapse of Bretton Woods.

It comes down to a confluence of r vs K effects on politics (and it's knock on effect on higher education and student debt), the Fed being a private bank masquerading as a US Government institution, fiat currency, and fractional reserve banking. This is the actual cause for inflation (which erodes the purchasing power of wages), and the so called "business cycle" of boom and bust (e.g. the credit bubble). Globalisation has also further exacerbated wealth transfer and increased the risk of systemic failure.

But this is not actually liberal capitalism's fault. Crony capitalism and Government intervention is to blame. There is nothing "liberal capitalism" about tax payers selectively underwriting shareholders. Under a "liberal capitalism" doctrine, the market is allowed to reward winners and punish losers.

If anything liberal capitalism is the only way to save the system but it will be an extremely rough transition.

> (good population age distribution, the classic "pyramid")

I would say that this is part of the problem: relying on something that is basically a ponzi scheme. Of course the European social systems work if you can constantly increase your population. But this doesn't work in the real life - the area of the country doesn't increase, therefore you can't increase your population infinitely. The reason young folks nowadays don't have 3 kids is that it's just not economically feasible any more. Add the fact that the top of the pyramid is getting wider every year (life expectancy is increasing) and here we are. The system was flawed since the beginning and now we are hitting the limits.

Ponzi schemes are much more common in nature than humans like to think. The default population dynamics for most species are feast-or-famine: population grows exponentially until it exhausts all available food sources, and then mass numbers of individuals die off all at once, leaving more resources for the survivors. Hell, life is a ponzi scheme: our cells divide, accumulating genetic mistakes (= technical debt) each time, until our body's ability to repair the damage is overcome by the accumulated mistakes. And then we die, hopefully having produced a fresh new individual to repeat the process.

Assuming no great technological breakthrough, the same thing will happen on a societal level: we'll die. But then, we knew there was 100% chance of that happening from the beginning.

> The whole western world is in for a rude awakening in the coming years with regards to retirement.

No kidding. Who will pay for all the people who didn't save? The people who did. I have very little expectation of keeping most of my money as I get older.

>Who will pay for all the people who didn't save? The people who did.

Correct. It is generally a good idea to consider all of the money being paid into Social Security to be completely wasted. I am in my early-mid 30s and I do not expect to see a dime of it. I think it will either be insolvent or subject to some ridiculous tax structure if people have earned X dollars in their lifetimes or spent too many years in high tax brackets (which I expect to in my late 30s and 40s).

Taxes will also go up dramatically as the years go by. I have a maxed-yearly Roth IRA but I also don't expect the government to keep their promise on letting me take out 100% of it tax-free despite all my contributions being post-tax. I expect to be double taxed on that, because, well, why not?

Retirement is ridiculous. It's just generally safe to assume all of your money is going to be taxed at a much higher rate and through loopholes/broken promises by the government. We face a really huge shortfall in the next few decades in public welfare programs, Social Security, and other tax-advantaged vehicles that I doubt will be honored down the line.

Just out of curiosity, what's preventing the US from implementing changes to Social Security that are sustainable? I read up on this for Norway a few months ago, and was actually pleasantly surprised at the thought that's gone into the sytem.

Norway's public pension system is now funded by every employee having 8% of their salary taxed away and earmarked to retirement. The money is placed in a broad stock and bond fund. In retirement, the earmarked amount of money for each employee is paid out in a monthly amount that matches the life expectancy of the retiree.

E.g. if the employee has paid $150.000 to the system over a lifetime of work, retires at 65 and the life expectancy for this age cohort is 10 years, the annual payment will be $15.000. The state covers for retirees that live longer, keep the money for retires that live shorter and provide a guaranteed minimum for people who reach 67 without saving up a minimum amount. To offset this, the possible monthly payment is capped with a maximum for high earners. There is also some inflation adjustment built in.

In effect, this provides a living wage for all retirees, with additional private savings required if you want to maintain a higher standard of living. The system is self-contained and is not based on younger workers paying the pensions of older workers.

>Norway's public pension system is now funded by every employee having 8% of their salary taxed away and earmarked to retirement.

Social Security payroll taxes are ~15% of salary per employee, so assuming Norway doubles the 8% (employee responsible for half, employer responsible for the other half) that's not much higher than the United States' system.

>The money is placed in a broad stock and bond fund.

Social Security is not privatized in the United States and efforts to do that by Republicans are regularly shot down. Social Security is an annuity that is tax-free and inflation-adjusted. The average ROI is about 2-4% for single, average salary employees who work full-time.

EDIT: Forgot to add, the United States excess funds in Social Security are loaned to the government for use for non-SS purposes. The government owes the Social Security program something on the order of $5+ trillion right now, which makes up over 25% of the national debt. Yes, you are reading this right. No, it is not a good thing.

You could argue that Social Security could do a lot better if citizens were allowed to control that money or if it was simply invested in a total stock/bond market index fund, but then you'd be incurring significant risk as well.

>In retirement, the earmarked amount of money for each employee is paid out in a monthly amount that matches the life expectancy of the retiree... The state covers for retirees that live longer, keep the money for retires that live shorter and provide a guaranteed minimum for people who reach 67 without saving up a minimum amount.

This is basically how it works in the United States, except:

> To offset this, the possible monthly payment is capped with a maximum for high earners.

This is likely to happen in the United States as the country moves more economically liberal (current administration excluded, but even Trump has some economic policies that old-timer conservatives would never agree to). We currently don't have this. But taxes and fees and other such efforts will be successful against the rich soon enough here.

>The system is self-contained and is not based on younger workers paying the pensions of older workers.

This doesn't really make sense. Your example describes this to a T.

Tell me: What happens when the "broad stock and bond fund" collapses in a thirty-year low for a period of six years and pension promises far outpace receipts? Who will pay for this? The state will cover, correct? Well, that's younger people paying for older people no matter how you slice it.

>>Norway's public pension system is now funded by every employee having 8% of their salary taxed away and earmarked to retirement.

In general this how any pension scheme is supposed to work. Except that it doesn't. When you start to add things like exceptions whole scheme starts to come apart after a while.

Pensions are one of those things which are ripe for abuse. Also you need to start looking at other benefits that come along with it like health care. Then there are unions that graciously award over time work to employees to drive up their compensation in the last few years of work.

There are also other things going on like inflation adjusted pensions.

In India there was a recent drive to include One Rank One Pensions for armed forces, which demands pension revisions every single year based on last highest pension paid in that rank for that year.

It's not retirement that's ridiculous, it's that old people have a vote in this and because that vote is so overpowering, no-one will even try and fix the issue until it's too late.

Double taxation is extremely unlikely, and would likely have to be of the form of applying a tax to earnings in the Roth IRA or something like that. Which is how other investment-related income is taxed anyways so, I don’t know.

Additionally, SS pays out at 75% of projected levels at the height of the retiree crunch, so assuming the program will just vanish is not something a lot of financial advisors are going to consider. Given the universe of possibilities, the one that doesn’t result in people with pitchforks is probably the one that we will go with. We could also solve this problem today with a 1.8% addition to the payroll taxes, removing means testing, etc. It’s a problem to be solved but expecting the world to burn in the process of solving it, the magnitude just isn’t there. Makes for good fan fiction though :-).

>>and would likely have to be of the form of applying a tax to earnings in the Roth IRA or something like that. Which is how other investment-related income is taxed anyways so, I don’t know.

Correct, this would be a huge breach of trust by the federal government. Which is nothing new, obviously, but....

There's some business-related reasons why I don't (I don't yet make enough money in salary for it to matter wrt deductions) but also because I think taxes will be very high when I retire and that my Roth will be taxed at a relatively low rate, subject to some "fees" or something.

I think the Roth will still exceed the value of a traditional IRA (plus it's only $5500/year, hardly huge as I get older and my net worth increases), but I would be willing to bet that the Roth IRA will not exist in the form it does in 20-30 years, and that existing ones will be subject to a tax/fee to make it "fair."

Depends how history plays out in the future. If people who save end up paying for people who didn't, it implies one of three things: 1) financial panic 2) inflation or 3) taxation.

All of these are fairly likely, but looking back at history, there are a number of other possible futures that would take care of the problem. Mass plague, where all the old people die off. Mandatory euthanasia, where the government kills all the old people. War or anarchy, where both young and old die indiscriminately. Colonizing other planets, which opens up vast new resources. Mass automation of health & elder care, so the robots pay for the people who don't save.

The depressing thing is that most of these are pretty horrible, and the two that aren't - automation and spaceflight - are probably the least likely. But then, history is filled with black swan events that open up human frontiers that nobody could've imagined. Maybe one of them will save us.

Or like it worked in most socialist economies which gradually migrated to free market in the 90s.

Older people make painful sacrifices to merely survive. Younger population doesn't care, and largely thinks the old deserve it for not being serious about their retirements in young age.

Social security in that situation will largely depend on continuing to work in old age, and surviving on bare minimum money and at worst depending on kids and friends.

War and anarchy aren't feasible in old age, when you get knee pain for walking across the street. The whole thing will be bad, its just people have to deal with it and move on.

It wouldn't actually matter. The problem is demographic, not financial.

Ultimately, somebody has to produce the resources, goods, and services that every person on earth needs to survive. If people live an average of 5 years after retirement, work for 50 years, and the population is at a steady-state, then every elder is supported by 10 workers. If the population has doubled in the last generation, then it's 20 workers. If the population is still doubling but people are now living for 10 years after retirement, then it's still 10 workers/elder. If the population returns to a steady-state but people now live for 20 years after retirement, though, we're down to only 2.5 workers/elder. Suddenly everybody feels the pinch.

Pensions, 401ks, stock market growth, and all other forms of retirement savings are just different ways of lying to ourselves. Ultimately, goods have to be produced, services have to be rendered, and money is just a way to track who has done that and reward them appropriately. If you have fewer people doing the work and more people depending upon it, standards of living will fall.

If I had to bet on a (peaceful) solution, it would be automation. Do more with less and a given number of workers can support a much greater number of dependents; the only challenge then becomes redistribution in a way that people find adequately fair. But elder care has proven stubbornly resistant to automation: if you've ever had a family member in their 90s and tried to take care of them at home, you may be doubting that it's even possible for 2.5 workers to take care of one elder, even if their own needs were completely automated away and they had no children.

"It wouldn't actually matter. The problem is demographic, not financial."

It's interesting how many people don't understand (or don't want to understand) this.

Money is just a number, is real resource what is important.

Never mind how many savings the people have, if there are not enough people or resources to do the necessary jobs.

And, the other way works too, never mind how many old people there are without savings, if the productivity is enough to take care of them easily.

The obvious conclusion is that, instead of caring about money "saved", we should be caring about getting more productive. That would mean improve technology, increase knowledge and training.

My problem with "getting more productive" is that the gains nowadays are achieved through automation (capital investment in general) which pretty much guarantees that the gains from the increased productivity are captured by the capital owners. So even if we double the productivity of the economy, there is no guarantee that this will improve the lives of most people who depend on salary or pension. There must be some form of redistribution to allow sharing the gains of productivity but this has been a taboo in the US (and many more places) since the 80s and I don't see this changing anytime soon.

Even if it were a problem or resources, the solution is invest now in creating more resources, not in "saving money".

I think that part of the reason it's a taboo, is because the officially pushed narrative is designed to hide that, in many instances, is a problem of redistribution more than a problem of resources.

For instance, in USA, the "public debt crisis problem", that it's mainly meaningless, distract from a honest debate of the real issues.

> That kind of runaway automation that could pay for this kind of a party isn't close

Automation is already here, and has been for a long time. The whole point of the industrial revolution is about automation: Machines that support or replace human workforce.

The explosion in availability of computing power in the last two decades put automation into overdrive, and I don't see it slowing down.

Meanwhile, the gains of automation do not directly translate in inproved wealth for all members of society.

For example, if a company replaces 50% of its workforce with machines, they might make more money because they save on salaries, but effectively worsen the situation for the pensions of the layed off people.

This idea is not without drawbacks. Mandatory pension systems have a history of being wiped out by extinction events both governmental (USSR et al) and corporate (Kodak and other midcentury megacorps).

It's at least something I guess, but retirement planning is a really really long forecast horizon and is inherently risky.

In Germany the retirement system is far from perfect - but it at least keeps (most) people from being homeless or starving.

The lack of universal health insurance in the USA is basically traceable to the same societal shortcomings. Why should a rich banker support with his premium health insurance for a woman who gets pregnant - as he's not getting pregnant anyway. That's a very egoistical way to look at communal cooperation but at the end of the day the reason for why ACA is being sabotaged by many politicians.

I assume by "woman" you meant someone who is at or below poverty line, if so, I (and most people) don't have a problem chipping in.

The point you are missing is that right now, 90% of the US population cannot afford to pay for child-birth (or any other medical procedure) themselves (out of pocket), as they typically cost $20K and up.

With a reasonable market- (or single-payer-) based health-care system, most people (except for the poor and almost-poor) would be able to pay for their own health care. The current "system" in the US is a scam of major proportions.

> Retirement is the golden carrot dangled in front of us for all our working lives ..

And then:

> .. and the average lifespan was 64 years (1 year before retirement)

Wouldn't it be more rational to try to get as much happiness and fullfillment from the years you spend working and healthy, instead of waiting for those few years you might have after your retirement? And maybe, if you don't have much money to spare, it would also be more rational decision to spend your money now instead of saving it for an age which you might never even reach ..

You make some good points. Working yourself to the bone until retirement is probably not the best approach. Spending ALL your money is maybe a bad idea though.

My plan is in the middle somewhere. I earn a decent living, and have a modest pension. The plan though is to save enough for a large piece of land in a cheap but stable country (inasmuch as THAT's possible - current thinking is Austria or South Africa), with a house, and then become self-sufficient on that land. Until I cash in my chips.

>The whole western world is in for a rude awakaning in the coming years with regards to retirement.

Most Western countries have mandatory pension systems in place. In my country, NL, everyone has to pay money into pensioen funds that invest it for you.

Sadly, in most of the Western countries, your pension payments go to paying the pensions currently being handed out. By the time you'll need yours, unless something changes, there won't be enough money to pay it.

That's why you're now encouraged to enlist in private pension saving plans and all those things.

We only do that for the government part of the pension. your additional pension is saved up and invested for you. Currently there is about 2 trillion USD in the Dutch pension system.

>Retirement is the golden carrot dangled in front of us

Not exactly. The 1% keeps pushing the "demographic time bomb" trope through the media precisely to make us believe that that this "golden carrot" is a vain hope.

300 years ago, 80% of the population had to work in agriculture just to keep the country fed and alive. Now, less than 5% work in agriculture and we produce so much food, that supermarkets have to throw more than half of what they buy.

Productivity has been growing in a exponential way since the beginning of the industrial revolution. Automation will allow many of the products we consume today to be produced almost without human intervention.

My point is that we, as a society, will be able to maintain the same standards of living (or increase them) while the workforce shrinks.

The only issue here is how the wealth produced by the automation will be distributed, but I can imagine a future where people is actually employed during less than half of their lives and still live well enough.

An alarming number of people I know who had high flying careers and who retired with huge pension funds died within a relatively short time of retiring.

Maybe its something weird about my extended family....

What makes me angry about this is that politicians in industrialised nations have no qualms with bailing out current retirees (because those will save them their next few re-elections) and shoring up mindless consumption at the expense of those who try to live more frugally.

Yet at the same time the very same politicians claim there's not enough money for implementing a universal basic income right here, right now.

I have 3 kids. I earn a decent wage but nothing excessive and my wife doesn't work (she looks after the kids). We live in a city, don't own a car and walk or bike most places.

They don't cost that much more if you're willing to be sensible (each kid doesn't need a TV and a games console or even their own bedroom). We're very moderate on how we spend our money - we don't blow thousands at Christmas just to give kids tat they won't play with, we keep clothes and re-use them as the younger kids grow up. We eat at home as a family, don't take extravagant holidays etc etc.

It's most expensive to have 1 child - then each child after the first is cheaper to raise, especially if they are of similar age. Once you get to 3+ kids it almost makes no difference. But, it depends very heavily on your lifestyle. If you think that every child needs their own bedroom, they all have to go to private schools, they all have to go to Disneyland every year, if you have to pay for healthcare and/or kindergarten, then yeah, the costs are exponential. But if you live in any modern country with good social care(this does not include US) and you think kids can survive without luxuries, then yeah, it's actually completely doable.

In France a large part of childcare is subsidized : kindergarden (the less you earn the less you pay, but there is not enough spots), schools since 3 (free for everybody), good public health centers if you want (PMI).

Also prenatal care is free (you don't pay thousands of euros to have a baby.)

That result in good numbers for a western country: in comparison with Germany for example, women tend to have more children (2.3) and have them younger with less impact on their career and revenue.

>in comparison with Germany for example, women tend to have more children (2.3) and have them younger with less impact on their career and revenue.

Indeed. Interestingly the differences between western and eastern states of Germany are huge. Childcare and prenatal care are in general much better in the region of former East Germany. Currently we are short on nearly 300,000 places for children in childcare (Kindertagesstätten/Kitas) but only 30,000 of them are in eastern states. The mother's mean age at first birth in those states is younger (27 years vs. 30 years in West Germany). Now the problem is that unemployment rates are higher in eastern Germany.

Some numbers:

>MOTHER'S MEAN AGE AT FIRST BIRTH

>France 28.1 years (2010 est.)

>Germany 29.2 years (2012 est.)

I have 7 kids, my wife stays at home and homeschools them. We live frugally. Outside of enormous COL areas like San Fran, NYC, LA, etc. it can absolutely be done.

The first couple kids are the most expensive, by the way. And thrift stores are my best friends.

Very broadly speaking (UK, Sweden at least since I live(d) there and know the rules); more kids = more income if you're living on income support.

So you have linearly increasing support depending on the number of people who depend on you.

There is no such linearity in work- you get paid and you pay whatever you need to pay, the company and the state do not make things easier.

I'm not saying that if you have kids on welfare you're better off- I'm saying that it's an easier cross to bear when you may not be as significantly worse off as you would be if you had a flat income.

If it makes you feel any better I was raised on welfare in the UK and am not insinuating anything negative. This is the reality of living on income support- if it is _not_ then please provide evidence instead of hitting the disagree button needlessly.

Not just in America. I don't have any saving at all, and a lot of people around me neither, and I'm in France.

Now theoretically, we all pay regularly to the state for that. But in practice, none of us believe we will see the color of it when we grow old.

Last week a dear and poor friend of us said she wanted to go to school again, but that the one she wanted in cost 5000€/year and she didn't have the money.

We secretly discussed to create a common money pot to pay the tuition for her. I suggested that we all put 500 € each and solve the problem.

All the participants were all above 30, none of them had children, all of them were working. Half of them don't even own a car, as in my city it's a useless expense. Yet it was a rude awakening: most of the people at the table could not afford such an amount. Even once in their life for a very old friend.

So we discussed a bit, and it turns out most of us don't have any saving and just live by the day. Comfortably, granted. They are not poor, they eat well, they have clothes and can afford pleasures. But if anything happen to any of us, we are screwed. We have no buffer of any kind.

The cost of life is, of course, part of the cause of this. But also the fact that our lives are very instable : breakups, job changes, moving in/out, make it hard to save. It's also a cultural problem: enjoying ourself have been more important that savings.

But there is also another issue: individualism. The thing is, most of us could probably find 500 € to give away. But the solidarity is not strong enough for this effort.

So if friends won't get out of their way to do that, I have little hope that society will solve the retirement puzzle. People care about _their_ retirement, not about everybody's retirement, not how society will find a balance or how their neighbor is going to survive.

> So we discussed a bit, and it turns out most of us don't have any saving and just live by the day. Comfortably, granted. They are not poor, they eat well, they have clothes and can afford pleasures. But if anything happen to any of us, we are screwed. We have no buffer of any kind.

The solution to this largely a matter of a shift in attitude. Start saving 10% of your salary right now and stop buying new clothes, eating out etc. Having a buffer is way more important. There are plenty of resources for learning how to live frugally. The benefits of having a cushion, however small, are enormous.

Of course, that doesn't take away from the other points you mention. But it's by no means an unsolvable problem for the average comfortably-living individual.

Attempting to actually have a life outside of the work, eat, sleep cycle and save money is difficult, though. Reading the experiences of "frugal" people suggests that they often barely do anything that isn't absolutely required to survive and hold down a job - this must surely be incredibly bad for their mental health from my perspective, but perhaps some people can live like that.

The actual trick is probably to make most of your savings in other places - a smaller house/apartment with less "stuff" to fill it might feel just as good, ensure that you always have some form of pre-cooked food in the house to avoid the temptation of takeout for no reason other than having no energy to cook, figure out whether you can spend less on transport (do you really need the big new car for the one time a year you go on vacation, or could you rent a vehicle or take the Greyhound/Megabus/etc for that weekend?), figure out whether you actually need the latest flagship phone and an unlimited data plan (maybe consuming netflix, youtube, and spotify on the mobile network isn't such a great idea?). These are big-ticket items and it's almost always possible to save significantly on them without changing your lifestyle if you're "comfortably living".

The general point is that when you were 22 and earnt bugger all you could still live, now you're 32 and earn a lot more, you live a lot better but never started saving.

You should be saving money but you're not. So force yourself to revert some of your positive life-style changes as you actually can't afford them yet. Do it at source, set up a standing order to automatically take the money out just after pay day.

Start small, say 1%, and increase it every 3 months maybe?

To be honest, the first statement you get of your savings where you earn interest instead of paying it is quite refreshing. And you feel a little smug and a little more mind-at-rest because you know you can deal with disasters.

I agree, hence the "It's also a cultural problem".

There is also the fact that we know the French health care system, the social aids you get if you loose your job, and your family will all come into play for some category of problems.

And there is the gamble for more comfort vs responsibility. My generation really don't want to take any kind of responsibility for anything, including society, the planet and their own life.

But even if you consider that:

- saving 10% of my income will not, in any way, let me live through my retirements. Not at half of my current life style anyway. And I do earn more money that most people.

- those are people in a very comfortable situation. Now take people with children, a loan and a standard job, and you have a much less simple picture.

- most people have been told the story that the retirement system will work, or that we will make it work. Beside, they don't thing 30 years ahead for anything.

- a lot of people won't make rational choices in their life. Taking a loan they should not, making a child they can't afford, getting married with the wrong person... Expecting people to save is already at another level of planning. We failed at educating people, but we also told them it was ok to do what they were doing.

- we have a huge value scale issue here. frugality, quality, solidarity... Those are not the thing that society promotes. Solving the retirement problem is not just an economical issue. When banks are bailed out, medias scream "money and consumption" and Trump rules the most powerful country in the world, convincing somebody to not go for take out is quite hard.

- fixing and cookie are getting a lost art.

- things do cost way more. 10% is a lot for some people.

If you can manage to save enough to live on for 6 months at your present level of expenditure you have some kind of insurance against the idiocies of life and employers.

Although I find it very peculiar that my parents could live the life my friend live, but afford children, have saving and yet now have a retirement.

A 30 years old single person with no children an a job that doesn't have a loan or crazy spending habits should not have to choose between savings and pleasures.

Yup the biggest social change in my generation (I'm 60 soon) was women going out to work. Mysteriously, having two wage earners per family has not actually increased apparent wealth. In fact it has decreased.

In UK housing has become much more expensive as a proportion of earnings, and wage rates seem to have declined in real terms.

> saving 10% of my income will not, in any way, let me live through my retirements. Not at half of my current life style anyway. And I do earn more money that most people.

sounds like you need to learn to live more frugal, then.

learning to not consume blindly but instead responsibly is just as important as saving money.

Although I'm not living the grand life. I don't own a car, I don't have children or crazy expensive hobbies. I cook every day, buy vegetables at the farmer market. I don't drink at all, or consume drugs, or smoke. I don't go out a lot. Once a week maybe.

Beside I find it very peculiar that my parents could live the life my friends live, yet could afford children, have saving and now have a retirement.

A 30 years old single person with no children an a job that doesn't have a loan or mad spending habits should not have to choose between savings and pleasures.

But yes, I don't deny I could definitely tune down my spending.

I'm not in a difficult situation myself. I don't have saving, but I have a nice life. I'm one of the person who can give away the 500 €. I'm more concerned that so many people around me can't.

While there is definitely an attitude issue here, it can't be the only one. I can believe there is a difference in the education my parents had. I can't, however, they were so much better planners than my friends are.

Please note that salaries are horribly depressed in France - in areas like Paris, the cost of living is comparable to places like San Francisco at easily 1/3 of the salary.

The price are not in the same league as SF, let's not exaggerate. But yeah, the salaries are low compared to the US. I had several proposal to make 5 times what I currently make.

However, money is not everything. Living is France is very sweet, and the US lifetyle is peculiar. Also, I'm currently an independent dev, and the salary implied I signed a 5 years contract. That's a lot of constraints for me.

But yeah, compared to the US, dev are not well valued here. And you should see in Spain...

> Beside I find it very peculiar that my parents could live the life my friends live, yet could afford children, have saving and now have a retirement.

I understand you know that yourself, but the past is the past - my grand parents were suffering through wars.

Sure, and it's good to be realistic, and take responsibility for your life.

But it would be unfair to blame entirely the current generation for their situation. I don't think another one would have ended up in such an entire different situation. Life does cost more. Society does push to consume.

I think it's just that given that the economy is probably going to be shittier and shittier, we should take the opportunity of our current still nice lives to prepare.

Well, what you are expressing is actually something particularly typical for this generation - which is demanding something of your fate.

The truth is - you are born - now play the cards you are dealt. If you complain about the cards - then you are already about to lose before the game even started. Maybe next card dealt to you is Leukemia - now you will complain to yourself "why me of all the people - what have I done to deserve this?" while you wish your only problems still were being in a financially worse position than your parents. I think that's what you are doing.

Congratulations, but that rate of savings is not even close to achievable by the vast, vast majority of workers in the world. Looking around my peers, it's hard to imagine that more than a handful can manage to even save 10%.

I can second this, I started putting just €100/month away and was pleasantly surprised to see it tick over into the €1000 mark very quickly. It's a standing-order at my bank, triggered when any large deposit is made (e.g it fires when my salary is paid).

Now that I reached a milestone (even if I did kill the account from 300->0, 250->0 a couple of times in emergencies) I intend to increase how much I put in there. 10% of my salary is a lot to do without, my wife doesn't work, we have two kids and a mortgage and a (useless expensive) car. But the €100 I simply didn't miss, and the €200, that will get me to the next milestone, when I'll jump to €300, and so on and so on will all soon arrive.

Yes. I looked at diverse investments but I'm still looking at losing at least 30% of value compared to inflation.

I have opted out of the mandatory pensions as I had debt to pay off and it makes more sense to invest in that. I'm not happy with the risk profiles of the investments they offer as well as even the low risk one has a shit return.

I'm looking for something different. TBH I'm making a reliable £300/month clear profit for a few hours effort on ebay buying and selling crap which over time has a better investment return sticking it in a low interest account that sticking a portion of salary in high interest.

That's working for now but I want something that requires less effort :)

It's not that difficult to keep pace with inflation and beyond over the long term. I'm not going to give financial advice here but if you look there is tons of useful information out there. You will need to educate yourself though, in particular, learn the common mistakes.

"Losing to inflation" is relative. If inflation is 2%, your goal is to find a strategy that yields higher than 2% after taxes and expenses at a risk tolerable to you.

Your eBay endeavors are basically allocating your capital to a closely held business, which is perfectly reasonable though like you said, likely unscalable.

Yes scalability is the problem. I'm expecting a shortfall within a couple of years so I need a new strategy. Currently this is running way above inflation which is good but the hill I'm pedaling up is getting steeper.

While I enjoy the odd banter about "what's the best investment planning strategy" — quite frankly, people seem to completely disregard/misjudge the impact of what being persistent and consistent in putting money away for later, vs. trying to find the best interest rates is. Sure, there's all sorts of deflation and opportunity cost eating up some of that money, but the single-most crucial threat to it is yourself. You will eventually rob that account, either for a car, or some other sort of luxury. I don't judge, a good vacation may do more to your health right now than a few hundred dollars down the road. I do have an MBA (also 20-years of SW dev, please don't rip me apart), and due to it, people seem to enjoy asking about investment strategies and saving for retirement. We go into various things, and then the conversation drifts off and we're talking about the next iteration of the Apple Watch and whether or not the person should upgrade. And I get it, it's part of the lifestyle, it's part of enjoying life, but don't come at me with interest-rate optimisation discussions when, clearly, you're sabotaging your own interests here, quite literally.

This is not the response you wanted, and I feel terribly sorry for it, but it's something that keeps creeping up when inflation/investment discussions flame up. So, to help, and this is just my very personal suggestion: grab a reasonable amount of your "savings", enough to make an impact (>$5k), but not enough to ruin you (<$100k). Put that into a low-fee stock-trading account (Robinhood, Fidelity, etc.) — wait for one of the very, very big ones (NOT Snapchat), like Amazon, or Apple, or Microsoft to dip a bit below the average going rate for the past few weeks/months. Like Amazon, it's been hovering around $1000 for a bit if I remember correctly, now it dipped below it and everyone wants/expects to see this go over again. Find an opportunity that will net you 3-5%. Amazon was at $955 yesterday, if you expect it to go up to $1000, that's 4.7% of gain (ignoring small fees). So, like many, you'd buy a good chunk of that. Once the order is through, you set two more orders, one for $670 (that's your panic sell), and one for $1000. Then you wait.

This either takes a few days, it may take a year. It doesn't matter, if you end up with 4-5%, you take out your original investment, and you leave in whatever dollar amount you just gained. Rinse, repeat.

There will be lots of people advising you against this, and that's absolutely correct. If there was a simple system to follow to guarantee you to make all that sweet sweet money, then, by definition of the market, there would be no such system any longer. That said, this strategy has served me (personally) very well over the past 10 years, and I've made much, much more than 5% over the years. The "magic" of it is that you can get out tomorrow, or you get out in five years. If you don't need the money to live, then you are not in a hurry. This allows you to wait until the time is right.

The single-biggest enemy here, again, is our own greed. I usually aim to net a meagre $200-$700 before I sell. Even if the stock keeps rising like crazy, I normally get out after $400-$500, and rarely let it sit any longer. It's one of my rules (and others may think this is stupid, which is just as valid as me having that rule).

And I speak from experience:

I've once had a tough year, after several years of just making easy money on an ever-rising market. So, I invested all I had into Netflix. It was a 'jumpy' stock, but I figured if I time it out right, I'll end up with way, waaay more than my regular 3-5%. I could possibly make a decade of progress in my otherwise tame (but perfectly steady) stock investments. Then, Netflix dipped 40% or so, and it stayed there for quite a while (days, weeks, months...) — and I didn't have a panic-sell in place then. To make it worse, I even doubled-down as any panicked idiot would do, and Netflix dipped further. I didn't log in to my stock account for well over a year, if not almost two years I think. Then, one day, it had made its way back to the original price. I got out without losses, promised myself to never break my own rules again, and continued without a hitch after that. But, holy moly, had I needed that money, I'd not have been in a good place.

At this point, someone would usually say, the smart thing is to diversify, to spread the risk. But to me, spreading the risk is like watering things down, you're also watering down the profits. I'd rather know a lot about one stock, at most two stocks (I never do more than two), and watch them carefully, vs. having 15 stocks in my portfolio, where I barely keep up with the basics. Again, that's just me, everyone is different. Also, having small investments in many stocks (vs. one or two stocks) may drive up fees quite a bit, depending on how fast you (have to) move.

If you don't want to risk this, then funds and or an index, or a work-place matching investments type-of-plan may be best. It's other people doing the same thing for you, and you pay them a fee, regardless of performance. Which never felt right to me (I still advise to do this if you don't care about stocks or actually taking care of the money).

I still firmly believe that someone who continues to save hard, and keep that money far away from your 'usual spending money' will almost always beat someone trying to optimise their investment strategies.

Oh, lastly, you obviously have to pay tax on short-term gains. So this will come into effect as well. Depending on your location/tax-jurisdiction, this will be handled differently and it may make sense to optimise based on that (>1 year investments).

Thanks for your input. This is the sort of response I want which is a well rounded one. I want to hear about the failures as much as the successes ;)

For reference, I am plugging a fair amount of cash into a savings account when I come across it and avoiding unnecessary luxuries. That in itself has netted me a fair amount of cash and flexibility. Not spending it is better than saving it.

I'll read further into the investment side of things. I really want to get 50% of my cash reserve into something with a better return at the moment.

Currently I am taking 1-5% of that and netting £300/month profit which totals about a 11% a year rate but the effort is quite large for this.

I don't know if a shift in attitude would help, at least not in aggregate. It might work for one person, but if everyone did it, then it could end up being a wash or we could see other weirdness..

If everybody started saving 10% of their salary, the decrease in consumer spending would put deflationary pressure on the economy. That could, in turn, lead to a few different possible scenarios depending on the economic policy decisions of the government and the central bank:

1. If the economic authorities refused to respond and decided to "let nature take its course" on the economy, the reduction in consumer spending would lead to businesses shuttering and people losing their jobs. Maybe instead of 1/3 of people not saving any of their salary, 1/3 of people just wouldn't have salaries in the first place.

2. The central bank can lower interest rates thereby making it easier for people to borrow. This easy borrowing would provide an incentive for people to spend. This could counteract the effects of whatever was incentivizing them to save in the first place. Or maybe we'll end up in a situation where people think they're saving, borrowing, and spending all at the same time and what's really happening is that they're "investing" in some kind of asset bubble that they don't know is a bubble.

3. The fiscal authority borrows and spends money into the economy to make up for the drop in consumer spending (and, if distributed well, that money circulates and boosts consumers pending too). This fiscal expansion route is kind of the opposite of the monetary expansion route in scenario #2. Here, the government is going into debt in a stable and controlled manner. With the central bank lowering interest rates (#2 above), you're encouraging the expansion of private debt, which is unstable and can collapse.

I don't make economic policy, but if I did, I'd tend to lean toward option #3. Of course, it entails the central bank and the country's government working together to make it happen. The ECB would have to encourage (or at least allow) the EU member nations to go further into debt. In the case of America, the Fed doesn't have that kind of control over the government. If Congress decided to take on massive government debt and spend new money into the economy, the Fed would have no choice but to take the necessary actions to keep prices stable (raise interest rates, etc).

Well, that turned into a little rant about things I care about. I guess my overall point is that if Everyone started saving 10% of their salary, it would be a huge shock to the economy, and probably not a good one. And what happens next would depend on a lot of things that I think about a lot.

Anyway, solving this "problem" is not just about a shift in attitude toward saving. At least not in the general sense. I do agree with you that it's not an unsolvable problem for an average comfortably-living individual.

I'd give 500€ away to someone. I have done before on numerous occasions. The problem is not solidarity, it is trust and the human condition. If I give that money to someone, it'll turn into an iPhone or be smoked before something productive is done with it even if it is mandated for education or essentials to get someone out of a hole they are in. People are stupid and irresponsible.

Your situation is extremely scary but not uncommon. Please see a financial adviser as soon as you can, it can make a world of difference (disclaimer, I am a financial adviser). If you can't, I humbly suggest:

1. Save up a 1000 € in an 'Extreme Emergency Fund' LIKE YOUR LIFE DEPENDED ON IT

2. Work out exactly where each euro goes each month and start cutting down your unnecessary expenses and keep to a strict budget

3. Pay off all debts (except your home mortgage) LIKE YOUR LIFE DEPENDED ON IT using the money you would have frivolously spent

4. Fully fund a 'Proper Emergency Fund' to the value of between 3 to 6 months worth of expenses (depending on how much sick pay/unemployment insurance you have from your employer/country)

5: Invest at least 15% of your household income into retirement

6: Start paying off your home mortgage early

7: Use the excess money to build wealth

Do not skip over a step. If you need help let me know.

I would not make it extremely scary. As you said, we know enough causes, consequences and solution to act. It's just interesting to have a picture of what's going on.

The thing is, most of the things you describe, I already do, in France, through taxes for health care, social aid and retirements. Then also insurances (for cars, flat, etc). Doing it myself would mean paying twice.

And since education is free and I don't have a car, I don't have a mortgage.

So my situation is not that bad. It can become bad if:

- the system fails. It will for retirements. It does for some health care / insurance / social aid situation.

- your issue arise outside of what the system takes in consideration.

Knowing that, setting up an automatic emergency saving wire is a good thing to do.

I don't believe saving for my retirement will help in anyway. I'll have to find something better, which I'm working on.

But again, remember than most people don't read HN or anything else than FB streams. They live their life as-is. Like my parents did.

The question is, why could they afford children, pleasures, and saving, while my friend can't. Neither my parents nor my friends are very good planners, but clearly their situation is vastly different.

To address your comment about the situation not being scary... I think it would feel very scary to find yourself in a situation where you don't have an emergency fund. No one ever thinks that they will be hit with an emergency situation but I've found that 8/10 people within a 10 year period will be hit with an unexpected event where they need to use emergency funds (disclaimer: this is based on anecdotal evidence as observed over my life).

If you or your friends couldn't spare 500 € to help a friend out I really wonder what savings you or your friends have.

The most powerful tool anyone has to build wealth (and help others) is:

* The discipline to live below your means (and avoid debt), and

* Your income.

If you are unencumbered with debt, and live as far below your means as you feel comfortable with, you can build a substantial amount of wealth if you have enough time.

As to affording children, and I can only speak from personal experience, but I've found that a dedicated parent will always find a way.

You're right that previous generations had things differently, but only with regards to globalisation... current economic disparity started to occur post 23 December 1913 with the Federal Reserve Act and post 15 August 1971 when Nixon unilaterally terminated the convertibility of the US dollar to gold.

If you really want to know why you will need to learn how money is created and the economic ramifications of a fiat currency (and inflation) combined with a fractional reserve system.

This is a great list, but most will never get through all the way to #7. People have major fixed costs that they simply cannot cut out. Hell, I struggle to get past #4, and I've cut expenses to the bone. Yes, I could drop my mobile phone and Internet. I can move 3 hours away from work (I'm currently 2 hours away) to save on housing costs. I can stop going out with friends once a week and live life as a hermit. I can collect rainwater to drink. Maybe after all that I can get up to #5. But at what point are you sacrificing your certain life today for a possible future life?

Thanks for your great question. I'm not sure how much you'll like my answer though.

I think you can, if you think you can, and can't, if you think you can't.

In other words, it's a matter of belief, action, and continuing motivation.

Of course I don't know your exact circumstances but controlling your expenses is only part of the equation. If you've trimmed your expenses down to the bone it's now time to focus on increasing your income while maintaining low expenditure. Most people don't do this and their spending grows faster than their income does. The mentality you want to avoid is "Get a raise? Buy a bigger/better (x)!"

So until you control your income with the discipline of a general controlling an army during war, the amount of money you make is irrelevant. A great example is sports personalities or entertainers that end up broke.

Assuming you've got that discipline, a sure fire money making scheme is a second job but this is where you can get creative... such as going around your neighbourhood and washing windows/cars/lawn mowing. The internet has flipped this idea on its head so you could freelance late at night after you've tucked the children in bed.

Whatever you do make sure it is bringing in cash right now and not some risky or highly speculative idea.

Imho you've got to earn the right to speculate and you can make sound decisions under high levels of risk when you know you got a properly funded emergency fund and pension.

But yeah, there was a reason why I emphasized LIKE YOUR LIFE DEPENDED ON IT. If your life depended on you getting 1000 Euros in one week you would come up with the money. If your life depended on you getting 6 months worth of expenses you would come up with the money. If your life depended on putting 15% of your income each month into your pension you would do it... you get the picture.

The sad thing is peoples' lives do depend on this stuff but they don't act like it does.

>>enjoying ourself have been more important that savings.

This is the main thing. People seem to always have money for gadgets, eating out, vacations and garden variety never-to-return expenditure. Yet savings are always dwindling and in many cases most people are in debt.

Marketing has done a good job of convincing people to spend money in the present. Even the money they don't have.

>>People care about _their_ retirement, not about everybody's retirement, not how society will find a balance or how their neighbor is going to survive.

There have to be consequence for bad habits. Free money hasn't done well to anybody around.

Also expecting some one hardworking to part their savings to pay for somebody who has partied all life is not just unfair, its theft.

Put that way, the recent dogma of spending on experiences, not things is a great trope. You can literally never have too many experiences and the consumption shall be limitless.

Some colleagues I have, take 10 vacation trips an year. Apparently its all about spending time chasing some hobby like photography. Apart from the fact that they spend insane money on camera and lens gear, you also have to spend money to travel, accommodation, food etc.

The funniest thing is most people don't use some lenses more than a couple of times. And they don't even see their photographs more than once. What's more, no other human will ever see their work.

All of this is fine and dandy during a phase when you are young, have energy and a job that pays well. All this money could go into a retirement fund. Someday its all going to end, and these people will blame government and societies for not doing enough about the 'free money' they think they are entitled too.

> It's also a cultural problem: enjoying ourself have been more important that savings.

It looks like the reason you have 0 saving is because you... simply refuse to save money and spend it all on leisure instead? (after necessities are met).

> But there is also another issue: individualism. The thing is, most of us could probably find 500 € to give away. But the solidarity is not strong enough for this effort.

What do you mean by individualism? That one should value individual rights such as freedom of speech, respect of individual property etc? Sounds to me like many freedoms are going away in France and civil liberties are always at risk. On the other hand, collective rights keep expending and these are extremely costly. When it comes to coerced solidarity, France sure is one of the world's champion. It seems to me that the reason you and your friends refuse to give to your friend is not because of too much individualism but because of too much collectivism, you are already paying so much in tax to support these solidarity policies that you are left with little money for your own leisure, let alone for your friends and you feel like you've already paid "your fair share" by outsourcing charity and solidarity to the State. But of course, as usual all problems in France are blamed on individualism and capitalism instead of the elephant in the room: the unfettered collectivism going on.

> simply refuse to save money and spend it all on leisure instead

Yes, I clearly said it's part of the problem. Now "all" is exaggerated, as it's I don't see my friends living a wasteful life. They do get out a little, but no more than my parents did.

> What do you mean by individualism?

I mean that everybody is cool to do fun things together, but grouping efforts to help one-another does not come easily.

As for the rest, it's a very different debate I'm not in the mood to have.

> Not just in America. I don't have any saving at all, and a lot of people around me neither, and I'm in France.

The situation is fundamentally different though.

Unlike what happens in America, in France you are already paying the pensions of currently retired people. Which means you aren't supposed to save yourself, as future workers will (in theory) pay for your pension once you retire.

In practice, we know that it might not happen this way, which is why you might want to have savings, of course. But the current system means saving for your own retirement ends up representing twice what an American would need to save, since you have to 1. fund current pensioners 2. fund your own future pension. Americans only have to take point 2 into account.

In theory, according to the French system's design, not having any retirement savings is completely fine and is even the intended situation. Transitioning from our general contribution system to a personal savings system might be good in our period of stagnating population growth, but the transition itself is hard precisely because it means one generation will have to both contribute for others and save for itself. And it looks like it might be going to be ours. But it's a very different situation from what happens in the US where people just can't save, but they have no other way of getting a pension anyway.

Unlike what happens in America, in France you are already paying the pensions of currently retired people.

Actually, that's exactly how Social Security works in the US. You and your employer collectively pay 12.4% on your first ~$130k of salary, which goes to support all the current recipients of Social Security.

I think it just depends if you are okay with what the social security benefits pay out. Currently if you retire it is $2,687 a month. This is the max though. Most may get less.

> But also the fact that our lives are very instable : breakups, job changes, moving in/out, make it hard to save.

It's not hard to save because of those reasons (for people in the situation your describe). Like, at all.

It's like people living paycheck to paycheck. Unless you're already so poor you're eating noodles and free store samples for nurishment, you can do this for just a while, and save enough to have one month's salary in the bank. (though probably you specifically don't need to be as drastic as this)

One month's salary in the bank means that when the car breaks (though you don't have one), or when you get fired, or have to move, you can have the means to "just fix the problem". And often being able to pay to fix the problem makes it much cheaper to fix the problem, in a virtuous cycle.

But you can't spend that on a vacation.

Yes I agree it's a cultural and educational issue in the end. This should be taught in schools.

I think it also hurts that in the US it's common to be paid weekly, or fortnightly. That means people never have even a full month's worth of rent and groceries, and they therefore never learn how to even informally have a budget. And you get things like people being able to afford eating out right after being paid, but not right before (which makes no logical sense).

But you know this, so why don't you do this already? You can save, you understand that it would be in your best interests, and you know how. So why don't you?

Essentially, I dont because i used to live with a lot less and now i like my life the way it is, so i gamgle comfort againts security. A lot of peoe have valid reasons for not saving. I don't have excuses, i take a risk in echange for a life style.

But you only need to save up that buffer once, then you can be in the same lifestyle again, with a higher likelihood of remaining in that lifestyle since you won't have to get a payday loan (and continue in a downward spiral) when something terrible happens.

This won't mean much coming from an Internet stranger, but your reply really makes me be disappointed in you.

Me neither, and I'm Italian. I'll also add that minimum age for retirement is being pushed farther and farther (I probably won't be able to retire until I'm 67 or something like that).

Maybe you shouldn't save for a retirement then. Maybe no-one should.

I think about this quite a bit. I'm quite frugal in my personal life (although certainly I could be more so), so I actively save for the future as a matter of course.

I'm also aware of the statistics around personal debt levels and net assets in the public at large and while it's clear there's a rude awakening to be had, I'm less and less convinced over time that the "awakening" is going to be of those who have no savings in place when they need them.

It seems pretty apparent to me that if the majority of people have no assets in a couple of years/decades (regardless of why that might be) and wealth inequality peaks to such extremes, then it's very likely the first political candidate to offer hard socialism (debt-driven basic income guarantee coupled with ultra taxation of higher net worth individuals) will sweep in an election, and the money problem will correct itself at an individual level.

Of course this isn't a solution to the living-beyond-your-means problem, and causes it's own problems (inflate the currency with QE, capital flight of high net worth individuals to friendlier jurisdictions), but I don't think that will matter in this scenario.

If the nature of people now is to be relatively short-sighted with regards to money, then what reason is there to expect that people in general are going to be any different in the future?

I fully expect it will be people who are saving their income that will pay to fund those who are not in the future if the latter is the majority.

>I fully expect it will be people who are saving their income that will pay to fund those who are not in the future if the latter is the majority.

Absolutely. I expect the government to renege on most tax-advantaged programs for retirement they instituted in the 1960s and on (Roth IRA etc). I expect Social Security to stop being paid to higher net-worth individuals or for them to be pushed into a later age where they can collect it.

The crisis we face isn't one that is going to be fixed easily. Government receipt shortfalls project to be massive in a few decades.

>>it's very likely the first political candidate to offer hard socialism (debt-driven basic income guarantee coupled with ultra taxation of higher net worth individuals) will sweep in an election, and the money problem will correct itself at an individual level.

As someone who has had experience living in that system let me tell you the moment something like that can even happen. Most rich people from whom you could take significant for your socialist schemes will leave the country. Leaving behind a very very small part of usable money for your schemes. It will be over before it begins.

You have also now scared away almost every single economic prime mover individual from the economy to a point almost any body smart will only have one option for a good future- To leave the country and immigrate to else where. And there will always be some capitalist heaven which will welcome all this smart people with open arms.

With this set up your common pool of money from which you wished to pay for your Basic income will shrink year after year, until bankruptcy and total investor loss stares you in the face.

>>I fully expect it will be people who are saving their income that will pay to fund those who are not in the future if the latter is the majority.

They won't(rightly so) and that is what will be the biggest problem in the times to come.

The only way in the future is to make good decisions for the future or suffer.

This is assuming they haven't found a tax haven where they already park their money.

These days no one stores money beneath their mattress. Most money is in global businesses. So exit tax strategy is already a failure. Capital exodus today is called 'foreign direct investments'.

Besides you still are left with a problem with losing a lot of bright young people every single year without whom and taxes from their ventures you won't have anything to run your schemes on.

The global business holdings are typically held in US accounts. Transactions from there are 100% traceable.

Overseas accounts in HK and Switzerland are being cracked down hard. (I mean if you want to break the law, you can always break the law...)

It's not that easy to move funds into tax haven without some risk (ex: whether your GRAT will actually pan out) or advance tax event. (The easiest way is to start businesses in a tax haven in the first place, which is different from moving capital once it has been created).

Great point about human capital. I would leave for Canada or Singapore under such a regime as well!

You can't stop people from leaving. Look at USSR, India or any other ex-socialist economy. Unless you turn your country into a kind of North Korea, these things can't be stopped. And even if you did turn your country into North Korea, the rich will likely be in the top party positions and do whatever is best for them.

Every other socialist economy has had this thing in the past to make it hard for people to leave. They don't work because you can't make people stay against their will.

Most countries have now learned this the hard way. On the longer time period you can only encourage people to do good work, you can't punish them into doing it.

Ah ok I think I get what you're saying better now. Once people decide they're leaving and never coming back, whatever rules you have in place are worthless since they're going to ignore your exit taxes or whatever since they're not coming back and they think your regime is illegitimate anyways.

A few years ago I learned about the FIRE-community. Financial Independence, Retire Early. I'm more in the FI part, saving a big portion of my income. By living on roughly half my income, I save up for a "year of not working" each year. This gives me a lot of freedom and ease of mind.

Do plans like this ever take family and children into account though. As a single person it's all very well saving half your income if you are reasonably well paid. But if you have children I just don't think that's practical.

I saved a fair bit before kids. Then me and my partner made the decision that we wanted one of us at home to bring up the kids, and not have them raised by daycare workers. So now we have one income, and more expenses than before. I'm reasonably well paid, drive older small cars, don't have any particularly expensive hobbies or holidays. I still save, and contribute to a private pension, but the idea of saving 50% of my income is unachievable.

Now that's fine if you don't want kids, but I often think these lifestyle philosophies promote themselves as fantastic and obvious, and why doesn't everyone do it. But forget to balance them with the hidden sacrifices you have to make that they never seem to mention.

I want kids some day, and I know saving 50% at that time might lead to sacrifices I don't want to make. But until then, I would probably have had a professional career anywhere from 7-13 years. Those savings can then accumulate rents for a long time, even though I wont be able to contribute any new significant amounts.

I have 2 kids (5yo and 2yo) and right now no problem at following this plan (started when my first born was born). It can be done, you need to make sacrifices but the sooner you start the better you will be later on

Yes! I save roughly half. I don't plan to live on where I am right now in the future, so basically every month of working means 2-3 months of "not working" in a cheaper location.

People like to ask that question, as it gives them an easy out; "those guys probably live boring lifes".

I'd say I don't sacrifice much. I spent a month income on vacation this summer, went skiing in the alps this winter. I have hobbies I enjoy where I don't cheap out on gear or experiences.

I'm privileged to have an income that enables this. But still I'm baffled on how my peers with the same income use all their money. And I don't really see how they are able to spend most of their money, and how they benefit from it compared to me. For comparison, my salary is about $70K in Norway.

IF I'd felt I now sacrifices something of importance, it still would be worth it. I can take years off and do what I want, switch to a lower paying job with higher QoL etc, retire early or other things, while those not making the same "sacrifices" will have to work.

Know a Googler who makes $350k/yr. Lives in San Jose, CA and no kids. Says he can't figure out how to save because his "modest" expenses are too high; thus, he needs a higher salary. Borderline absurdity.

Getting a new car every 3-4 years is extremly expensive. A lot of people think they can't live with an old beater, that they absolutely must have a "new-ish" car. An old beater for those people is a 5 year old car. An old beater for me is an 15-20 year old car.

"Warren Buffett lives in a modest house that's worth 0.001% of his total wealth".

An old beater car can be a huge inconvenience though. My 16-year old (when bought) Saxo had to have bearings replaced, but the bolts for the suspension arm were so rusted they snapped during the process and cost me 1/2 the price of the car to get a new arm and bolts, too. Replaced that car with a 15-year old Astra for a little more oomph (1.6L over 1.1L) which recently had it's handbrake rust onto the disc. A few whacks with a hammer fixed that, but I couldn't use it until after the place I wanted to go was closed because I needed my girlfriend to be able to hit the foot brake when I hit the handbrake off.

Both cars required a replacement battery within a year of buying, as well as new stereo wires for the Saxo which I had to acquire from a Peugeot 106 in a scrapyard and various bulbs for the Astra. These problems are less about age but more about previous owners and myself.

I can't wait until I can afford a newer car, something closer to 5-10 years old instead of 15-20, because I won't be praying that my car will pull off every time I haven't used it for 3 days.

living frugal - meaning actively reflecting on expenses and consumption behavior - actually leads to realizing that life is not about acquiring status symbols to impress the wrong friends or a bigger TV. It's a very healthy virtue.

I do the same (actually I live on more like 40% of my take-home), and I don't feel as if I've sacrificed anything.

The amount I live on has slowly gone up since I started working. It's just that when I get a raise or promotion or new job, I don't spend the new cash flow, I save it.

A couple years from now I'll probably be living on 30% of my take-home, but the amount I spend every month will probably have gone up slightly.

The question you should be asking is how much do you sacrifice by not saving?

I could get fired tomorrow and my bills would still all be paid for years. When I retire it's going to be in a big house with kids and grandkids that have their college paid for. I can retire at 45 if I really want to. Knowing all that is incredibly comforting and peaceful.

Just the feeling is worth it. I used to spend my entire paycheck on bills and put the next month's spending on a credit card. My net worth was negative. That way sucks. This way is better.

People probably thought I had more money before because of all the useless flashy crap I bought. Fuck those people, I'm doing way better than all of them now and I know it.

I used to drive a really nice car thinking it made me seem important or something. Now I know only idiots are fooled by that trick, and to everyone else the car just made me look broke and stupid.

While I probably don't earn as much as OP, when I compare myself to my friends, I earn more than most and still spend less, living on about half my income too.

Main differences in lifestyle are I don't buy shit (I don't even shop online at all most of the time so no temptation, when I consider buying an item I ask myself "do i really need this" and most often find that I don't, I try to get most items from nearby businesses, I don't subscribe to stuff may it be paying services or even newsletters, hell I even found half of my furniture on the streets or second hand), I cook like 90% of my meals (takeaway is an extra 2-3 times per month average, I bring my food to work, I try to do as much as possible from scrap), I don't spend as much time/money in bars or other social activities as them, and I don't take trips across the globe (I am lucky enough to have enough family-owned places to spend my vacations at, I also avoid flying far for ecological reasons).

Pretty close to what I'm doing except the travelling/flying part, which is important to me. I don't even like "owning stuff" or subscriptions so I naturally only buy things I can't go without.

I live on ~30% of my income, which I would consider a modest "upper entry level developer" in my country.

I don't feel like I sacrifice anything, though it is true that I'm lucky to share an already cheap apartment with my SO. (But we also only have heating in two of our rooms, and not even a sink in the bathroom - we brush our teeth in the kitchen. I guess this would already be inacceptable for many...)

I don't own a car because I can bike or walk everywhere. I only use prepaid cards for my mobile phone, no data plan, because I always found the idea of paying for mobile internet ridiculous when there is wifi all around us.

(Plus, I don't like how being online all the times makes me check my phone so often.) I don't need a new shiny phone every two years and will use my Fairphone 2 until it dies on me.

I do eat out 3-4 times a week for lunch at work, but when at home I cook 99% of the time. Sometimes I eat out with friends, go to the cinema etc. I buy clothes maybe once or twice a year but avoid expensive brands like the plague, except for things like running shoes or other "long term equipment".

When it comes to my hobbies, I don't sacrifice anything, but I naturally like to do things that are inexpensive or for free like excercising and spending time outdoors, reading, watching movies...