The last go-round of this was with Celsius Network, which went bust a few months ago.

Celsius managed to create the impression that, funds deposited to them were somehow insured.[1] Now that Celsius is in bankruptcy, customers are finding out that they're not. Plus there were sketchy transactions, such as loans to affiliated parties. Which, of course, went bad.

The trouble with FTX is that they are a pretend bank and brokerage. They offer services that look like banking and brokerage, but the backup isn't there. They're not regulated as a bank or a broker, and they don't have the insurance of a bank or a broker.

From their site:

* "FTX US is a US licensed cryptocurrency exchange that welcomes American users."

* "The safe and easy way to get into crypto."

* "We are US based and regulated"

* "Don't be like Larry".

There is a concerted effort to create an illusion of legitimacy.

Even in their disclosures[2], you can see them trying to create the illusion that they're regulated as a financial institution. Their derivatives unit, FTX US Derivatives, does have some of the licenses of a commodity exchange. The main company, "West Realm Shire Services" (remember Magic, the Gathering Online Exchange?) just has money transmitter licenses. Not in NY or CA, interestingly. They don't have a banking license from a state. Or a New York State BitLicense. Or a brokerage license from the SEC.[3] Or an exchange license from the SEC. Or Security Investors Protection Corporation insurance. Or Financial Industry Regulatory Authority regulation.

> Their derivatives unit, FTX US Derivatives, does have some of the licenses of a commodity exchange.

This is because their derivatives unit was acquired, previously LedgerX, which I've used happily for 2 years. They're professionals, and not sketchy. It's really unfortunate that the antics and sketchiness of the parent might affect the perfectly legitimate and rule-following child company, and all of their customers like myself.

Wondering if I should close my positions, sigh.

edit: Wow, what a deceptive clickbait title! Should read "FDIC tells FTX US to delete a tweet".

> Wow, what a deceptive clickbait title! Should read "FDIC tells FTX US to delete a tweet".

(I've restructured this comment removing only a tangential illustration of shareholders liability, adding only to make my meaning clear from the beginning)

Prior to which you argue that the subsidiary is regulated as a commodities trading house. If so, CFTC is likely to promptly suspend them after digesting this FDIC enforcement action.

You appeal to the reputation implied of a known historical entity and or management and dismiss the enforcement action against the combined post acquisition entity as trivia. This is a circular conflagration as disingenuous as the offending misrepresentation of Federal guarantees. I'm suspicious of what connection you may have to this company and thinking your comments may be construed as flagrant obstruction the enforcement of Federal law through persistence with the estopped activities. If you are associated in any way but spoke independently, I think this one is really worth sitting out. For a start FDIC account protection is provided to individuals via FDIC insured banks and can't be parlayed by any broker. FDX referring to individual and or separate insured deposits I'm expecting to give rise to charges of interstate fraud at least. The targets of current enforcement are almost certainly intended to establish case law to enable sweeping enforcement and punishment I think I'm going to say is expected this time, through lower courts.

(Continues unchanged)

The usual resulting status of a any company acquired is "wholly controlled subsidiary" , and bar special classes of shares outstanding accounts and corporate governance arising from the parent holding majority voting rights prevails over any surviving minority shareholders or board member votes. It's theoretically possible for a acquirer to overlook the perfunctory resignation of the board and end up having to use company law and call for a EGM to vote on the termination of incumbent recalcitrant directors, but hardly likely anyone in the farthest reaches of M&A would have so little oversight of catastrophic professional liability.

In plain English there's no separation nor distinction between a subsidiary and its parent.

You could invent intricate arms length contrivances and claim independent operations, but unless each corporate entity has clearly independent capital structure, claims of independence are liable to be interpreted as fraudulent in English or judicial evaluation. Multinationals using offshore treasury vehicles use companies limited by guarantee and partnerships for avoidance of this category of responsibility.

The FDIC and other comments make it easier to see that the problem is widespread. Otherwise the FDIC wouldn't need so much boilerplate putting the onus on the respondent to deliver complete record of all misleading and unlawful communication.

Edited: replaced "guaranteed by share capital" with "limited by guarantee".

First, thanks for the thoughtfully written (though a bit hard to digest) reply, I wish I had seen it sooner!

Your exacting precision and care with words lies in stark contrast to my comment's lack thereof, is the mark of someone who knows what they're talking about, and is probably a lawyer with domain specific knowledge. :)

Though I doubt anyone will see this, to be clear, the vast majority of my "communicative intent" was to express:

* My explanation for WHY and HOW it came to be that the derivatives unit, FTX US Derivatives (aka LedgerX), has the proper licenses and is probably run with a different management philosophy than the parent. (that explanation being: "because they were acquired, not part of the original parent group of FTX people")

* My displeasure with what I think is a quite misleading and exaggerated "clickbait" title.

My feeling that it would be a sad state of affairs if the bad (and possibly illegal!) behavior of the parent company were to adversely affect the rule-following child and the rule-following customers was a minor point, though one I still stand by. I am curious if you agree that it wound be unfortunate?

Consumers gripe over unfortunate changes by and in management of their preferred vendors all the time, while being fully aware of the legal reality. :) I could have just as well been complaining about a great restaurant or coffee shop which was acquired. Either way, it was a minor point.

I'm aware that post-acquisition, even though it's not unusual for an acquired and independent business unit to continue operating just as they always had, in the eyes of the law any distinction between acquiring and acquired company is dissolved. As you correctly state "there's no separation nor distinction between a subsidiary and its parent". I know this, but that doesn't mean it's not "unfortunate".

> This is a circular conflagration as disingenuous as the offending misrepresentation...

No. You are incorrect. Nothing I said is disingenuous.

> I'm suspicious of what connection you may have to this company...

LIKEWISE!! :)

(I'm just a customer, though I'm flattered.)

And yes, you are correct that "FTX US Derivatives is a digital currency futures and options exchange and clearinghouse regulated by the US Commodity Futures Trading Commission (CFTC)".

Though I have yet to see any change in their operation -- CFTC has not "promptly suspended them" -- I do wonder if anything will happen.

This is how Coinbase wins in the crypto space. They are doing their best to do everything by the books. It's not flashy and exciting like FTX but they're playing the long game and intend to be around 20 years from now.

Could be. How FTX wins the crypto space is by bribing American politicians to get their way and do what they want. The founder has said he's gunna spend $1 billion on lobbying.

Doordash, Postmates and Uber have proven this works when their business was under fire through AB5 legislation they spent hundreds of millions on a state proposition to block it

> How FTX wins the crypto space is by bribing American politicians to get their way and do what they want. The founder has said he's gunna spend $1 billion on lobbying.

He's doing it. He's become a huge political contributor.

He's pushing something called the "Responsible Financial Innovation Act".[2] The proponents of this want to remove the SEC's authority over crypto things that look like securities, and be regulated by the Commodity Futures Trading Commission, which doesn't look that hard at offerings. From the bill text:

"Notwithstanding any other provision of law, if an issuer issues a security through an arrangement or scheme that constitutes an investment contract, ... and is in compliance with the periodic disclosure requirements under subsection (c), an ancillary asset provided directly or indirectly by the issuer shall be presumed ... to be a commodity"

So far, the bill hasn't gotten beyond introduction. There's considerable opposition. Since the massive collapse in crypto markets, and bankrupcies all over the place, it's less likely to go anywhere.

However, the political pressure has been successful in discouraging the SEC from bringing the hammer down on everything in crypto that looks like an unregistered security. They've been going after about two blatant scams a month. But the SEC hasn't been telling the entire industry, file an S-1 signed under penalty of perjury and get SEC approval, like every stock offering. (It's not that the paperwork is the problem. It's that lying on the paperwork is a felony.)

U.S. securities regulation uses something called the "Howey test" to determine if something is a security. (The name comes from a 1946 case where someone got creative and tried to securitize orange-picking rights in Florida.) The Howey test requires all four of the following:

1. Money is invested. ("Money" means anything of value here.)

2. There is an expected profit ("To the moon!")

3. The money investment is a common enterprise.

4. Profit comes from the third-party or promoter’s efforts.

Many crypto schemes have been devised to get around this. #1 was back around 2015-2017, when claims were made that crypto coins were not "money". That's been settled; they're assets for tax and regulatory purposes. #2, the "expected profit" thing usually isn't hard to prove.

Non-fungible tokens are an attempt to get around #3 by claiming that each NFT is its own collectable, so there is no common enterprise. But the marketing around NFTs ("floor price", "collections") tend to make that an iffy defense. Attempts to get around #4 involve turning control, or the illusion of it, over to a DAO, so the DAO, owned by the investors, takes the heat, while their subcontractor, the promoter, rakes in money. I don't think that one has been litigated yet.

Once you understand this, how crypto schemes are organized starts to make sense. The crypto industry lost on #1. #3 is the reason ICOs are dead and NFTs are in. #4 is the motivator behind DAOs.

> Doordash, Postmates and Uber have proven this works when their business was under fire through AB5 legislation they spent hundreds of millions on a state proposition to block it

As well as Apple, Google, Microsoft, Amazon, Facebook, Samsung, and the list goes on with their bribery in the US.

But thank you for confirming that the tech bros here are no different to the crypto bros also lobbying congress.

Most people and most drivers are against AB5 and it showed in the polling booth. It's a terrible piece of legislation that singlehanded caused the supply chain issues last year. They tried carving out industry after industry from the law because most people don't want to work the way AB5 is forcing, and it still broke things and things continue to be broken.

How did AB5, a law specific to California, cause a global supply chain shortage? Wouldn’t it be more reasonable to say that COVID was the ultimate cause?

If you’re referring to the LA and nearby ports being clogged, my understanding is that there was a massive rise in demand as restrictions (from COVID) were lifted, and they happened to coincide with the holiday season. Workers (and truckers), also at that time, realized they deserve better working conditions and decided to stop working, leading to an inability to move containers. That’s not AB5’s fault.

There are issues with AB5 as it pertains to owner-operators (people who own their truck and drive it).

Before AB5, a carrier company could hire an owner-operator to do some work without them being employees (eg. to handle excess work that their employees could not), but now they cannot, so those carriers are not sending any more business to owner-operators.

The options for owner-operators, who paid a large sum to acquire their truck, are to move out of California, become employees (owner-operators likely don't want that, hence them acquiring their own truck), or stop driving altogether.

Since California is a major port of entry for goods in the USA, having fewer truckers to move those goods leads to logistical issues.

I'm not coinbase nor FTX but if I would have already made billions I would consider myself a winner. I would say that all crypto companies that have survived with some kind of profitability for more than 3 years are clear winners.

>Celsius managed to create the impression that, funds deposited to them were somehow insured.[1]

Are they not? Sure, they're not FDIC insured, but it's pretty clear from the press release that the insurance is just the company itself promising to pay depositors if there are unexpected losses. Obviously if the losses exceed whatever has in the bank, the insurance won't be able to cover everything.

How do you accidentally make false statements about customer funds being FDIC- and SIPC-insured?

It's just not plausible to me that this wasn't an intentional attempt to mislead about some pretty darn fundamental properties of the investment scheme.

This is about their direct deposit product, which is offered through an FDIC-insured bank, Evolve Bank & Trust. (Same bank that holds accounts for other fintech startups, such as Mercury.)

It works as follows: When you sign up to enable direct deposit, FTX opens an account for you at Evolve. You can use that account number to have some or all of your paycheck direct-deposited. When you buy cryptocurrencies on FTX, that account is automatically debited. (This avoids the ACH transfer step if you were to purchase using your "regular" bank account.)

I may be missing something, but I'm pretty sure the deposited funds are FDIC insured, up until you use them for a purchase. But FTX isn't allowed to say that without mentioning the name of the actual bank (Evolve), and the FDIC thinks the "until you use them for a purchase" part of the preceding sentence is confusing.

I agree with the FDIC here, but I don't think FTX's statements were particularly nefarious. There's more nuance here than could fit into the tweet this C&D is about.

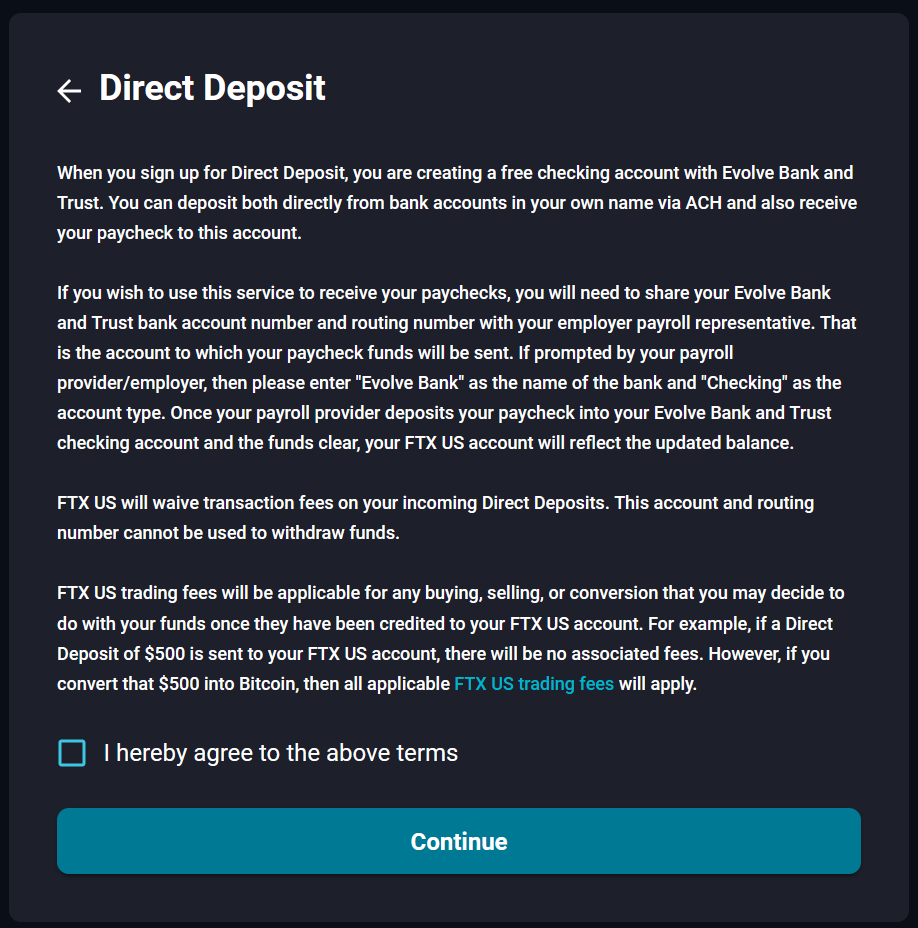

Edit to add: this is how FTX explains it when you enable this feature on their site (no mention of FDIC insurance, but if it's a regular checking account, the unspent funds in that account would be protected if either FTX or Evolve went bust): https://pifke.org/ftxdd.png

Yep, that's how I interpreted it to. The following things are still unclear to me:

- if you ACH push/pull funds from your other banks accounts into FTXus, are those funds held in that Evolve Bank checking account (therefore being FDIC insured)?

- if you deposit some crypto/stables and sell to USD, are those funds deposited into the Evolve Bank account?

- if you wire in USD (domestic and international) are those stored in the Evolve Bank?

They didn't - read the tweet, the statement they made is factual and boring. The tweet says they hold funds in FDIC insured banks and stocked in insured brokerages...how on earth is this misleading or controversial is beyond me.

This has popped up before with other crypto exchanges. The core piece is that the bank that the crypto exchange uses is FDIC insured but not the direct crypto exchange. So, if the bank that the exchange uses goes under, then yes that money should be insured. However, if the exchange itself goes under you SOL.

So technically this is accurate but very misleading. This is a complete nothing burger. They want Brett to remove a tweet (posted on his personal account by the way) and text on 3rd party sites FTX US does not control. Government regulation at its best.

> However, if the exchange itself goes under you SOL.

Either your deposits are federally protected from failure of the institution, or not.

It's as ridiculous as me telling my credit card issuers that their loans to me are federally protected because I have an FDIC bank account.

Nobody's worried about some bank going under, we're worried about the risk of trusting our money with a crypto exchange when so many have been Ponzi schemes.

Waving around the terms FDIC- and SIPC-insured in a way that implies that it means something to the end consumer is, IMHO, the sign of a scammer.

Fraud is never about anything other than false statements. Falsely telling people their money is insured (i.e. no possibility of loss, you can only win!) is a very bad thing.

Then we can all agree that the regulators are doing their jobs then.

Whether if it is the NTHSA investigating Tesla over its misleading claims and deceptive advertising of Fools Self Driving (FSD) and autopilot in the US to this matter of a crypto exchange misleading its customers via a tweet with the FDIC ordering them to remove the tweet, there are no exceptions to putting out vacuous and unchecked claims that involves safety in finance, or on the roads or anything that can cause financial or life changing implications.

This only shows that the regulators are doing their job and the system is working.

Per the letter, probably want to point out the cease and desist was due to "Potential Violations of Section 18(a)(14) of the Federal Deposit Insurance Act"

Also the conditions of the cease and desist also say they should make no additional dishonest statements regarding FDIC insurance, which is in no way restricted to tweets.

Does it even offer any realistic protection if the "partner bank" goes under? AFAIK the limit on FDIC insurance is $200k / account. Is FTX managing hundreds/thousands of account to get around this or is only $200k of their money FDIC insured?

To get FDIC insurance in a meaningful way it would have to be per-customer accounts created in specific ways.

If they're not created in particular ways the funds in the third party bank accounts can be taken in bankruptcy actions by creditors and aren't actually protected customer funds and aren't insured at all accept with whatever level of insurance they have for the partner bank going under, but that is not the risk anybody is worried about.

Good. Regulators have been dragging their feet with crypto businesses and them taking action means hopefully fewer people will be taking misrepresented risks.

Seems like a lot of tech companies have tried to ignore regulations.

Uber ignored taxi rules, AirBnB hotel rules, and many crypto companies have ignored banking rules. The difference is that the FDIC doesn't fuck around.

People seem to think that disruption requires the breaking of rules including legal ones. There's a difference from disruption from a new player by offering better service at cheaper prices than getting cheaper prices by breaking laws. But hey, history is rarely made by...

This is another example that Twitter needs richer semantics. It should not be possible to delete a tweet. There should be some way to mark it as "retracted".

TLDR: The Pres. of FTX made a confusing tweet about some external FDIC-insured accounts FTX uses to store some customer funds, that the FDIC claims could imply FTX accounts themselves are FDIC insured. And another tweet that says "stocks... are held in FDIC insured accounts," which is untrue since the FDIC does not insure stock holdings.

Seems likely it's a genuine mistake on their part, totally fair for the FDIC to call it out, and seems like as long as they acknowledge that the tweets could be misleading and give the tweeter a talk, it's just a warning.

> Seems likely it's a genuine mistake on their part

If the president of a financial services company didn't understand, in substantial detail, which types of account FDIC insurance applies to, I'd have some big questions about their capacity to manage a financial services company.

Read the tweet, it's not that he didn't understand, he was in fact talking about FDIC insured accounts, just ones that FTX uses, not FTX accounts themselves.

The FDIC is being a little pedantic here, but that's fine, it was a warning and he deleted the tweet.

> Read the tweet, it's not that he didn't understand, he was in fact talking about FDIC insured accounts, just ones that FTX uses, not FTX accounts themselves.

Yes, he's repeating an old scam that has played out a number of times in this space.

1. Build customer confidence by telling them that your[1] accounts[2] are FDIC-insured[3].

2. Go to Vegas and put all your customers' money on red.

3. Whoops.

It's fine for some Joe on reddit to be this willfully ignorant and misleading about how the technicalities of FTX, its accounts, and the FDIC work. But it's not fine for the CEO of FTX to do this. It's his job to know this shit, and it's his job to not mislead his customers. [4]

[1] And by your, we mean our.

[2] And by accounts, we mean our operating accounts.

[3] And we don't mean insured against us doing stupid shit with your money, we mean insured against our counterparty running off with our money.

[4] Well, it would be if he weren't running a fly-by-night wildcat bank.

I wouldn't be so quick to assume good faith. Voyager made the same "pedantic" mistake in their marketing materials and quite a few retail investors got a nasty surprise when they collapsed.

Given that Sam is one of Tether's biggest customers, plus his US campaign donations and efforts to deregulate derivatives markets (when has that ever been a bad idea?), I consider him far more dangerous than Mark Cuban could ever be.

Especially given that other crypto funds have deliberately misled customers about the presence and/or significance of FDIC insurance, and subsequently collapsed:

It seems like a mistake, but the sort of mistake that makes me even more wary of them.

They seemed to phrase things to imply things were more insured than not. It seemed like they tried their best to arrange the verbiage in a way where they could be technically correct while still giving the wrong impression. So if something went tits up, they could say, "No, what we said was this". And it seems like they messed that up. They crossed the line that they didn't want to cross.

So I'm sure that it was a mistake. They didn't mean to say the thing. But they really, really, really wanted to imply that thing. So, yeah, sketchy as hell.

Just a regulator telling an exchange to remove a confusing tweet. A false alarm to collect impulse upvoters who read as far as the clickbait headline.

So it's business as usual and no major investigation or breathtaking slam duck billion dollar fine this time.

Move along now, nothing to see here.

EDIT: So what I said isn't true and the tweet was not deleted? The misleading tweet in question has been deleted. As instructed by the FDIC:

'We hearby demand that you cease and desist, and take immediate corrective action to address these false statements, as more fully set forth below.'

FTX were caught by the regulators, they complied and that is that. There are no investigations, fines, lawsuits, or any grand trial of the century that you thought you were looking for. This ain't it.

The regulators are doing their job and the system is working.

{kind=link}

The trouble with FTX is that they are a pretend bank and brokerage. They offer services that look like banking and brokerage, but the backup isn't there. They're not regulated as a bank or a broker, and they don't have the insurance of a bank or a broker.

From their site:

* "FTX US is a US licensed cryptocurrency exchange that welcomes American users."

* "The safe and easy way to get into crypto."

* "We are US based and regulated"

* "Don't be like Larry".

There is a concerted effort to create an illusion of legitimacy.

Even in their disclosures[2], you can see them trying to create the illusion that they're regulated as a financial institution. Their derivatives unit, FTX US Derivatives, does have some of the licenses of a commodity exchange. The main company, "West Realm Shire Services" (remember Magic, the Gathering Online Exchange?) just has money transmitter licenses. Not in NY or CA, interestingly. They don't have a banking license from a state. Or a New York State BitLicense. Or a brokerage license from the SEC.[3] Or an exchange license from the SEC. Or Security Investors Protection Corporation insurance. Or Financial Industry Regulatory Authority regulation.

[1] https://newsoutlet.ai/blockchain/celsius-ceo-alex-mashinsky-...

[2] https://ftx.us/legal/regulations-licenses

[3] https://www.sec.gov/reportspubs/investor-publications/divisi...